EZ HICP Preview (Mar 31): Headline to Surge but Core to Slip Back?

The first of the Iran War induced rise in prices arrive in the coming week with flash March HICP data. We see the headline rate spiking higher to 2.6%-2.7 from February’s 1.9%, the former largely chiming with that implied ECB thinking from the latter’s recent updated projections. But both it and ourselves see the core rate falling back in March regardless as this March surge will be purely energy-led. But with us seeing more real economy damage which together with tight(er) financial conditions we do not see the HICP rising as much as the ECB envisages beyond this quarter, albeit we do concur that the headline may be back below target by mid-2027. Thus we see the peak in HICP inflation just under 3% around mid-year. We accept risks – but on both sides but with those on the upside for inflation being possible price gouging (ie over-charging) given the manner in which the likes of heating oil prices have soared!

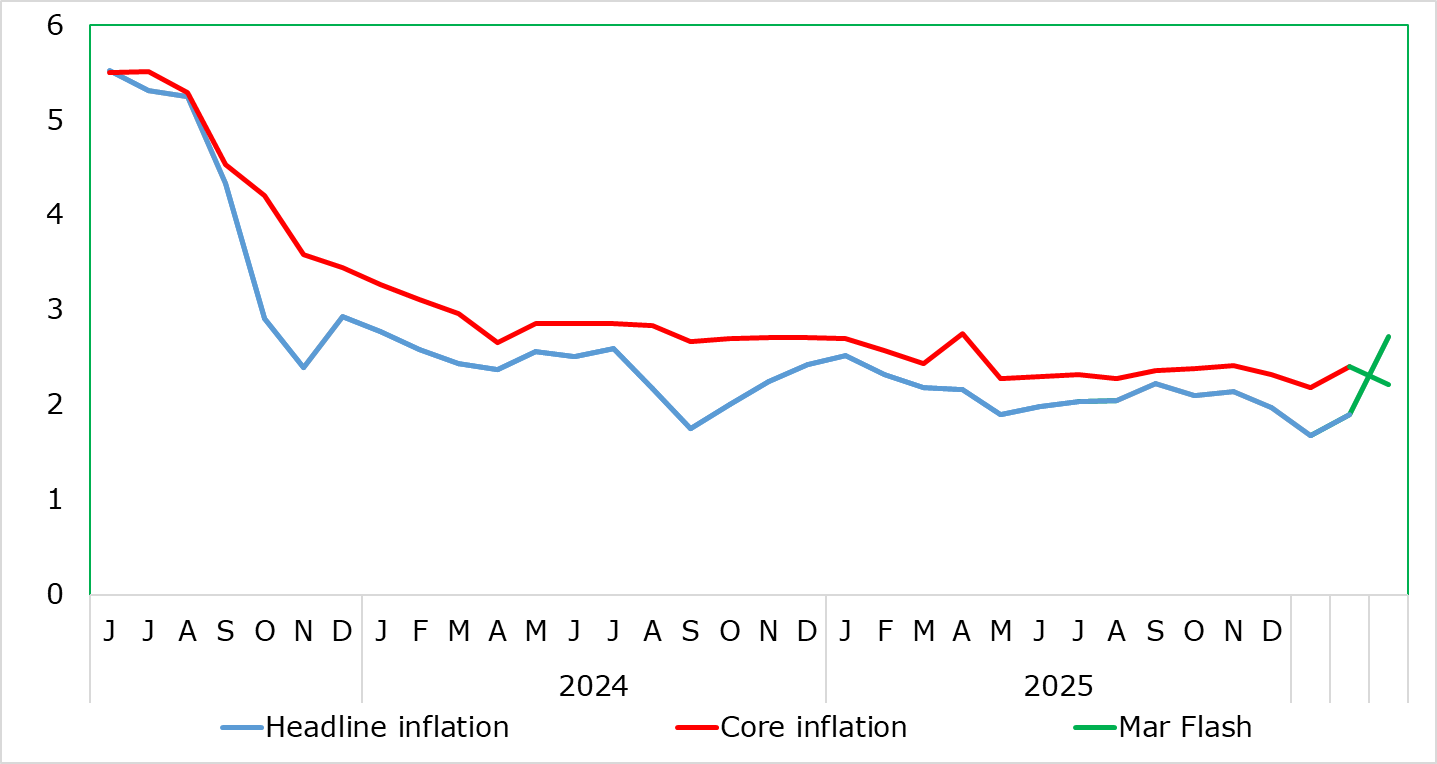

Figure 1: Headline Sharply Higher, Core to Fall?

Source: Eurostat, CE

NB; EZ HICP data are preceded by German price data on Mar 30, but which may rise even more due to both a lack of service price correction back and a more sizeable adverse energy base effect.

Having dropped to 1.7% in the January data, thereby matching expectations and the short-lived Sep 24 outcome, the headline HICP rate rose 0.2 ppt to 1.9% in February only partly due to energy. Even more unexpectedly, the core rose similarly to a 3-mth high of 2.4%. That reflected a fresh rise in services inflation and less weak non-energy goods prices, the former though linked to the Olympics and should reverse in March data – hence the anticipate drop in the core for this month.

Of course, the Middle East conflict is changing what has been a clear disinflationary outlook, certainly for headline and core inflation. Given volatility in energy prices and uncertainty about conflict goals and timing, projecting the EZ outlook at this juncture is fraught with risks causing hesitation.

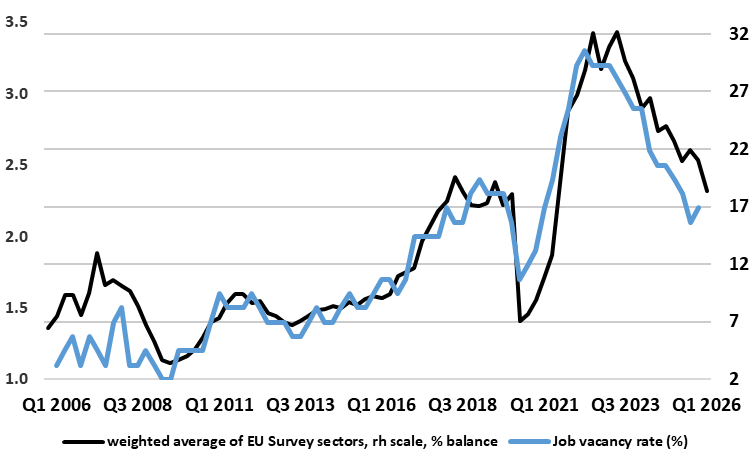

Figure 2: Labor Market Far From Tight

Source: Eurostat, European Commission, CE

Diehard hawks at the ECB remain focused on the recent rise, and seemingly more apparent resilience, in services inflation and now can allow the energy price surge to perturb them further. Of course, the ECB is still reverberating from the energy-induced surge in inflation that ensued from the pandemic and then the Ukraine War and the criticism levied at it about being slow to react. But perspective is needed as it is important to stress that the EZ economy is better positioned to absorb shocks, with the current situation very different from that of 2022 and the Ukraine War in which in losing access to Russian gas was a ‘shock’ super-imposed on an EZ economy where demand was recovering from the pandemic the latter having caused clear shortages. Job vacancy rates are now also much lower than the record highs then s are perceived labor shortages (Figure 2). Moreover, the monetary setting is vastly different now, with policy rates very positive and inflation much lower so that real rates are effectively well over 6 ppt higher than four years ago.

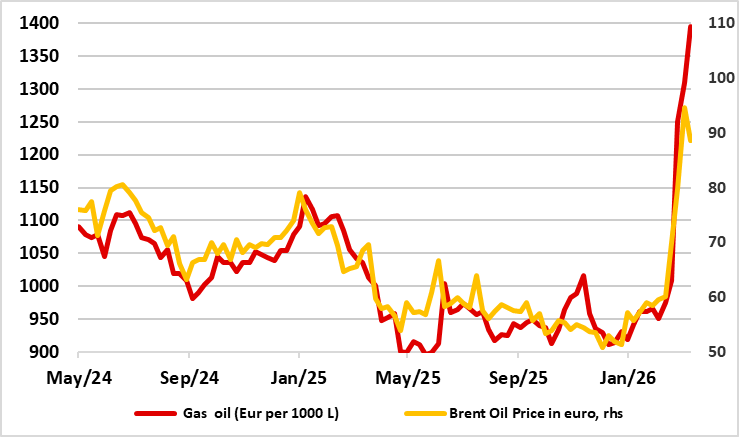

Admittedly, a clear and fresh rise in inflation is already emerging given what is happening to retail fuel prices so far this month - in some cases seemingly rising much more than perhaps the wholesale price would suggest (Figure 3). But particularly given the labor market backdrop, we see only some limited second round effects that will affect prices into 2027 (though where actual inflation at the end of next year may be lower than previously thought).

Indeed, and on the baseline of a 4-8 week war, we now see 2026 HICP inflation some 0.5 ppt higher than envisaged three months ago, averaging 2.2% but with a dip back below 2% on the cards by mid-2027 (as does the ECB) and with the HICP outlook on average for next year little changed at 1.9%.

This will be partly on account of the likely real economy damage from the conflict but also reflects our long-standing view that the ECB has been complacent, downplaying what we regard are downside real economy and monetary risks which may now be materialising. These range from ignoring the fact that a third of what looks to be above trend growth last year was abnormal (due to an aberrant surge in Ireland), the lagged U.S. tariff impact and what we think are financial conditions that have actually been tightening even before the impact of the conflict on markets.

Notably, banks have not only been tightening credit standards for some months now but are actually refusing to lend to an increasing amount of companies and are now raising effective rates to customers, this making the next ECB bank lending survey (2 days before the next Council meeting on Apr 30) all the more important. There is also the Chinese export dumping factor, this likely to depress consumer goods prices and hit GDP via increased EZ imports!

Figure 3: Price Gouging Emerging?

Source: Eurostat, CE