Iran War Scenarios

· Our central scenario (75%) remains a multi-week war in Iran. Trump loathing of long wars and high gasoline prices prompts U.S. to declare victory before end of March. Israel and Iran would most likely agree an effective ceasefire. The ceasefire would be fragile, however, as it would likely not involve concessions from Iran’s new hard-line leader, while potential Israeli hostilities could breach the ceasefire. We would see WTI at USD80-85 by April and USD70-75 by June. The main alternative scenario is a multi-month war (15%), which could squeeze oil prices up to USD120-130.

How long will the war with Iran last and what will happen to energy prices in the coming quarters?

Figure 1: Iran War Scenarios and Oil Prices

· Source: Continuum Economics.

With war in an intense phase, a lot of uncertainty exists over likely outcomes. However, in one to two more weeks, the damage to Iran’s missile and offensive capabilities will likely mean that initial military objectives could be partially or fully achieved. We highlight below a number of scenarios that could occur, with some broad estimate of probability – with the understanding that these will likely change based on decisions in Iran/U.S. and Israel.

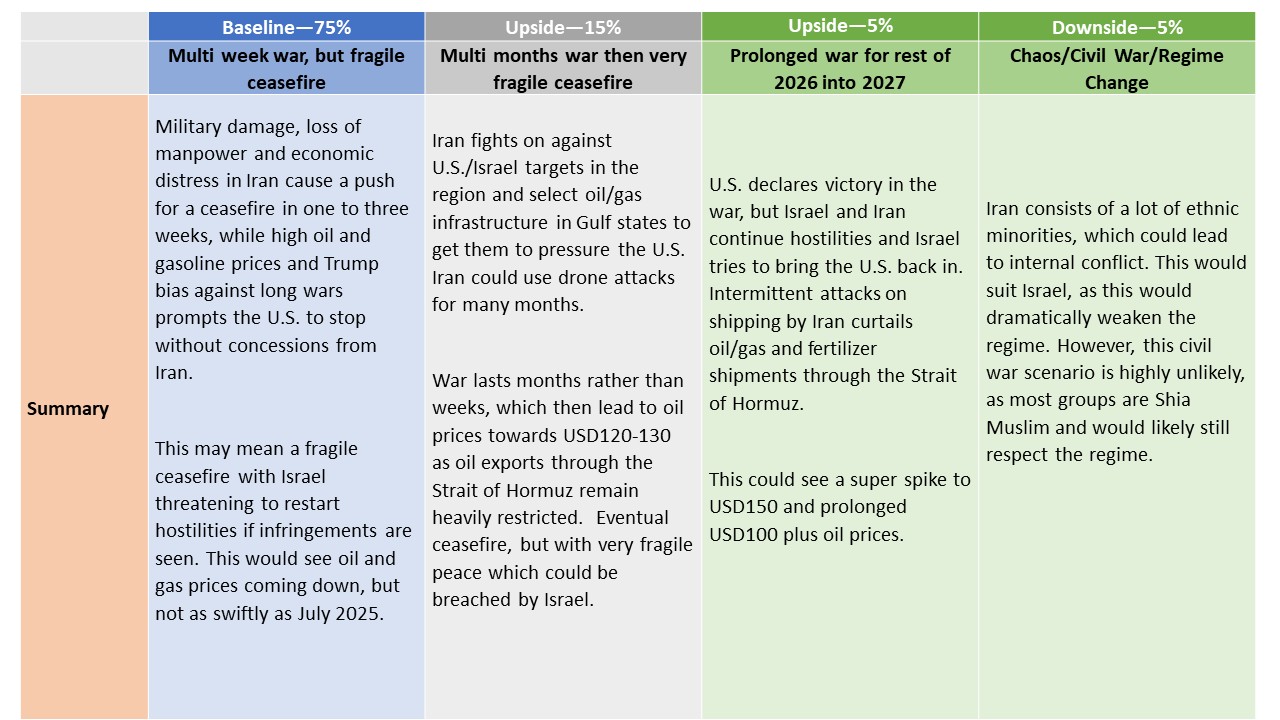

· Multi Week War, but Fragile Ceasefire (75%). Military and state infrastructure damage in Iran causes a push for a ceasefire in one to three weeks, while high oil and gasoline prices and Trump bias against long wars prompts the U.S. to stop – Trump statement on Monday that war could end very soon suggests he is looking to declare victory soon. This Trump declaration of victory could come without concessions from the regime (e.g., stopping nuclear weapon development). Israel may not be fully satisfied, as their aims are either regime change or chaos (see below). Iran’s nuclear threat would still linger multi-year. This may mean a fragile peace with Israel threatening to restart hostilities if infringements are seen. In turn, this could cause lingering tension throughout the Middle East. This would see oil and gas prices coming down, but not as swiftly as July 2025 and a residual premium would exist in case hostilities restart. However, by the summer some negotiations could restart between Iran and the U.S. to produce a more lasting peace. We would see WTI at USD80-85 by April and USD70-75 by June (see below).

· Multi Month War (15%). Iran fights on against U.S./Israel targets in the region and select oil/gas infrastructure in Gulf states to get them to pressure the U.S. Iran could use drone attacks for many months to cause mid-level problems around the region. Iran’s new Supreme leader could also extend the war to avoid the U.S. to restart a new war at a future date. War lasts months rather than weeks, which then lead to oil prices towards USD120-130 as oil exports through the Strait of Hormuz remain heavily restricted and strategic oil reserve release is insufficient. This scenario could also involve some lasting damage to oil and gas production facilities in the region. Eventual ceasefire, but with very fragile peace means oil prices come down but risk premia would be higher than the baseline scenario above. We would see WTI at USD120-130 by April and USD95-105 by September, as production would be slow to restart. This is not our primary in House scenario, given the high economic costs of the war and the significant loss of manpower on all sides.

· War into end 2026 and 2027 (5%). U.S. declares victory in the war, but Israel and Iran continue hostilities and Israel tries to bring the U.S. back in. Intermittent attacks on shipping by Iran curtails oil/gas and fertilizer shipments through the Strait of Hormuz. This scenario could also involve a major Iran terrorist attack on U.S. interests, that sucks the U.S. back into the conflict. This could see a super spike to USD150 and prolonged USD100 plus oil prices. The main argument against this scenario is that Israel and Iran would become exhausted and a strong pressure would exist to have a ceasefire – Israel prefers a short war against Iran.

· Chaos/civil war/regime change (5%). Iran consists of a lot of ethnic minorities, which could lead to an internal conflict like Libya. This would suit Israel, as this would dramatically weaken the regime but Gulf states want to avoid this outcome as it could cause prolonged mid-level chaos in the region. However, this civil war scenario is highly unlikely, as most groups are Shia Muslim and would likely still respect the regime. The regime remains powerful supported by the military. Additionally, the IRGC would also have to be severely weakened for this to occur. Oil and gas prices would come down as Strait of Hormuz shipping would likely restart more than the multi month war scenario, but a risk premium would still exist. Regional powers, such as Turkiye, remain firmly opposed to any outbreak of civil war in Iran, viewing instability as a significant threat to their interests such as mass migration and economic costs.

Currently, WTI stands at around USD 92 per barrel. Under the first scenario, a fragile ceasefire could be reached before the end of March. Such an announcement would likely remove part of the current geopolitical risk premium. However, given the fragile nature of the agreement, oil prices would be unlikely to revert immediately to pre-conflict levels in the USD 50s.

Historically, when geopolitical shocks have driven oil prices higher, the subsequent correction has tended to occur gradually. Price retracements of 30% - 60% have typically taken place over three to nine months, or longer. Accordingly, the announcement of a ceasefire this month would likely remove only a portion of the risk premium. Assuming that the agreement allows shipping to transit the Strait of Hormuz, we estimate that roughly 15 - 20% of the geopolitical premium could dissipate initially, bringing WTI to around USD 80-85 by the end of Q1/early Q2.

During Q2 and Q3, the fragility of the ceasefire implies that tensions may persist. Sporadic attacks involving Iran cannot be ruled out, although at a lower intensity than those observed during Q1 2026. As conditions gradually stabilize, while uncertainty remains, an additional 10% of the geopolitical premium could unwind. Under this scenario, WTI prices would likely average USD 70-75 during the Q2 and Q3. By Q4, if the ceasefire holds and the conflict does not escalate, a further reduction in the geopolitical premium of around 5% could materialize. This would place WTI in the USD 65-70 range by the end of the year.

Looking ahead to 2027, the conflict will likely lose momentum and most of the geopolitical risk premium would have dissipated, allowing oil prices to realign with underlying market fundamentals.