ECB: Not the Only Game in Town – But A Time for Hair Shirts?

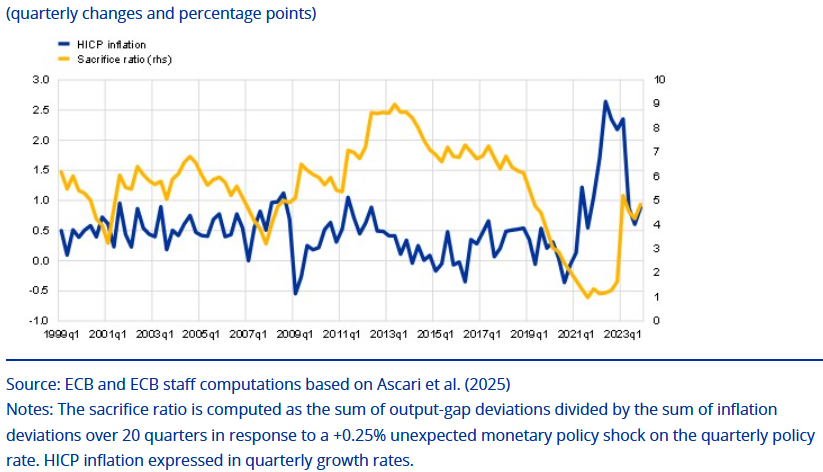

When hearing ECB Council policy thinking one can get the impression that it sees only a direct link from changes in its policy rate to inflation rather than the latter succumbing to a range of factors, this being the transmission mechanism. Most important of course is the economic damage that changes in policy rates may wreak, both in deterring spending and in affecting the costs and supply of credit. Well, a recent ECB blog, very much discusses the extent in which lost output has been a feature (albeit modestly so) in helping bring the HICP rate back to target in the last tightening cycle – involving a so-called ‘sacrifice ratio’. But this analysis seems skin deep, ignoring that many other factors helped reduce inflation once the first rate hike was put in place in July 2022. In other words, the ECB and its rates hikes were not the only game in town and were never going to be. We would also quibble with the blog’s assertion that when inflation is high, prices and wages adjust more flexibly, making it easier to bring inflation down without large overall output losses. Does this mean that we are to expect more economic damage from any even small rate hike that the ECB decides on in the near future – if so, will this feature in the ECB reaction function?

Figure 1: HICP inflation and Sacrifice Ratio Over Time

The ECB blog basically asserts that monetary policy in the EZ was particularly effective during the 2022-23 tightening episode. It asserts that it achieved rapid disinflation with limited output cost which reflected a stronger transmission to inflation relative to past monetary policy interventions, a more decisive monetary policy response to supply-driven shocks, and the continued anchoring of inflation expectations. We think this is almost arrogant in suggesting that a) the ECB rate hikes were the only factor involved and b) that the analysis does not comment on the extent to which the Council was culpable in allowing inflation to rise in the manner that then precipitated the conventional tightening cycle.

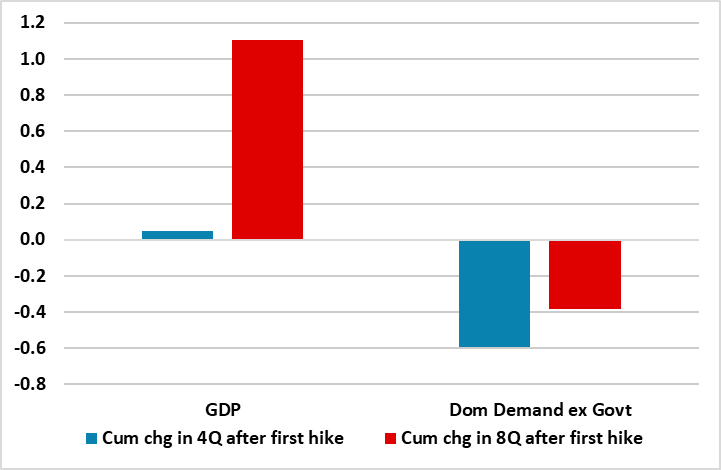

In terms of assessing how limited were the output costs, we would suggest that GDP may be far from the best measure. GDP growth in the year and two years after the first hike were buoyed by very strong government consumption and a marked fall in imports. As Figure 2 shows, while GDP overall was hit minimally in both the first and then eight quarters after the initial hike, domestic demand ex government fared far worse, this surely as, if not far more, important in shaping domestic price pressures.

Figure 2: Two Very Different Degrees of Economic Sacrifice?

Source; Eurostat, CE, ppt chg

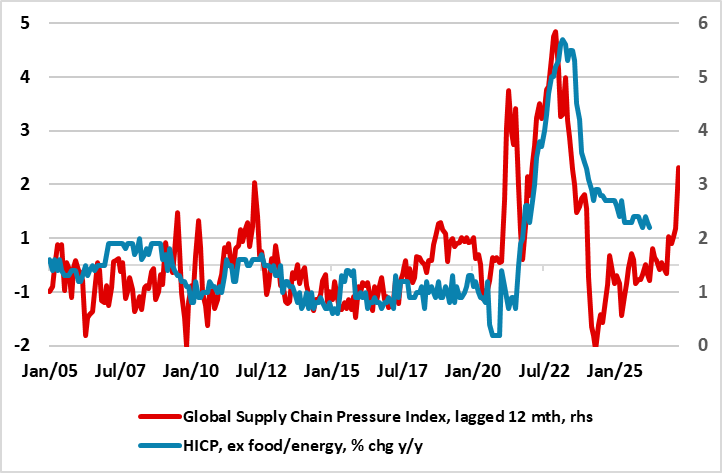

The blog and its simplification also make no attempt to ascertain the extent to which the GDP swings were demand and/or supply determined even though the sacrifice ratio does encompass an assessment of the change in the output gap. Indeed, as we have suggested repeatedly, it does seem as if global supply factor were both the main factor in causing the HICP inflation surge and then its fall – albeit with more recent data causing some more genuine upside inflation risks (Figure 3).

Figure 3: Global Supply Swings the Main Factor in Shaping Recent Inflation Swings?

Source; Eurostat, CE, ppt chg

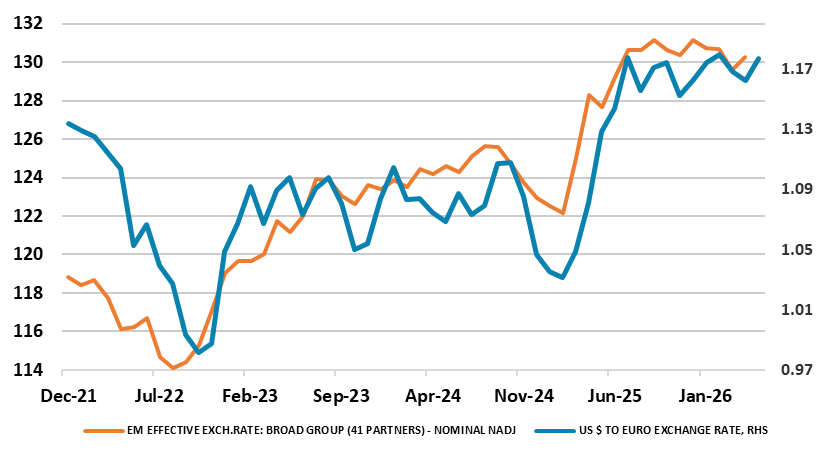

But there are other shortcomings. As suggested above, the ECB and it conventional rate hikes were far from the only factor at play. Half of EZ GDP are imports, highlighting the extent to which external factors such as global demand, supply chains and the exchange rate are key inflation factors. As for the exchange rate and only partly driven by the ECB’s conventional hiking cycle, the trade weighted euro rose some 10% in the first five quarters after he mid-2022 first rate hike (Figure 4). But this also ignores the impact of the unconventional tightening that the ECB undertook starting in H2 2002 as well as the growing unwillingness of banks to supply credit so that the tightening cycle saw a rise in the cost of credit but also a in its supply!

But the major gripe is the assertion in the blog is that ‘when inflation is high, prices and wages adjust more flexibly, making it easier to bring inflation down without large overall output losses’. This runs against economic orthodoxy, although there have been dissenters from this line of thinking too. Even so, it seems that lowering inflation from a high rate is generally considered to be harder and more economically painful than from a low rate. Several key factors explain why reducing high inflation is significantly more difficult and more painful: Firstly, there is the issue of price expectations; when inflation is high, consumers and businesses expect it to stay high. Workers demand higher wages to keep up with the cost of living, and businesses raise prices to cover those rising wage costs. This can create a wage-price spiral that wild be difficult to break without something that softens both demand generally and the labour market specifically. Secondly, central banks risk losing their credibility if they fail to act aggressively against high inflation.

Figure 4: A Stronger Euro Helped the Inflation Battle?

Source; Eurostat, ECB

Not only do we quibble with the blog’s assertion that when inflation is high, prices and wages adjust more flexibly, making it easier to bring inflation down without large overall output losses, we also try and understand the policy consequences. Does this mean that we are to expect more economic damage from any rate hike the ECB decides on in the near future – if so, will this feature in the ECB reaction function whose remit is solely based around inflation and (unlike the Fed) does not encompass employment considerations? Such considerations are all the more relevant now as a weak 0.1% q/q Q1 GDP release may continue through the rest of the year and with the downside risks posed by business survey data. Is the ECB starting to consider dressing in hair shirts?