Foreign Exchange

View:

July 06, 2026

Preview: Due July 15 - U.S. June PPI - Some fading from recent strength

July 6, 2026 9:05 AM UTC

We expect an unchanged June PPI, a significant slowing from two straight gains of 1.1% as energy corrects from recent strength and other inflationary stimuli from the conflict in the Middle East fade. We expect a 0.4% rise ex food and energy, matching May’s outcome, and also a 0.4% increase ex foo

July 05, 2026

July 03, 2026

July 02, 2026

Preview: Due July 20 - Canada June CPI - Energy to correct lower but BoC core rates seen mostly stable

July 2, 2026 7:58 PM UTC

We expect June Canadian CPI to correct lower to 3.0% yr/yr from May’s 3.2% which was the highest since December 2023, with a slowing to 2.98% from 3.23% before rounding. The Bank of Canada’s core rates however are likely to remain mostly stable with CPI-Median at 2.1% and CPI-Trim at 2.0%, both

Preview: Due July 6 - U.S. June ISM Services - Sustaining a May improvement

July 2, 2026 5:50 PM UTC

We expect an unchanged June ISM services index of 54.5, sustaining a May pick up from April’s 53.6. Gasoline prices moving off their highs and the World Cup may both provide some support, preventing a correction from May’s improvement. May’s bounce may have been assisted by seasonal adjustment

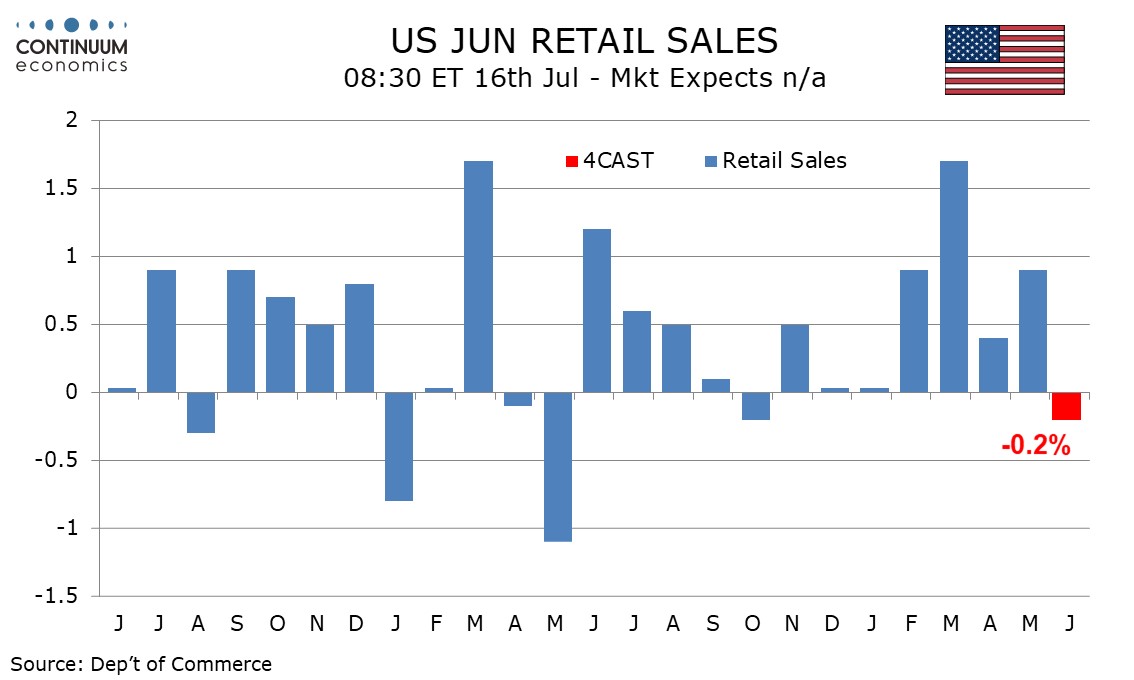

Preview: Due July 16 - U.S. June Retail Sales - Softer on gasoline, only modest underlying slowing

July 2, 2026 5:33 PM UTC

We expect June retail sales to fall by 0.2% overall and 0.4% ex autos, though with a 0.2% rise ex auto and gasoline. Even the latter would be the slowest gain since a flat December 2025.

Preview: Due July 17 - U.S. June Industrial Production - Two straight subdued months after a strong April

July 2, 2026 3:51 PM UTC

We expect an unchanged June industrial production outcome with a marginal 0.1% increase in manufacturing. This will be a second straight subdued month but still leaving a healthy Q2 given a strong increase in April.

Preview: Due July 17 - U.S. June Housing Starts and Permits - Multiple starts to bounce, but trend is slowing

July 2, 2026 3:01 PM UTC

We look for June housing starts to bounce by 13.0% to 1.33m to correct a sharp 15.4% plunge seen in May, with most of the move again due to the volatile multiples component. We expect permits to suggest a modestly negative underlying trend, falling by 2.1% to 1.38m.

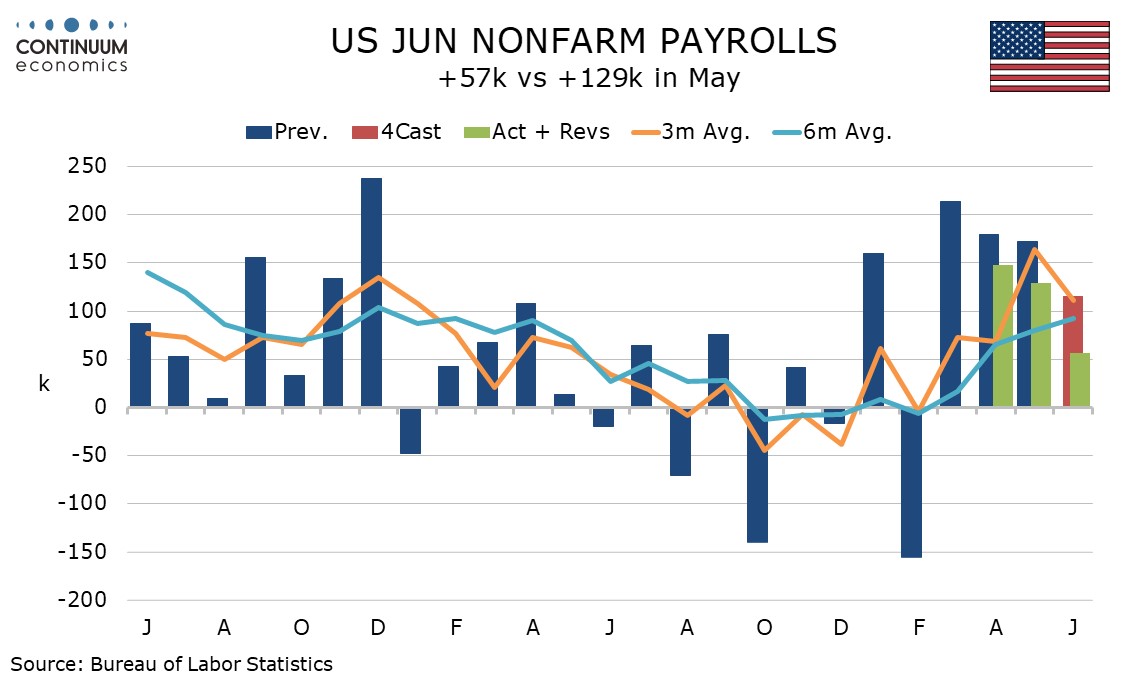

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:20 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:12 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

July 01, 2026

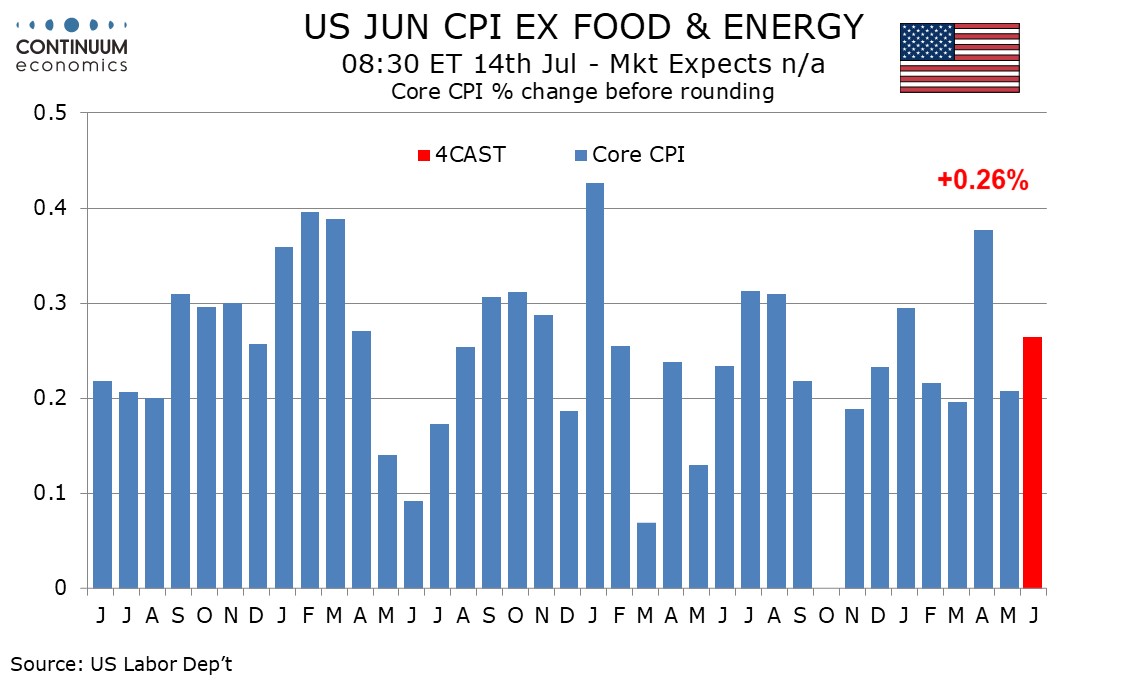

Preview: Due July 14 - U.S. June CPI - Energy to correct lower, World Cup to support core

July 1, 2026 3:18 PM UTC

We expect June CPI to be unchanged overall as energy corrects from three straight strong gains while the core rate ex food and energy sees a slightly firmer 0.3% increase. Before rounding we expect respective outcomes of -0.02% and up 0.26%, with the World Cup having just enough impact to nudge the

U.S. June ISM Manufacturing - Some easing in inflationary pressures

July 1, 2026 2:21 PM UTC

June’s ISM manufacturing index of 53.3 is down from 54.0 in May but still above the 52.7 seen in both March and April. Detail shows some easing of inflationary pressure. Perhaps more notable is an unusually large downward revision to the S and P manufacturing PMI, to 53.9 from 55.7, released 15 mi

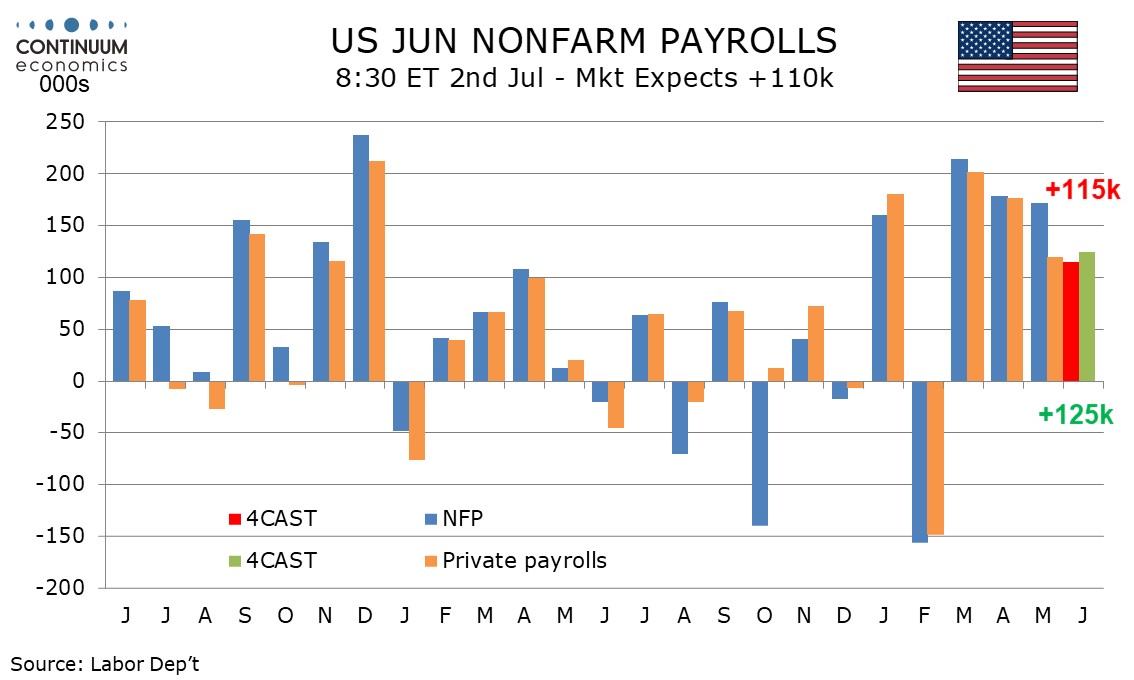

Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

July 1, 2026 12:47 PM UTC

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend

U.S. June ADP Employment - Slightly slower, far from weak

July 1, 2026 12:37 PM UTC

June’s ADP’s estimate of private sector employment of 98k is on the weak side of expectations and similarly below consensus forecasts for private sector payrolls tomorrow. It is possible that payrolls could outperform ADP data if payrolls capture more temporary jobs created by the World Cup. Our

June 30, 2026

U.S. May JOLTS report shows job openings trending higher but June Consumer Confidence shows pessimism on jobs

June 30, 2026 2:30 PM UTC

May’s JOLTS report shows a marginal 9k increase in job openings, but after a strong 698k increase in April this is stronger than expected and there has been a clear pick up in trend in recent months. The 3-month average of 224k is the highest since March 2022 as is the 6-month average of 125k.

Preview: Due July 1 - U.S. June ADP Employment - Weekly ADP data remains healthy

June 30, 2026 1:06 PM UTC

We expect a 125k increase in June’s ADP estimate for private sector employment, which matches our forecast for private sector non-farm payrolls in June. It is also consistent with a 30.75k four week average for the ADP weekly report in the weeks to June 6, the week before monthly data was surveyed

Canada April GDP - Set for a healthy Q2

June 30, 2026 12:53 PM UTC

April Canadian GDP increased by 0.5%, even stronger than a preliminary estimate for 0.4% made with March data. The data comes after a 0.1% decline in March and suggests the economy is regaining momentum in Q2. The preliminary estimate for May is for a 0.1% increase.