Eurozone: Manufacturing Seeing Excess Supply Not Excess Demand

In Europe generally, but especially in the EZ, it will be manufacturing that will bear the brunt of the recent jump in energy prices, where industrial electricity prices even before the conflict started were among the highest globally. While high energy costs affect all sectors, manufacturing’s reliance on the likes high heat processes and high-volume electricity consumption makes it disproportionately vulnerable. However, while vulnerable, given the current relative state of demand and supply, manufacturing is far less so than four years ago, and also far weaker than services. This is important as it should help restrain goods price pressures and also thus temper any spill over effects both within manufacturing as well as into other sectors.

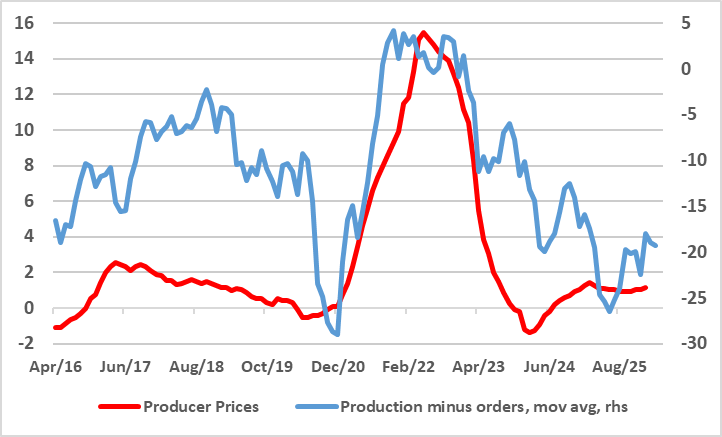

Figure 1: EZ Industry Supply-Demand Imbalance Opposite to Four Years Ago

Source: European Commission – PPI % chg y/y, Prod-orders is percentage balance

Assessing how the current energy price surge relates to that of four years ago when the Ukraine War started is all the rage at present and understandably so. Obviously, HICP inflation is relatively much lower and monetary and fiscal policy tighter. With this in mind, we did an analysis recently that showed how the EZ labor market is much looser now than in Feb 2022 (and even relative to the decade before the pandemic) with wage pressure second round effects likely to be less marked as a result. But another key area of difference is the state of the EZ manufacturing sector. This is all the more important as it is this good-making sector that will bear the brunt of the recent jump in energy prices, where industrial electricity prices even before this year’s conflict started were among the highest globally. While high energy costs affect all sectors, manufacturing’s reliance on heat-heavy processes and high-volume electricity consumption makes it disproportionately vulnerable to rising energy costs.

In this regard, EZ manufacturing is in a much weaker situation at present than four years ago, with a supply-demand imbalance almost the opposite of the situation then. With supply proxied by production and demand by orders, there now seems to be a clear current situation of the former very much higher than the latter unlike Feb 2022. This is shown in Figure 1 based on European Commission survey results of industry recent production trends and orders position. The bottom line is that amid this ‘excess supply’ position, manufacturers will find it more difficult to pass on higher costs both within the sectors as well as to others. Indeed, as Figure 1 also shows, the current state of excess supply is even more marked than pre-pandemic period when producer price inflation was hardly positive.

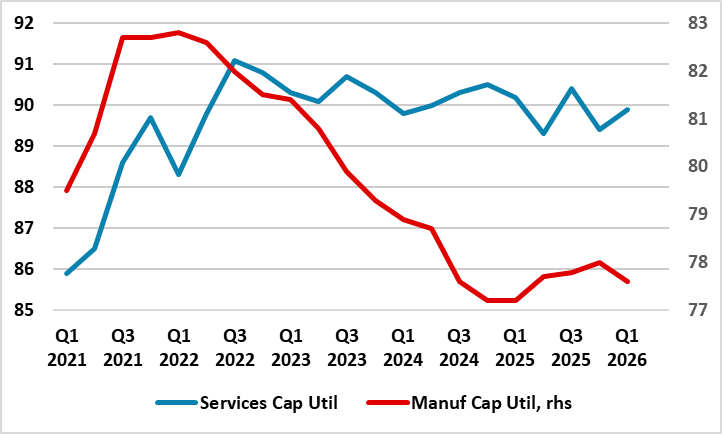

This backdrop is echoed in Figure 2 which shows capacity utilisation actually for both manufacturing and also for services. It very much shows that current factory sector utilisation is clearly lower than four years ago while that for services is broadly similar. Given that the energy price shock will hit manufacturing earlier and more severely than services, this is a better juxtaposition for the EZ economy to be in if second round price effects are to be minimalized.

Figure 2: EZ Industry Capacity Usage Has Fallen Markedly

Source: European Commission (%)

The orders- production imbalance may even be accentuated if the tariff-induced influx of Chinese exports continues to build, this very much evident in the fact that EZ non-energy goods inflation has been barely positive in the last two years. Admittedly, this has been countered by services inflation, which while having slowed, is still at a pace above that of the ECB’s overall inflation remit. But as the ECB assesses its policy options a key question arises; if the Council claims to have a symmetrical interpretation of its target where undershoots carry as much weight as overshoots, why has it placed more emphasis on services inflation being above 2% than goods inflation being near zero!