AI, Fed and Inflation and Disinflation Risks

• Existing Fed officials and Fed chair designate Warsh have divergent views on the impact of AI in boosting productivity and whether this means lower inflation/policy rates or high business investment/electricity prices argues against lower policy rates and potentially meaning a higher short-term neutral rate. The timing and scale of the AI adoption will become a more persistent theme in Fed press conferences and policy debates in 2026 and 2027.

Recent comments from Fed officials shows the impact of AI on the Fed economic thinking is becoming greater, but what about the inflation and policy outlook under a Kevin Warsh led Fed?

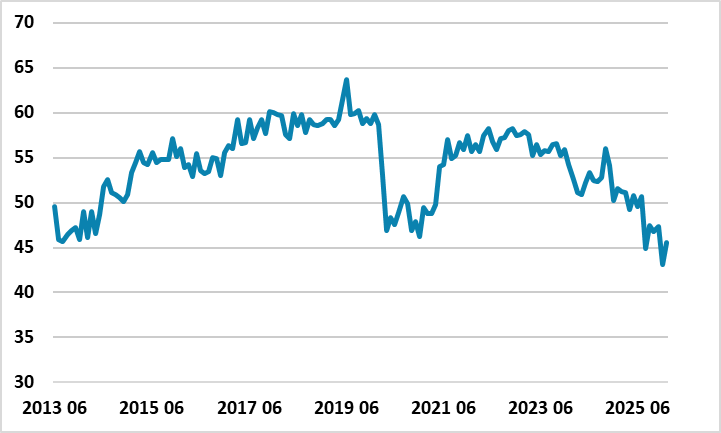

Figure 1: Mean probability of finding a job in the next three months if one loses a job today

Source: NY Fed Survey of Consumer Expectations

Fed officials are starting to talk more on the impact of AI on the economy and policy. Key points to note. • Kevin Warsh and productivity supply side disinflation. The nominated Fed chair argues that AI is already boosting productivity and will increase disinflation pressures, which we covered in a recent article (here). This comes through the classic routes of new product price reduction, but also potentially a temporary pick-up in the unemployment rate as hiring freezes and job losses occur before new job occupations and roles are created. Fed Cook has expressed concern that AI is already impacting hiring for coders and also graduate entry jobs (here). Additionally, the NY Fed mean probability of finding a job in the next three months if one loses a job today is back down to COVID recession lows (Figure 1). However, data is not conclusive, with NFP establishment data showing no major job losses in AI sensitive sectors such as Information and Professional Services (here). Meanwhile, though consumer sentiment remains weak, this is more about cost of living concerns than fear that AI could reduce employment and wage prospects. It is also difficult to separate cyclical forces (slowdown and lower immigration) from structural AI influences.

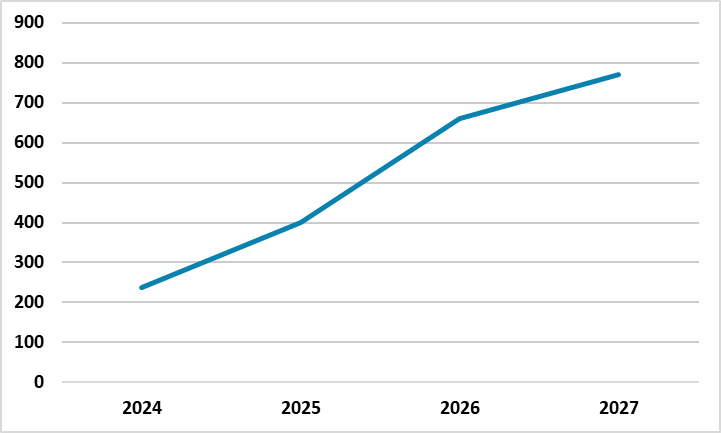

Figure 2: U.S. Hyperscalers Estimate CAPEX (USD Blns)  Source: Industry Estimates

Source: Industry Estimates

• Higher Then Lower Neutral Rate? Fed Jefferson has argued that current high investment demand for the AI buildout of semiconductors and datacenters means that the neutral rate could be pushed up due to increased investment demand. Additionally, the boom in U.S. datacenters has put upward pressure on electricity prices in certain states, while key commodity prices (e.g. copper) are being buoyed by the AI investment boom. Fed Barr (here) argues that the labor market data so far is consistent with a scenario of gradual AI adoption, which is slow to boost productivity and not impacting aggregate U.S. labor market conditions (with some evidence of labor reallocation/retraining within firms and also mixed evidence on more or less income inequality). Barr concludes that the evidence so far is that AI does not argue for lower policy rates and could boost real wages. This sits in contrast to Kevin Warsh view that the current rise in productivity is the most important aspect and this will deliver disinflation and argues for lower policy rates. Part of the growing Fed debate reflects timing and scale. The AI buildout boom is now, but some economists argue that the structural boost to productivity could still take 2-5 years. Not all areas of the U.S. economy are exposed to AI benefits, as manual work can only be replaced by humanoid robots which requires major advances in robotics and battery life. Fed Cook (here) has floated the idea that AI investment demand could boost the short-term neutral rate, but then productivity and job losses could reduce the long-term neutral rate! Secondly, the scale of impact remains uncertain. Though Fed Barr argues for a gradual AI scenario, he looks at two other scenarios including quick AI adoption that causes large scale job losses. This would be a huge adverse scenario, which could then cause a cyclical recession; stock market shakeout and sharp fall in the still overvalued USD as the Fed slashes policy rates!

• FOMC data dependence versus Warsh Forward Looking Fed. Thus different Fed officials will likely continue to have divergent views over the impact of AI on economy/inflation and the prospective policy path, as they seek to understand the timing and scale of AI impacts. This could be further complicated by Kevin Warsh’s view that the Fed is backward looking and needs to rely on forecasts to tilt towards a more forward looking policy setting given the lags of monetary policy. However, the majority of voting members on the FOMC are data dependent in their views, which means that policy setting will likely be dominated by incoming data rather than one to two years ahead forecasts. We do see consumption slowing down cyclically due to weaker income growth and this will likely deliver 25bps cuts from the Fed in June and September. We will also watch data closely to understand the dynamic impact of AI on economic/inflation and policy outlooks.

I,Mike Gallagher, the Director of Research declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.