ECB Review: ECB Mixed Communications

· Overall, the June and July meetings have live risks that the ECB could undertake a modest 25bps hike. If a partial reopening of the Straits of Hormuz occurs then the ECB will likely keep hawkish, but not actually hike. We feel that the ECB is overestimating natural gas prices, while financial conditions and the economy argue for caution against hiking. Lagarde did note in the Q/A that financial conditions tightening is evident. The odds would then be that the ECB does not hike in 2026. Alternatively, if the Straits of Hormuz is still closed by the June 11 meeting, then the hawks could be able to push a 25bps hike through at the June meeting or commit to a move in July. The doves would counter that 2nd round wage effects are absent meaning a hike would not be guaranteed.

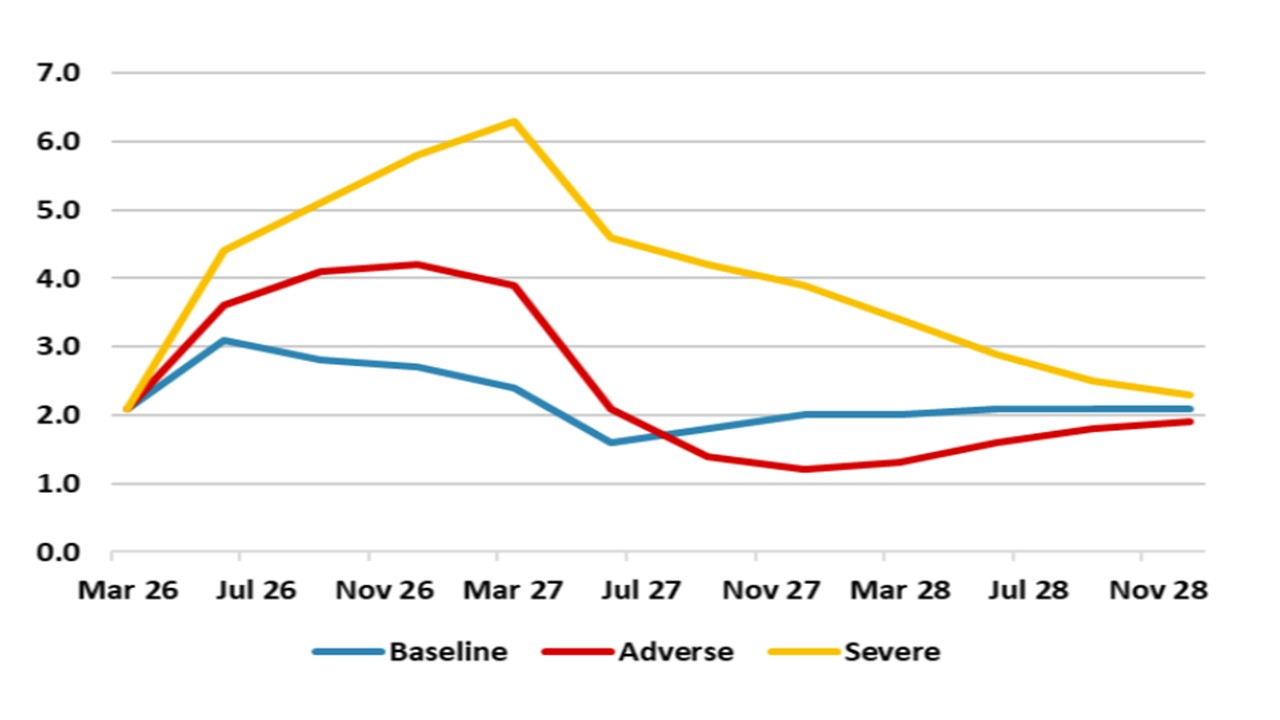

Figure 1: EZ HICP Including Projections From March Forecasts (%)

Source: ECB

A number of points are worth making from the April ECB statement and press conference.

· ECB wait and see, but council split. The initial monetary decision announcement showed a wait and see approach noting upside inflation risks and downside economic risks. In the introductory statement Lagarde took the view that the economy had momentum, but the Q1 GDP numbers were weak (here) and the statement did acknowledge the softening of business and consumer surveys. Though CPI inflation has picked up this is largely direct effects from higher crude oil prices and is in line with expectations, but Lagarde noted the ECB is not seeing 2nd round inflation effects. However, the ECB faces uncertainty over the oil and oil product price trajectory until the Straits of Hormuz is reopened, where the current stalemate is not being broken by talks. This means differing views on 2nd round effects, which drives the 2026 monetary policy debate and the duration of the closure of the Straits of Hormuz is the key swing policy factor. Lagarde noted that the backdrop is moving away from the March baseline but would not be drawn on whether thinking is in line with the adverse scenario (on the basis that new alternative scenarios will be released in June). She also noted that a rate hike was debated at the April meeting, which will intensify fears of a June/July hike in the market. This latter insight came in response to the first question and is more hawkish than the tone of the introductory statement.

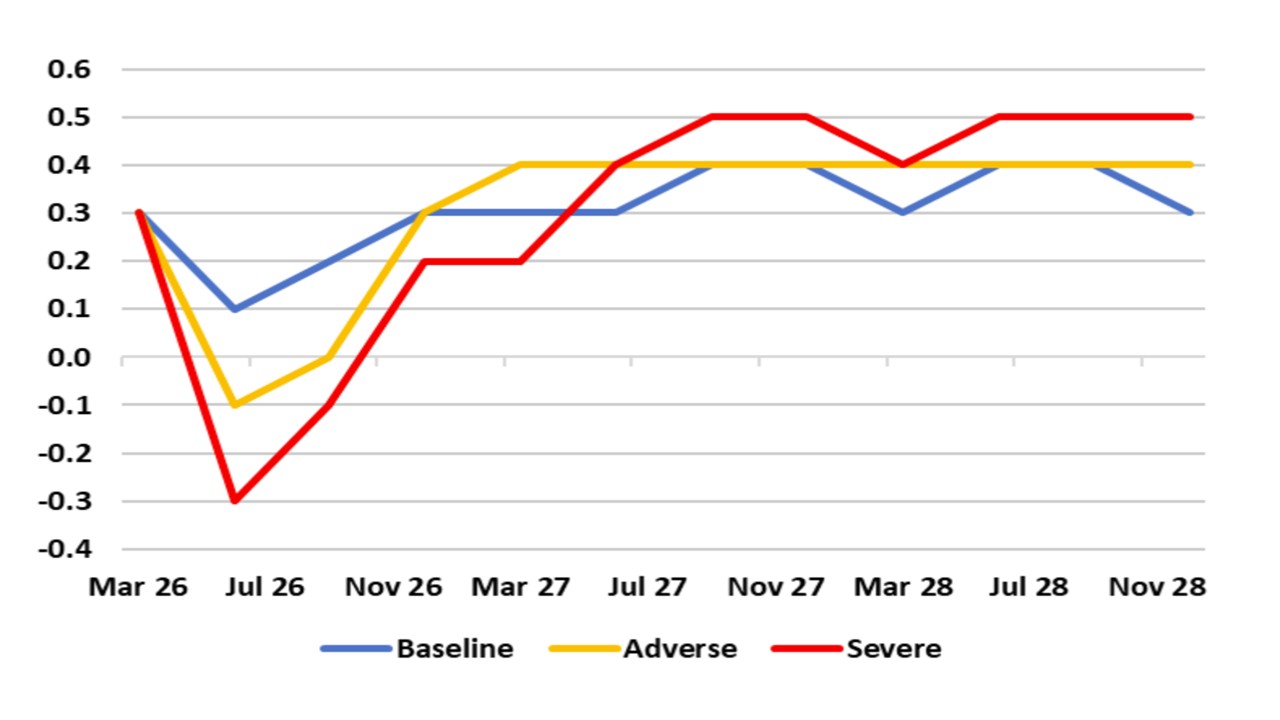

Figure 2: ECB GDP Quarterly from March Forecasts (%)

Source: ECB

· ECB scenarios wrong on natural gas prices. While the ECB March alternative scenarios have clear and credible crude oil price forecasts, the natural gas forecasts are too high. With the Straits of Hormuz closed for 2 months now, some in the ECB talk about the situation developing towards the adverse scenario (Figure 1 and 2) and some hawks wanting a hike at the April 30 meeting. However, the adverse scenario assumed European TTF prices at Eur90 versus Eur47 currently, which is also marginally below the Eur50 baseline for Q2. The Straits of Hormuz may account for 20% of LNG, but it is only 2% of global natural gas consumption. China has also quickly switched to coal fired power stations from gulf LNG. This is a crisis for crude oil and its products, but less so for natural gas and electricity prices/production/utility bills. Thus this is yet another way in which the impact on Eurozone differs from 2022 and the ECB appears to be overestimating natural gas prices in talking about the adverse scenario. This should be rectified in the June scenarios and the doves will be ware of this and argue for caution.

Overall, the June and July meeting have live risks that the ECB could undertake a modest 25bps hike. If a partial reopening of the Straits of Hormuz occurs then the ECB will likely keep hawkish, but not actually hike. We feel that the ECB is overestimating natural gas prices, while financial conditions and the economy argue for caution against hiking. Lagarde did note in the Q/A that financial conditions tightening is evident. The odds would then be that the ECB does not hike in 2026. Alternatively, if the Straits of Hormuz is still closed by the June 11 meeting, then the hawks could be able to push a 25bps hike through at the June meeting or commit to a move in July. The doves would counter that 2nd round wage effects are unlikely. Even so, the ECB does not want to overreact (mindful of its 2008 and 2011 errors) and we see the worst case scenario being two 25bps in 2026 that are then reversed in 2027.