Eurozone: In Dire Straits?

Amid all the concern about the energy-induced surge in inflation resulting from the Middle East conflict, the impact on EZ real economy looks to be sizeable and growing. High profile PMI numbers are flashing alarmingly, but the message from the April composite (at a 17-mth low) may actually be not pessimistic enough for a variety of reasons. Instead, European Commission aggregated survey data suggest a much bleaker picture, actually suggesting a GDP backdrop of stagnation for the current quarter, thereby adding to the downside surprise the ECB has to consider from the Q1 national account numbers. Although not yet our official line of thinking, the ECB does seem to have its figure on the hiking trigger and will pull it without some positive news from Middle East conflict such as re-opening of the Straits of Hormuz. But if a hike occurs this is only going to add to real economy downside risks, both by damaging sentiment further, increasing costs and adding to what already signs of EZ banks wariness about lending, all suggesting rate hikes will not last.

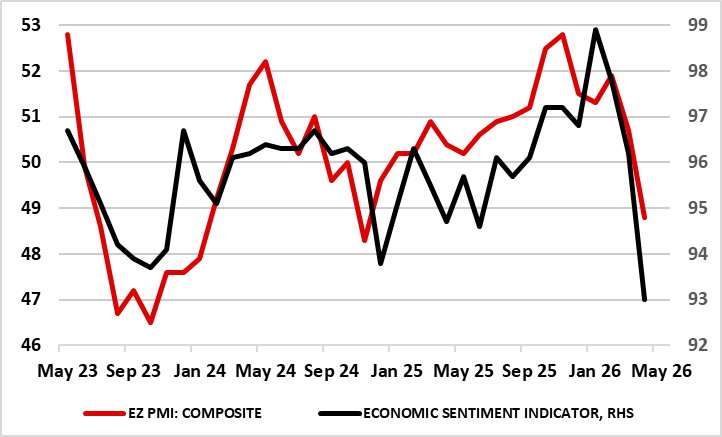

Figure 1: Softer But Divergent Business Surveys?

Source: European Commission, Markit, Continuum Economics

Once Upon a Time in the West

We remain critical of the ECB assertion (at least before the Iran War) that the EZ economy was in a ‘good place’. This to us was too backward looking and amid some signs in both hard, soft and monetary data, that the economy going into the last quarter was soft and fragile. Indeed, flash GDP results for Q1 (0.1%) suggest less apparent resilience despite a surprise pick-up in German growth that conflicts with the slight growth pencilled in by the Bundesbank. But amid what was still below trend growth in Q1, there are some worrying aspects, not least what may be a major involuntary inventory build in France and German data where weakness in imports may have been the major ‘support’, this the case for Spain and Italy too. Regardless, the Q1 EZ outcome is clearly below ECB thinking (0.3%), the latter envisaging weakness in coming quarters that very much contrast with the pattern of growth seen four years with the last energy price shock.

Industrial Disease

But business and consumer surveys are flashing worrying signs even suggesting that the ECB’s modest real economy outlook for the current quarter is under threat – ie all envisaging 0.9% 2026 GDP growth. This is very much a reflection of the Middle East conflict but, where unlike the Ukraine War shock of four years ago, it is services that have shown the greater weakness of late (Figure 3), this possibly being a factor in those same surveys suggesting less price pressure in that sector than four years ago. Most high-profile has been the drop in EZ PMI figures if late. But the message from the April composite (at a 17-mth low of 48.8) may actually be not pessimistic enough for variety of reasons. For a start, it incorporates a manufacturing reading of 52.2 which implies solid activity in the sector – normally. However, this instead is a result of slowing delivery times which usually would imply rising demand, but at present reflects growing supply problems. Secondly, the composite does not include construction, but aggregating the former to include the latter points tn ‘overall’ PMI nearer 47. Such weakness is instead best seen in the European Commission business survey data, most notably its Economic Sentiment Index (ESI). This ESI has several shortcomings, not least how coincident the updates are, but it incorporates services, manufacturing retail and construction and tallies better with EZ GDP growth, especially when the latter excludes the very volatile Ireland component.

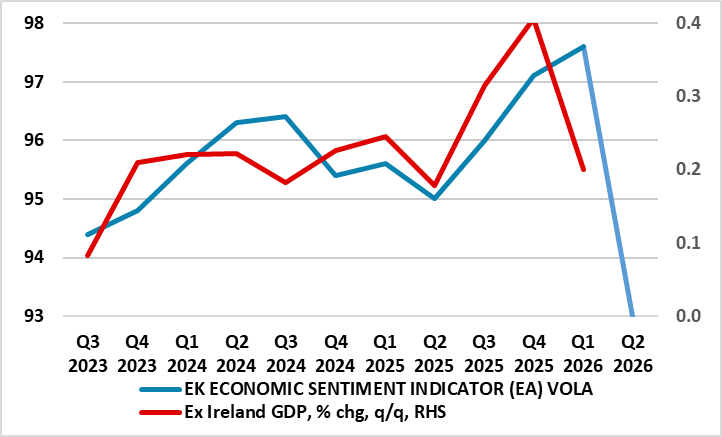

Figure 2: ESI and Ex Ireland EZ GDP

Source: Eurostat, European Commission

Notably the April ESI which actually drop back to early pandemic readings is consistent with flat GDP growth (Figure 2) in EZ – and that may be not pessimistic enough given the manner in which supply problems may cause as much damage in stalling output as they do in pushing up costs and prices. All of which to us suggest downside risks to our already- below consensus 0.6% 2026 GDP projection suggesting that the downgrade made by the ECB in March was too little, too late. But this also to us reflects not only to the rise in effective borrowing rates but also to the increasing bank reticence to lend. In fact, it has been increased bank wariness about lending seen more broadly over the last 6-9 months or so that has been possibly the prime factor behind our continued below-consensus growth outlook and criticism that the ECB has been (and is still being) complacent. This is hardly Money for Nothing!