EZ HICP Review: Core Rate Spikes as Upside Inflation Risks Return

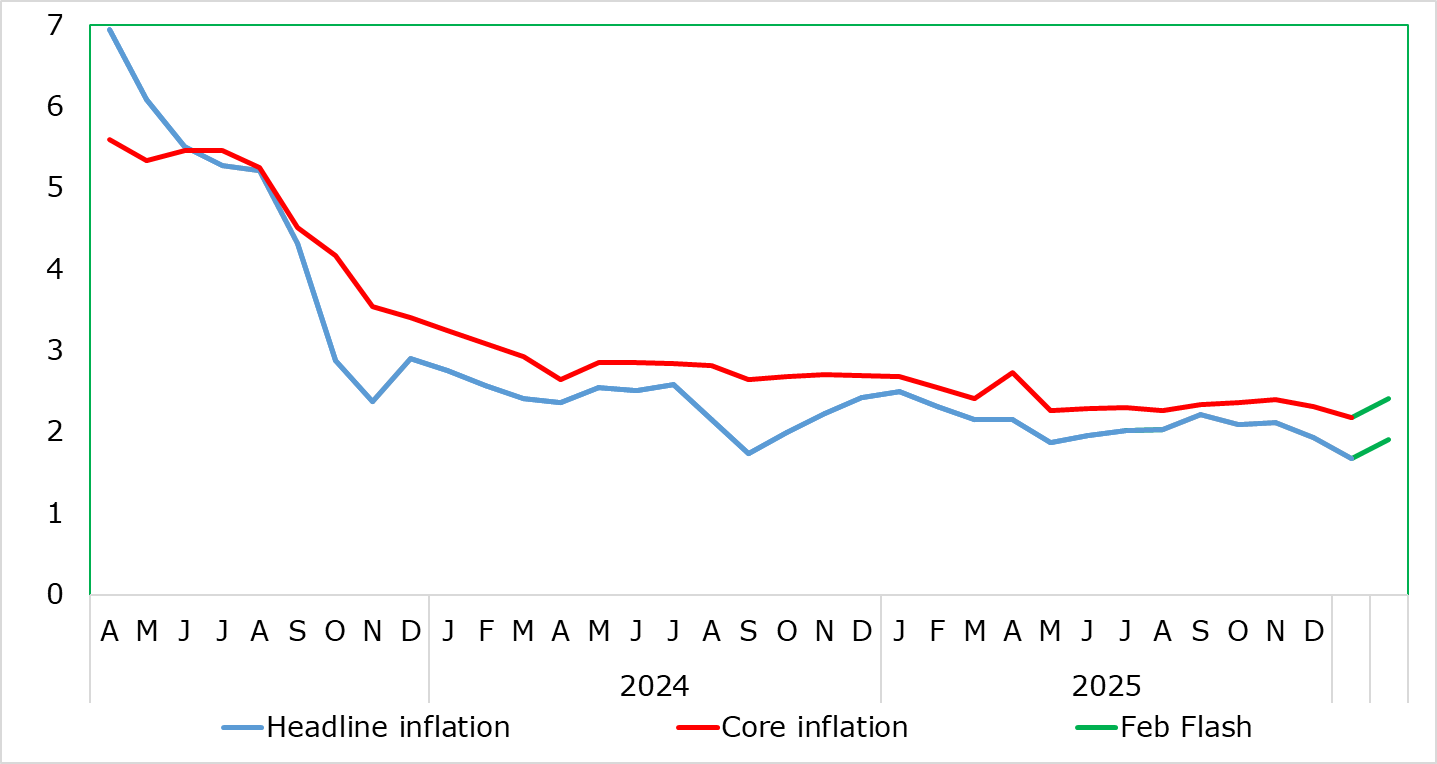

Having dropped to 1.7% in the January data, thereby matching expectations and the short-lived Sep 24 outcome, it is likely especially in view of the Middle East conflict that the headline HICP rate may not be any lower through this year and into next. Indeed, we headline rate rose 0.2 ppt to 1.9% in the February flash only partly due to energy. Even more unexpectedly, the core rose similarly to a 3-mth high of 2.4%. That reflected a fresh rise in services inflation and less weak non-energy goods prices.

Of course, even though the data is for a recently as February, the Middle East conflict is changing what has been a clear disinflationary outlook, certainly for headline inflation. Given volatility in energy prices and uncertainty about conflict goals and timing, amending the EZ outlook at this juncture is fraught with risks causing hesitation. This is very much underscored by two recent scenario analysis that tried to assess the impact of an energy price supply (as opposed to demand) shock. They show markedly different outcomes. Even so, we suggest that the likes of the ECB look through the likely spike in prices in the near-term as it its updated forecasts due later this month may imply.

Figure 1: Headline and Core Higher

Source: Eurostat, CE, % chg y/y

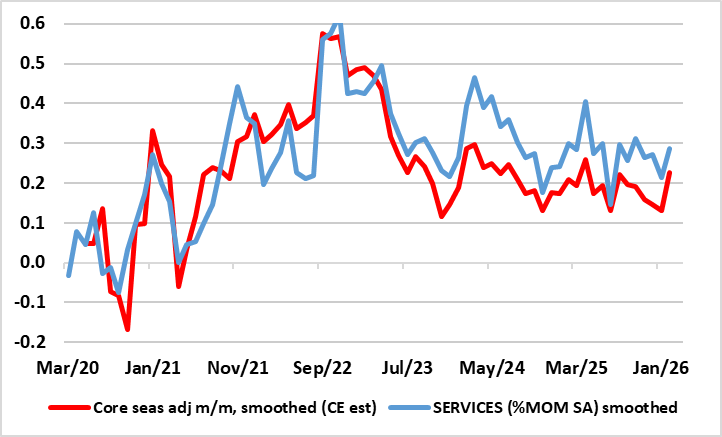

Diehard hawks at the ECB remain focused on the recent rise, and now more apparent resilience, in services inflation - this despite still target-consistent outcomes in more short-term seasonally adjusted m/m data (Figure 2) and a rise in February probably driven by hotel costs through the recent Olympics in Italy. Even so, hawkish thinking seems to have reverberated within the ECB and seemingly prompted the upward revisions made in December to the 2026 HICP outlook. Regardless, over and beyond a justified more amenable reassessment of services inflation, we think the hawks will have to come to terms with other component of core inflation, namely non-energy industrial goods which accounts for one third of core HICP (services the other 2/3) which we think will still succumb to the joint impact of Chinese export dumping and the higher euro.

Figure 2: Services Inflation Still Near Target Already?

Source: Eurostat, CE, m/m seasonally adjusted

Of course, it is now the case that markets are starting to assess the what the likely economy and policy impact of the current Middle East conflict may be. In this regard, it is important to differentiate between energy price rises caused by demand shocks compared to spikes stemming from supply. As for policy from the likes of the ECB, scenario analysis it has offered of late will be important in understanding its probable thinking in regard to supply shocks. In particular, analysis published in December 2023 sought to estimate the repercussions of a an energy price spike resulting from a Middle East conflict in which about one third of the oil and gas in transit via the Straits of Hormuz was disrupted, contributing to a tightening in the global energy markets. As a result, a synthetic energy price index (which combines oil and gas prices) was assumed to be 64% above the baseline in the first year if the estimate and to remain 36% above the baseline two years later. Such a scenario is an extreme one, with the assumed oil and gas supply shock more persistent than historical supply shocks.

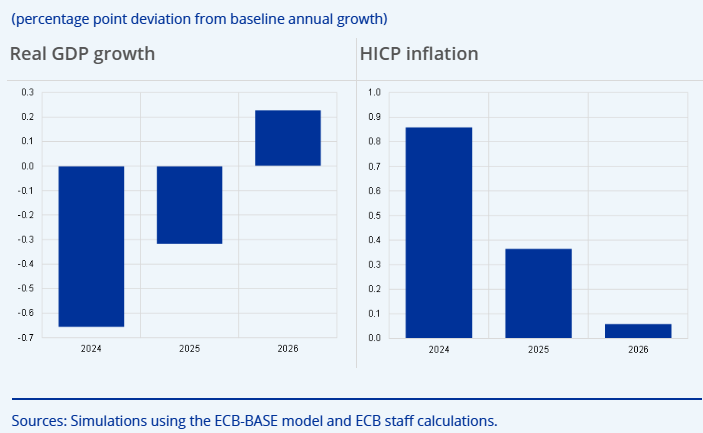

Figure 3: ECB Estimate of Impact of Energy Shock Scenario on EZ real GDP growth and HICP Inflation

As a result, the impact on global economic activity and EZ foreign demand was seen to be considerable with the latter hit by 1.2 ppt in 2024 relative to the December 2023 baseline. As with the global economy, the higher oil and gas prices and heightened uncertainty was seen to directly impede EZ economic activity so that real GDP growth was estimated to be 0.7 ppt lower in the first year (2024) and 0.3 ppt lower in the following year (2025) than in the December 2023 baseline projection, but was then estimated to rebound in the third year (2026) as uncertainty effects unwound (Figure 3), with HICP inflation 0.9 ppt in 2024 and 0.4 percentage points in 2025, mainly on account of higher global energy prices.

Other analysis is possibly more pertinent and more worrisome given its more sizeable estimated impact of a supply shock. Scenario analysis by the European Commission in 2022 examined an adverse scenario characterised by oil and gas prices being 25% above the baseline assumptions over the forecast horizon as it analysed the impact on the EZ of the Russian invasion of Ukraine. This causes stagflationary forces. Annual GDP growth rates for year one and year two are estimated to be 1¼ and ½ ppt below the projections in the baseline forecast, respectively. Inflation is estimated to stand ¾ and ½ ppt above the forecast baseline.

We would expect fresh and more detailed scenario analysis from the ECB when it updates its forecast at the Council verdict on Mar 19!