Eurozone GDP & HICP Review: Fragile Resilience?

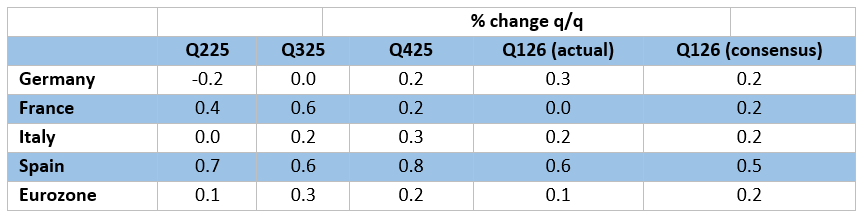

We continue to be critical of the ECB assertion (at least before the Iran War) that the EZ economy was in a ‘good place’. This to us was too backward looking and amid some signs in both hard, soft and monetary data, that the economy going into the last quarter was soft and fragile. Indeed, flash GDP results for Q1 (0.1%) suggest less apparent resilience despite a surprise pick-up in German growth that conflicts with the slight growth pencilled in by the Bundesbank. But amid what was still below trend growth in Q1 (Figure 2), there are some worrying aspects, not least what may be a major involuntary inventory build in France and German data where weakness in imports may have been the major ‘support’, this the case for Spain and Italy too. Regardless, the Q1 EZ outcome is clearly below ECB thinking (0.3%), the latter envisaging weakness in coming quarters that very much contrast with the pattern of growth seen four years with the last energy price shock (Figure 3).

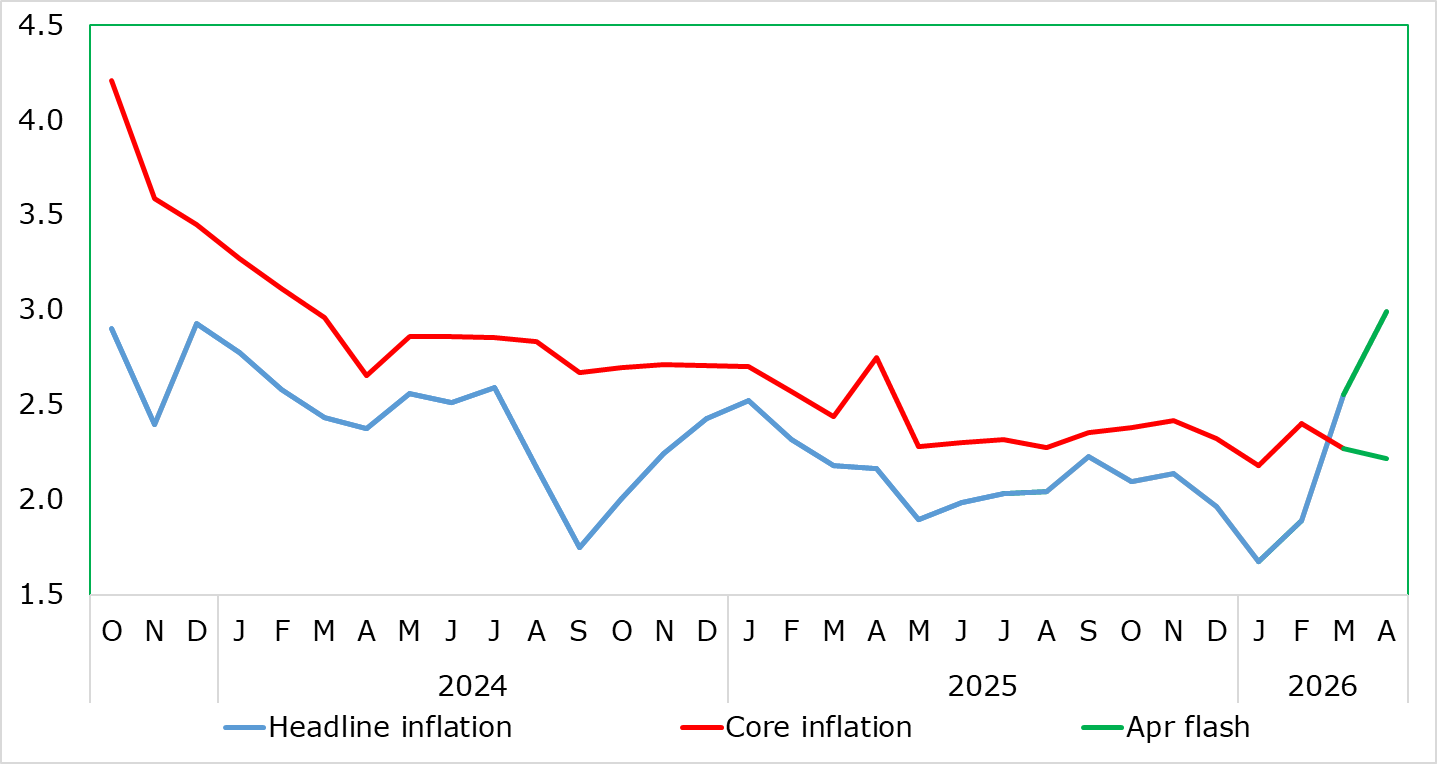

As for HICP inflation, it rose broadly as expected in the April flash, up 0.4 ppt to a 33-mth high of 3.3% what was not expected was the drop in the core rate, down notch to a 3-mth low of 2.2 on the back of what the weakness services reading (3.0%) in over four years. To what degree this reflects the timing of Easter is unclear at this juncture, but it certainly gives he ECB breathing space to assess the actuality and likelihood of second round effects.

Figure 1: Headline Soaring, Core Resistant?

Source: Eurostat

It continues to be the case that, for an economy that has seen repeated upside surprises until now and apparently above trend growth, GDP data do not seem to have had much impact is shaping, let alone dominating, ECB policy thinking save to encourage a Council view of EZ economic resilience. However, some degree of resilience had been evident, especially given the manner in which ex-Ireland GDP growth has picked up by 0.2 ppt in H2 last year so that q/q growth on this basis (at 0.4%) was actually a touch higher than EZ GDP including Ireland – this being a reversal of the backdrop into H1 last year. But this resilience is fading, even before the full impact of the conflict filters through; even with further weakness in Irish Q1 GDP, this stull means that EZ growth halved to 0.2% last quarter. It will be interesting to what degree the ECB continues to be explicit in highlighting the ex-Ireland measure not just for its better message but also because it is less volatile. But it is also the case that country divergences persisted not just between the likes of (relatively stagnant) Germany and immigration-induced Spanish strength but also with France having to rely on inventories to accomplish the moderate growth seen of late.

Figure 2: Softer But Still Divergent EZ GDP Picture?

Source: Eurostat, Continuum Economics, Bloomberg

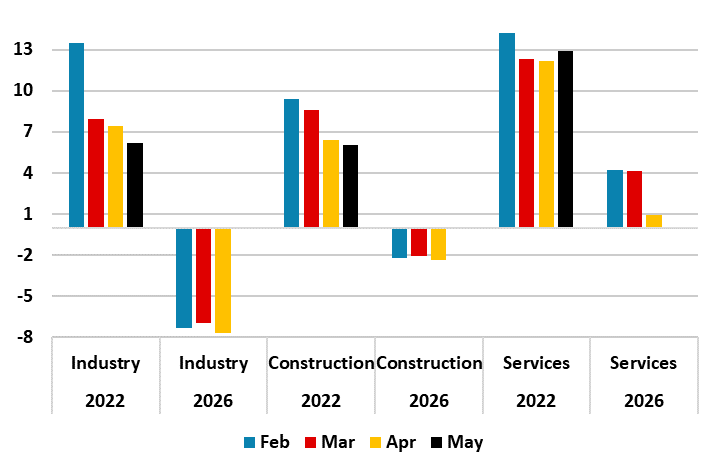

But business and consumer surveys are flashing worrying signs even suggesting that the ECB’s modest real economy outlook is under threat. This is very much a reflection of the Middle East conflict but, where unlike the Ukraine War shock of four years ago, it is services that have shown the greater weakness of late (Figure 3), this possibly being a factor in those same surveys suggesting less price pressure in that sector than four years ago. But this also to us reflects not only to the rise in effective borrowing rates but also to the increasing bank reticence to lend. In fact, it has been increased bank wariness about lending seen more broadly over the last 6-9 months or so that has been possibly the prime factor behind our continued below-consensus growth outlook (0.6% for 2026) and criticism that the ECB has been (and is still being) complacent.

Figure 3: Business Survey Signals Weaker Now – Absolutely and Relatively

Source: European Commission Business and Consumer Survey results for April 202, % balance