Trump’s Fiscal Dominance

· Voting will be done by 12 FOMC members and while Kevin Warsh could mellow some centrists, 5 district Fed presidents and Barr/Jefferson are at the Fed until at least 2031. Warsh may merely bring interest rate cuts sooner from June or potentially engineer a small dip below the 3% neutral policy rate in 2026-27 rather than Trump’s dreams of a Fed Funds rate persistently at 1%. Additionally, Warsh persistent concerns about QE; Fed balance sheet size and it allowing reckless government borrowing suggests he may want to toughen the 1951 Fed-U.S. Treasury accord and avoid fiscal dominance. Warsh could be a rate dove, but not a balance sheet dove and is unlikely to fulfil Trump fiscal dominance wishes.

U.S. President Trump wants the Fed to cut interest rates to reduce government debt service costs, which is fiscal dominance of the Fed. Will his cunning plan succeed?

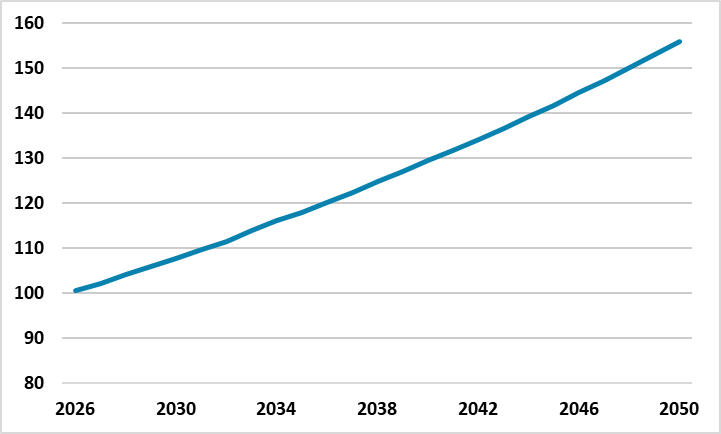

Figure 1: U.S. Federal Debt Held By The Public (% of GDP)

Source: CBO Long Term Projections (here)

Fiscal dominance of a central bank comes from difficulties in managing a large and rising government debt/GDP trajectory; large deficits and rising debt servicing costs. Is the U.S. approach a tipping point to fiscal dominance that could produce unexpected inflation/Fed Yield curve control and in the worst case monetary financing & debasement of the USD?

· Economics: Debt trends v USD reserve status. The U.S. debt held by the public is already high, but lower than France/Italy and Japan and also rising at a modest pace over the next 10 years from the new February 11 long-term projections (Figure 1). Combined with the USD reserve status, plus 2% real yields in the 10yr area, prospect that the GOP lose the House in the mid-term elections, this produces the view that debt sustainability is more of a 2030’s issue than 2020’s and fiscal dominance of the Fed is not a major near-term risk. However, the short average maturity of U.S. government debt (5.8 years from IMF Oct fiscal monitor) means that debt servicing costs are already 3.2% after the jump in yields since 2021 and set to rise to 4.4% of GDP by 2036 (Figure 2 for new CBO 10yr projections). This also means that the budget deficit edges back above 6% of GDP into the 2030’s, even with new CBO projections that custom duties will be USD3.45trn over the 10yr period to 2035 – which could be undermined by the Supreme court ruling on reciprocal tariffs. Additionally, Trump wants to fiscally dominate the Fed, as his call for dramatically lower interest rate is motivated also by a desire to reduce debt servicing costs to allow for fiscal space for new populist measures.

Figure 2: 10yr Federal Debt Held By The Public; Total Deficit and Net Interest Costs (% of GDP)

Source: CBO Medium Term Projections (here)

· Fiscal dominance risks. Fiscal dominance has occurred in EM economies and the risks were well documented by the benchmark BIS study in 2011 (here) and more recently in 2023 by an article from the St Louis Fed (here). First step is to weaken central bank independence and get the central bank to focus on fiscal financing, as well as inflation/employment. This can involve lower policy rates than on economic grounds alone. The second step can include making reserves non-interest bearing, capping deposit rates in the banking system and capping yield levels in the U.S. Treasury market (i.e. Fed yield curve control), which suppresses the nominal and real costs for U.S. Treasury financing. The Fed did this after WW2 until the 1951 Fed-U.S. Treasury accord boosted Fed independence and the pursuit of economic goals. The 3rd step is to produce unexpected inflation, which acts as an inflation tax on debt holders and that the central bank does not react to by tightening. The 4th step is to introduce the ugly sister of monetary financing of the deficit, either indirectly via persistent QE (beyond that consistent with the growth of nominal GDP) or outright monetary transfers by the Fed to the U.S. Treasury. Some investors fear a number of all of these steps on a road to monetary financing and eventual debasement of the USD. However, a number of reasons suggest Kevin Warsh Fed will not playout fully along these lines.

Limits to fiscal dominance under Warsh include

· Objective FOMC voters. The decision to reappoint the district Fed presidents until 2031 means that 5 of the 12 FOMC voters (4 rotating and NY Fed Williams) will follow orthodoxy assessments of the tradeoffs between employment and inflation, which the dots suggest means two more 25bps cuts in 2026 – we pencil in June and September. Trump may dream of seven Fed governors outvoting the district Fed presidents, but this is unlikely in 2026. Fed Barr and Jefferson serve to 2032 and 2036. Thus even if Trump replaced Cook (2038) and Powell decided to step down early (2028), 7 out of 12 members would be orthodox in their approach. Bowman and Waller are also doves, but do not appear to be in the mood to accept fiscal dominance of the Fed looking at their speeches and 2026-28 and long-term Fed Funds dots. Warsh influence will also depends on whether he tries to change the Fed quickly Maga/DOGE style or more measured by considered decisions, as the former could see resistance to Warsh on monetary policy decisions. Bessent has suggested taking time, but Trump is impatient.

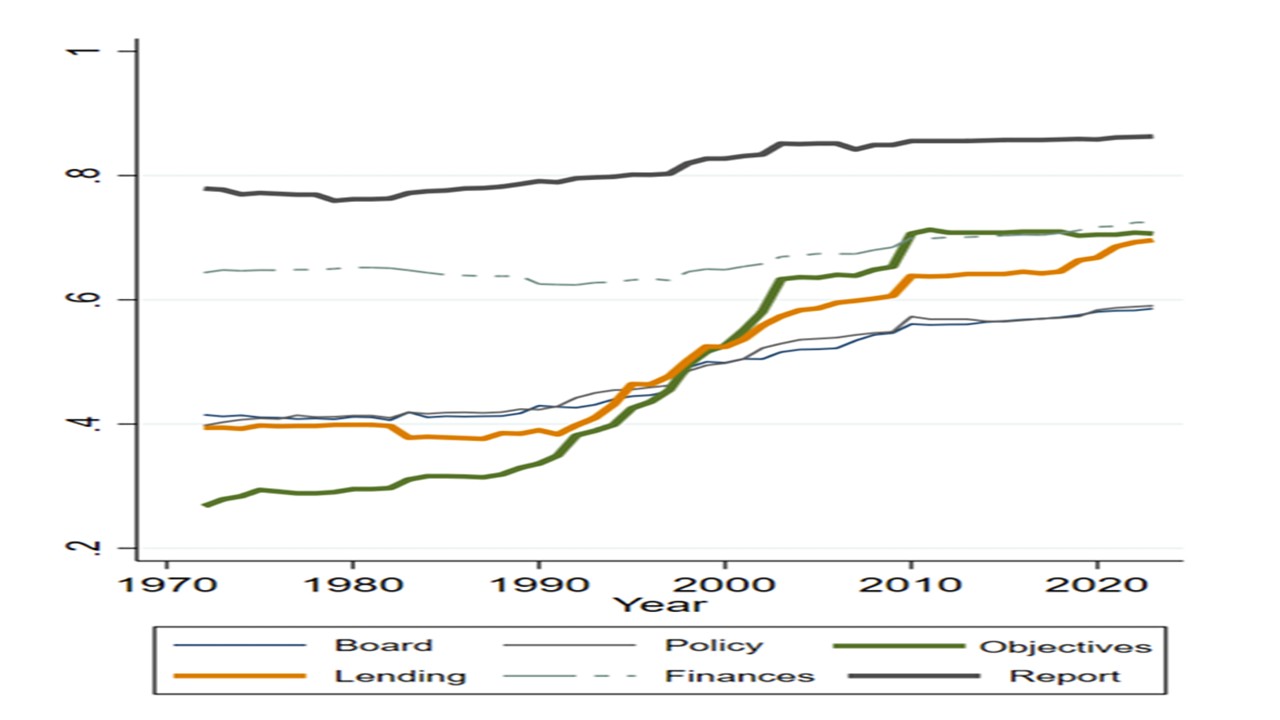

Figure 3: Dimensions of Central Bank Independence (%)

Source: ECB study (here)

· Warsh monetary policy changes and more dovish communications. It is certainly true that Warsh sounds more dovish than the dots would suggest and the Fed chair also has more influence over FOMC voting than his one vote. Additionally, Warsh appears to want to make the Fed more forward looking/staff model forecast based and less data dependent. Add in his arguments that AI is boosting productivity and disinflation; Bessent desire to scrap the dots and stop Fed district governors from speaking on monetary policy and communications/forward guidance could see the FOMC becoming more dovish. However, voting will be done by 12 FOMC members and while Warsh could mellow some centrists, it may merely bring interest rate cuts sooner or perhaps a small dip below the 3% neutral policy rate in 2026-27 – a hard landing for the U.S. economy could see sub 2% policy rates however. The real test for the Warsh Fed will be when economic conditions warrant a tightening of monetary policy, which is something that a fiscally dominated central bank would be reluctant to do. This might happen in 2028-29, but probably not 2026-27. Multi-year Fed independence could be softened on some dimensions of central bank independence, but this is unlikely to be a complete U-turn (Figure 3 shows the global improvement in central bank independence since the 1970’s)

· Warsh dislike of QE and monetary financing. Warsh is famous for his dislike of QE and large balance sheet size, which he fears boost asset prices and the 2nd Fed QE in 2011 prompted his resignation. Warsh has called for an update of the 1951 Fed-U.S. Treasury agreement and Warsh last year said that the agreement could “describe plainly and with deliberation” what the Fed’s balance-sheet size would be, with the Treasury laying out its debt-issuance plans. Additionally, he noted that the Fed (QE 1-3 and 2020) had violated the accord and allowed reckless government borrowing. Given Warsh past concerns on the size of the Fed balance sheet, Warsh could be looking to avoid a balance sheet increase in line with rising debt issuance i.e. guard against monetary financing. Additionally, given his comments on reckless government borrowing, it could be that Warsh wants to guard against fiscal dominance. It seems unlikely that Warsh want to play part of the fiscal dominance playbook and reintroduce yield curve control.

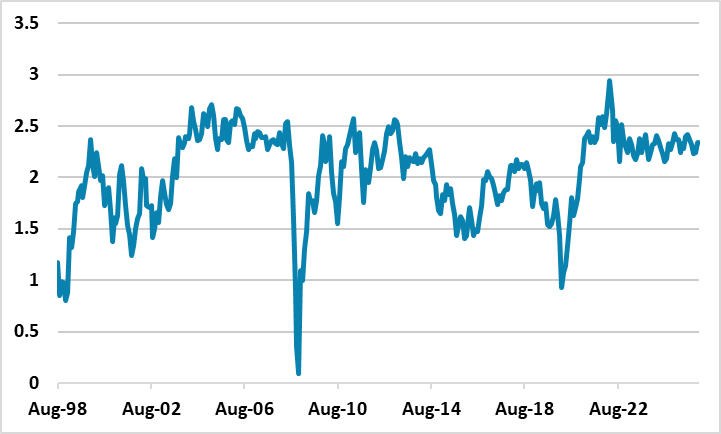

· Warsh and QT. Warsh long-term may also want to reduce the Fed balance sheet still further, but the FOMC consensus voted to stop QT last year and Warsh may not be able to build support for the idea of lower policy rates offsetting the effects of restarting QT. However, Warsh has also hinted at giving some control of the balance sheet to the U.S. Treasury, which would be fiscal dominance! The Senate confirmation hearing warrants careful review. One key indicator to watch throughout this period will be the 10yr breakeven inflation expectations, which has been dominated by macro rather than fiscal issues (Figure 4).

Figure 4: 10yr U.S. Breakeven Inflation Expectations (%)

Source: Bloomberg