Asia/Pacific (ex-China/Japan) Outlook: The Iran War Shock

· The Iran war macro impact on Asia depends on length of the conflict and impact on energy flows. Our baseline is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end 2026 and USD60 by Q3 2027 (here).

· India GDP growth has been revised down slightly and CPI forecast pushed up, but India has less excess demand and non-energy supply constraints than when the Ukraine war energy shock hit in 2022. Price control and subsidies help in a short war. This should see a muddle through by India, with CPI coming back down in 2027, as energy prices fall further. A dovish RBI is likely to keep the policy rate unchanged, but use its large FX reserves to ensure only further modest INR depreciation.

· Indonesia 2026 CPI inflation is being revised upwards from 2.0% to 2.9% due to the energy price shock, but we have revised down 2027 CPI from 2.5% to 2.3% as energy prices reverse. This provides a dilemma for Bank Indonesia (BI). Before the Iran war, BI was looking for an opportunity to cut interest rates to support growth. However, with the 2026 pick-up in inflation and the Indonesia Rupiah weak it is difficult to see the BI cutting in 2026 – MSCI is also threatening to shift Indonesia from emerging to frontier status, which would dent foreign investor flows. Nevertheless, if a 4-8 week war is seen and energy prices reverse, then we feel a window of opportunity should open in 2027 for BI and we look for a 25bps cut to 4.25%.

· Australia will be impacted by energy prices pushing up CPI inflation further at a time when domestic inflation is already more elevated than RBA desires. However, the RBA had already been proactive before the Iran war (while policy rates are much higher than 2022) and we feel one further 25bps hike should be enough to restrain 2nd round effects. The reversal of energy prices should allow a more controlled inflation outlook into 2027.

· In Malaysia our 2026 inflation forecast is revised up to 2.7% from 2.0%. Nevertheless, a 4-8 week war is unlikely to produce 2nd round effects and as energy prices come back down we see inflation ebbing. We are thus reducing the 2027 CPI forecast from 2.5% to 2.3%. BNM will look through the CPI pick-up and keep the policy rate unchanged at 2.75%

· Risks To The Forecast: A 2-to-6 months Iran war can spike WTI to USD 120-180 (depends on duration and further damage) and remain elevated for the remainder of 2026. This would prompt a stagflation hit to the global economy and Asia and in some cases prompt modest to moderate rate hikes to lean against 2nd round effects e.g. 50-100bps hike from RBI. GDP growth more adverse impacted.

Our Forecasts

| GDP Growth | Inflation | Policy Rate | |||||||

| 2025 | 2026 | 2027 | 2025 | 2026 | 2027 | 2025 | 2026 | 2027 | |

| Australia | 1.9 | 2.2 | 1.8 | 2.8 | 3.1 | 2.1 | 3.60 | 4.35 | 4.1 |

| India (FY 25/26/27 for GDP) | 7.3 | 6.4 | 6.4 | 2.1 | 4.1 | 4.2 | 5.25 | 5.25 | 5.25 |

| Indonesia | 5 | 4.8 | 4.8 | 1.8 | 2.9 | 2.3 | 4.75 | 4.75 | 4.5 |

| Malaysia | 4.7 | 4.6 | 4.4 | 1.9 | 2.7 | 2.0 | 2.75 | 2.75 | 2.75 |

Source: Continuum Economics

Risks to Our Views

| Risk | Probability | Impact | |||

| Upside | Iran war settlement cause quicker reduction in energy prices than our baseline. | Low to Medium | Medium | ||

| Structural reform efforts gain traction and enables strong medium-term Asia growth. | Low to Medium | Medium | |||

| Downside | 2-6 month war leads to energy prices surge up to demand destruction levels of USD120-180. Regional economies CPI surge threaten 2nd round effects and temporary policy tightening. GDP Growth also hit. | Medium | High | ||

| Trump administration gets aggressive on new tariffs, which cause 2026 trade tensions and export hit – very low probability, while Iran war elevates energy prices. | Low | Medium | |||

Source: Continuum Economics

India

The Iran war economic effects at least hit at a time when India had been enjoying a Goldilocks period of good growth and controlled inflation. Even so, our baseline of a 4-8 week war means that we have to revise down the GDP outlook slightly to 6.4%, as the government cannot fully protect the economy from the supply disruption. Oil imports are also 3.1% of GDP, which means higher costs will likely hurt other domestic spending. India has already switched some oil purchases towards Russia, with April orders of 60mln barrels double the February figure, but at a USD5-15 premia to Brent prices. Though price controls and subsides will curtail the initial impact of higher oil prices, we have also revised up our 2026 CPI forecast to 4.1%.

The lower effective trade tariffs from the U.S. (10% with section 122 rather than the higher reciprocal tariffs), will continue to feed through and help CPI. Meanwhile, core inflation at 4% was controlled before the Iran war. Even so, higher cooking oil prices will feed through quickly, while LNG is a headache. Though India has only about 5 days of strategic oil reserves it can redirect oil purchases from other countries. The problem for LNG is that alternative providers are also seeing strong demand from Japan/S Korea and Taiwan, which is keeping Asia gas prices high and supply tight. Meanwhile, nitrogen fertilizer prices have surged as the Middle East is a big supplier via the Straits of Hormuz and India is a large importer of Urea and other Nitrogen fertilizers. This can have a direct effect on food prices later in 2026, which could be amplified if India farmers reduce use of nitrogen fertilizer and then crop yields turn out to be lower than previous projections! This is an upside risk to our 2026 inflation forecast.

The RBI has to navigate these challenges. We expect the RBI to not hike the policy rate on our view that oil and gas prices will come back down later in 2026. The RBI has a dovish bias, which was evident in February where 2 members were building the case for easing. Easing is no longer on the cards, but a high bar exists for a hike. The RBI will likely expect limited 2nd round effects, as the situation is different from 2022 when the Ukraine oil price spike came against a buoyant post COVID demand picture. Additionally, non-energy and fertilizers goods are not impacted by the global supply disruption seen in 2022 and China is currently keen to export globally. The RBI initial guidance in the latest state of the economy report was also to emphasize the resilience of the Indian economy. Some words of caution should be seen from the April 8 RBI meeting, but we do not expect this to translate into any rate hikes in 2026.

Meanwhile, though the India Rupee (INR) has depreciated since the start of the Iran war, the direct impact on inflation is moderated by the closed nature of India’s economy. The indirect psychological effect on INR depreciation is a potential inflation issue, given the overemphasis on the INR in the media. However, the RBI has large FX reserves, which we expect them to continue to use in the acute war stage and we see a managed depreciation through the remainder of 2026 to the 95.50-96 area on USDINR. A rate hike for INR weakness is not likely, as the RBI FX reserves are large enough and foreign investors have already cut India asset holdings substantively in the past 15 months.

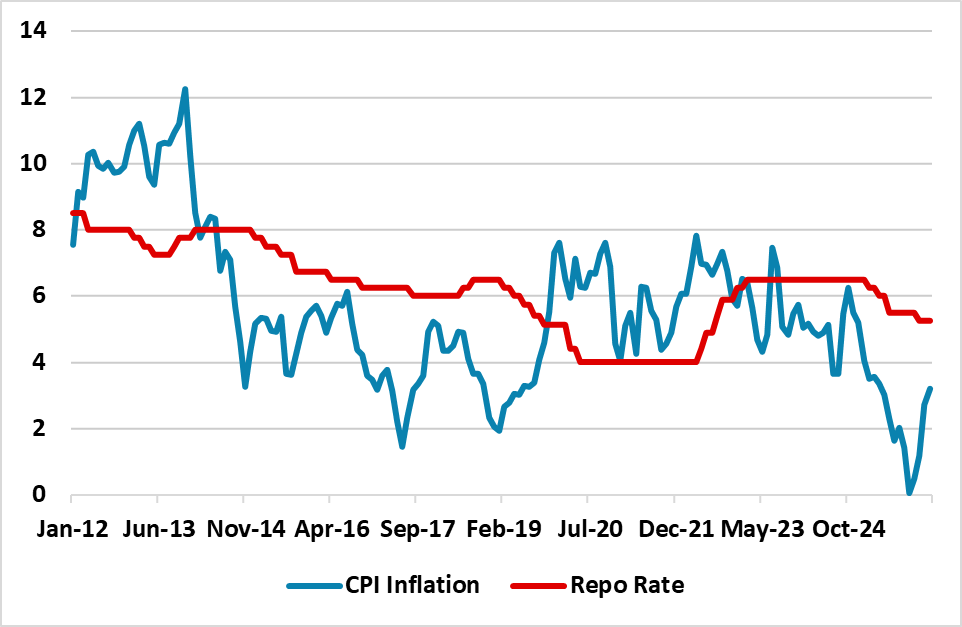

Figure 1: India CPI, Policy Rate (% change, yr/yr)

Source: Datastream/Continuum Economics

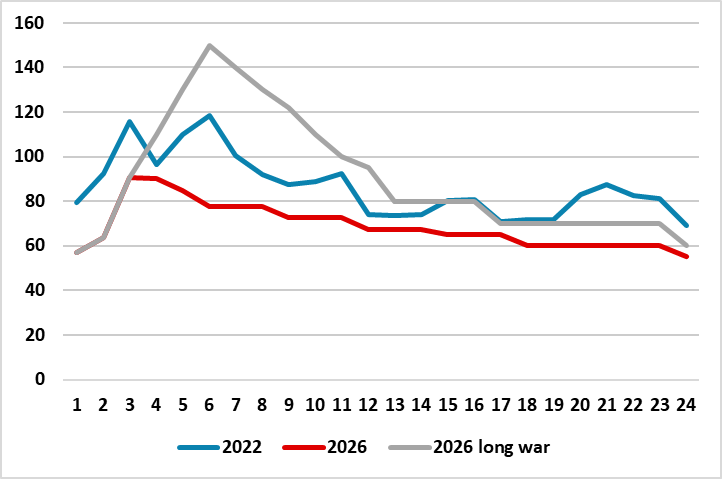

A crucial assumption is that the Iran war lasts 4-8 weeks. Figure 2 shows our forecast for WTI prices in the remainder of 2026 and 2027 and contrast that with the profile of WTI through the early stages of the Ukraine war from 2022 and 2023. We see oil prices coming down by Q2 with the end of a 4-8 week war, which is a short duration than the 2022 Ukraine war. This is helpful as India energy subsidies act as a buffer and reduce feed through to hurt growth and boost CPI. It is also worth noting that LNG gas prices are nowhere near as high as the Ukraine war, as 2% of global gas is shipped through the Straits of Hormuz versus 20% of global gas cut off during the Ukraine war.

A 2-to-6 months Iran war can spike WTI to USD 120-180 (depends on duration and further damage) and remain elevated for the remainder of 2026 – see Figure 2. This would prompt a stagflation hit to the global economy; and in some cases prompt modest to moderate rate hikes in Asia to lean against 2nd round inflation effects. For India, this is a worse oil shock than the Ukraine war, which would knock 1% off our 2026 GDP forecast and boost CPI inflation to 6-7%. A dovish RBI would be forced into temporary rate hikes of 50-100bps to guard against 2nd round effects, but then look to reverse in 2027.

Figure 2: WTI Oil Price Including CE Forecasts (USD)

Source: Continuum Economics

Indonesia

The Iran war comes at a difficult time for Indonesia. The rating agencies are already upset with signs of fiscal slippage and concerns that the 2003 3% limit on the budget deficit could be broken by populist programs (free school meals and welfare programs). Now energy subsidies are being put under pressure by the elevated oil prices. The government will try to cushion the economy from the effect of the high energy prices, but we would suspect that the threats of rating agency downgrades could mean that this is somewhat less than would normally occur. This means that the feedthrough of energy prices to hurt GDP growth could be somewhat more than in government forecasts of 5.3% 2026 GDP growth and we have revised down our GDP forecast to 4.8%. Even so, Indonesia is a modest net oil importer, but exports coal and this means the direct hit from supply disruption should be small on GDP. However, we keep 2027 at 4.8%, as our baseline of a 4-8 week war and then reversing energy prices should help support 2027 growth.

2026 CPI inflation is being revised upwards from 2.0 to 2.9% due to the energy price shock, but we have revised down 2027 CPI from 2.5% to 2.3% as energy prices reverse. The 4.8% CPI figure in February will unwind in March, as February was distorted upwards by adverse base effects. Even so, inflation could push above 3% Yr/Yr into the spring.

This provides a dilemma for Bank Indonesia. Before the Iran war, BI was looking for an opportunity to cut interest rates to support growth. However, with the 2026 pick-up in inflation and the Indonesia Rupiah weak it is difficult to see the BI cutting in 2026 – MSCI is also threatening to shift Indonesia from emerging to frontier status, which would dent foreign investor flows. Nevertheless, if a 4-8 week war is seen and energy prices reverse, then we feel a window of opportunity should open in 2027 for BI and we look for a 25bps cut to 4.25%. Healthy FX reserves means that BI can manage currency pressures in the near-term.

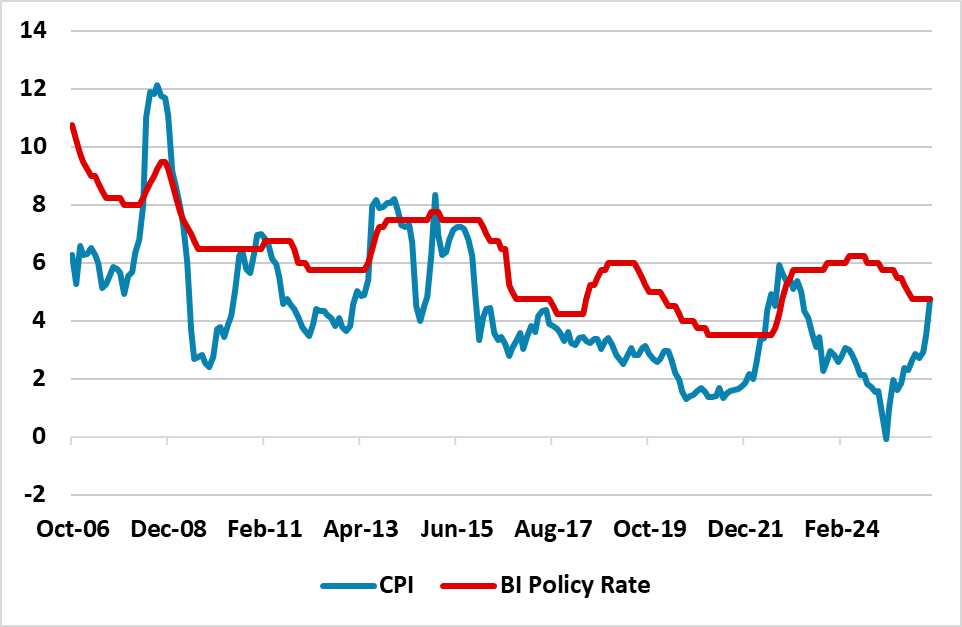

Figure 3: Indonesia CPI, Policy Rate (% change, yr/yr)

Source: Datastream/Continuum Economics

In the alternative scenario of a 2-6 month war and USD120-180 oil prices, Indonesia would be under severe pressure. This would be a worse oil shock then the Ukraine war and would threaten to boost annual inflation outside of BI 1.5-3.5% inflation target. Headline CPI could spike to 5-6%, which would likely force BI to undertake 50-75bps of hikes to guard against 2nd round effects. The adverse GDP hit would also be greater, as limited fiscal space would mean that the government could not provide large subsidies against the energy shock.

Australia

The RBA underwent a decisive shift in the first quarter of 2026 as they raised the official cash rate for the second consecutive month, bringing it to 4.1%. This was a narrow 5–4 split decision that reflected a change toward an active stance in response to geopolitical energy shock and rising underlying inflation. The hawkish pivot from before the escalation of conflict in the Middle East, which disrupted global shipping and pushed energy prices significantly higher. This external shock has complicated the inflation path just as the base effects from the expiration of government energy rebates began to take effect. While headline inflation held steady at 3.8% in January, the trimmed mean CPI edged up to 3.4%, signalling that underlying inflation is more entrenched now. The RBA Board noted that while some of these factors are transitory, the risk of inflation remaining above the 2–3% target band for a prolonged period was too high to ignore.

The domestic demand resilience seen throughout 2025 has begun to show cracks under the weight of negative real wages. Although the Wage Price Index remained solid at 3.4% y/y, it continues to lag headline inflation. This has turned Australian' consumers head towards a higher household saving ratio (from 6.1% to 6.9%— highest level since September 2022). We have revised 2026 GDP lower to 2.2% and 2027 at 1.8% accordingly, also factoring in tighter fiscal policy from the RBA.

Investment has become another pillar of the Australian economy, specifically within the digital and green energy sectors. Private investment grew significantly in late 2025 and remains firm in early 2026, led by a massive wave of capital expenditure in AI-ready data centers. These are being paired with significant public investment in renewable energy zones and water infrastructure.

Looking forward, the trade outlook is volatile from ongoing geopolitical tension. While LNG prices have spiked alongside oil due to physical disruption, iron ore export is relatively steady supported by Southeast Asian and Indian demand. This could potentially be a boom for exporters and bane for Australian residents.

The RBA has taken a hawkish stance in the March meeting. They are seeing the service sector continuously driving inflation higher, given the current solid labor market (4.3% unemployment). Our forecast for 2026 CPI is revised higher to 3.1% and 2.1% for 2027, to reflect the inflationary impact from the Middle East chaos and then the unwind helping subdue inflation in 2027. We are only seeing one more 25bps hike from the RBA in the May meeting to 4.35%, unless geopolitical tension persists longer than our central forecast of a 4-8 week war. Figure 4 shows that policy is already restrictive in contrast to the start of 2022. If we do see a 2-6 month war then, we could see another 25bps hike from the RBA to curb the red hot inflation.

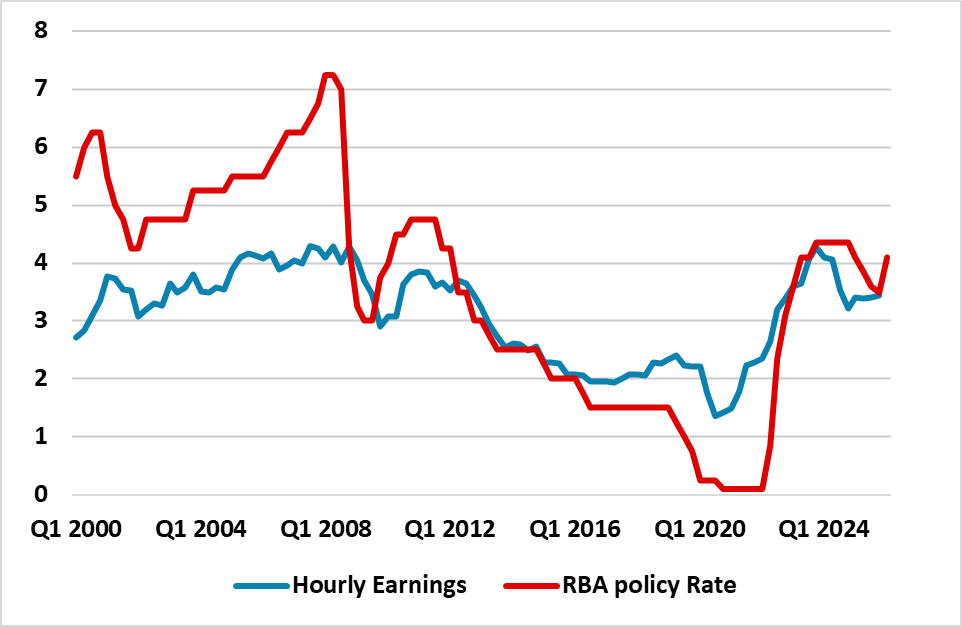

Figure 4: Australia CPI, Policy Rate (%)

Source: Datastream/Continuum Economics

Malaysia

The surge in oil prices due to the Iran war has prompted an upward revision in our 2026 inflation forecast to 2.7% from 2.0%, as oil and gas prices feed into the economy. Nevertheless, a 4-8 week war is unlikely to produce 2nd round effects and as energy prices come back down in H2 2026 and H1 2027, the monthly inflation numbers should be better controlled again. We are thus reducing the 2027 CPI forecast from 2.5% to 2.3%.

The real sector should not be impacted. Firstly, though Malaysia is a modest net oil importer, it is a net exporter of LNG and this will find plenty of buyers. The external energy balance is thus unlikely to deteriorate. Elsewhere, the Malaysian economy continues to benefit from the AI boom, with semiconductor demand strong and order books healthy well into 2027. This should also support the economy. This leaves us inclined to keep the existing 2026 and 2027 GDP forecasts.

Central bank policy will also likely remain unchanged on a 4-8 week war scenario, as BNM will expect the 2026 CPI pick up to reverse in 2027. On the external side, the Malaysian Ringgit has actually remained strong against the USD, despite the USD bounce on the Iran war. The market appreciated that favourable energy position for Malaysia and also its AI and tech exposure and this is keeping the currency well underpinned, despite policy rates being lower than the U.S. The currency is thus also comfortable for the BNM and we see the policy rate remaining at 2.75% throughout 2026 and 2027.