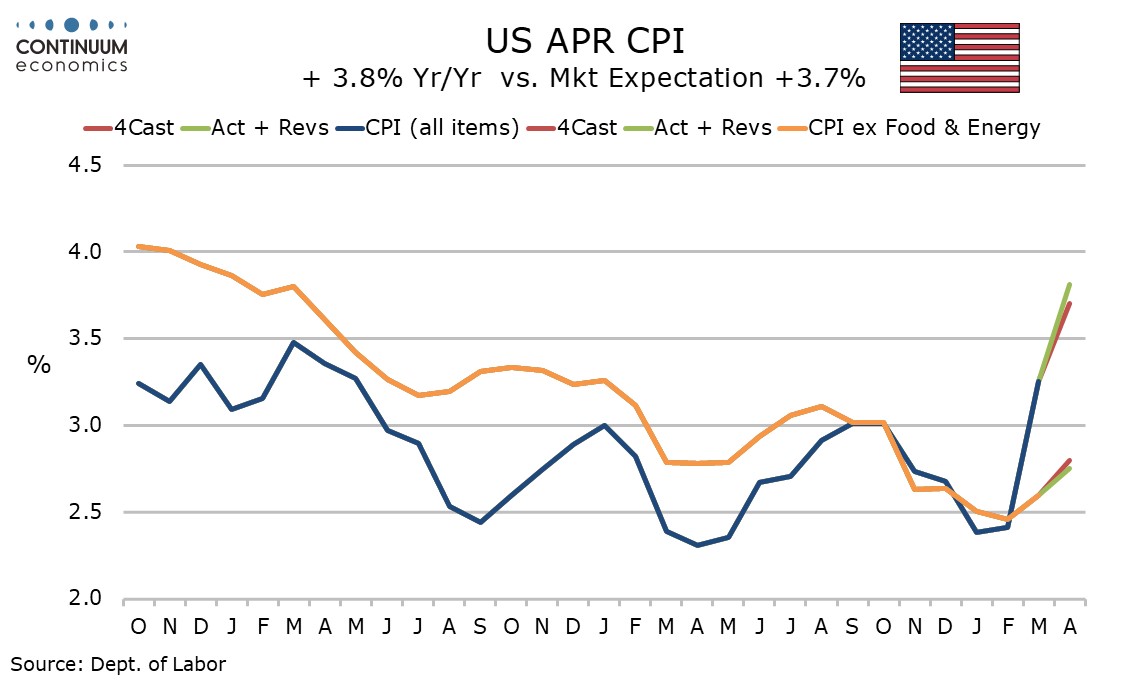

U.S. April CPI - Subdued ex food, energy and what looks like one-time strength in shelter

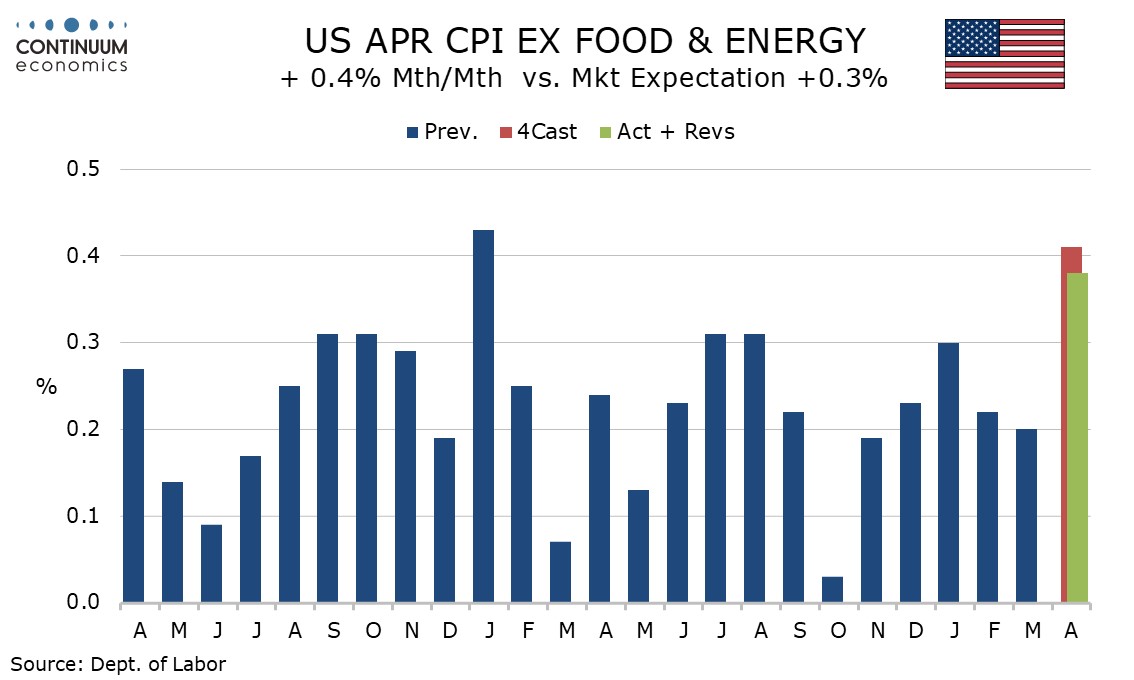

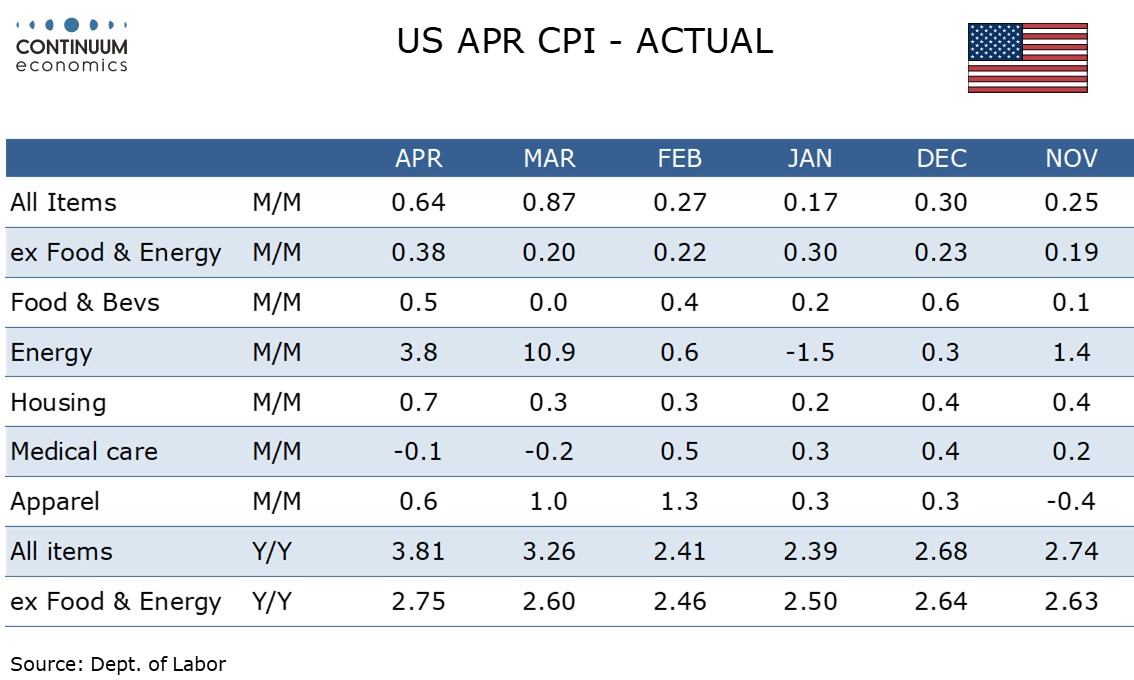

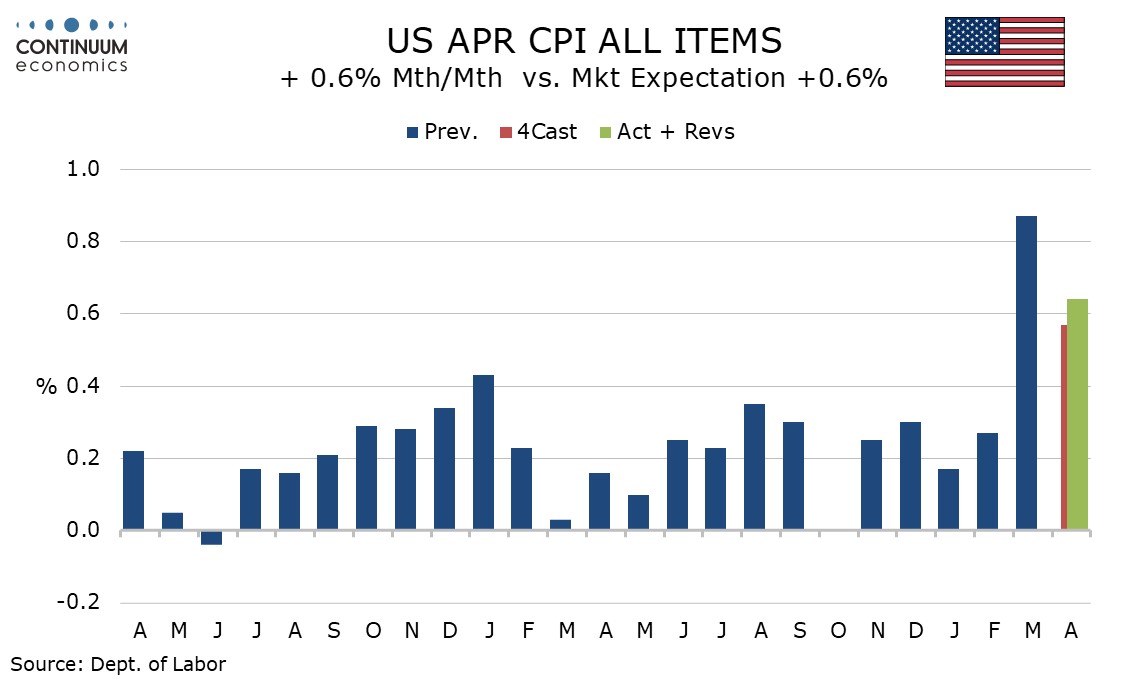

April CPI is only marginally stronger than expected on the core rate, up by 0.4%, 0.376% before rounding, and the data not alarming outside of a one-time distortion in housing. The headline gain of 0.6% was as expected, and here the rise was a little firmer at 0.64% before rounding.

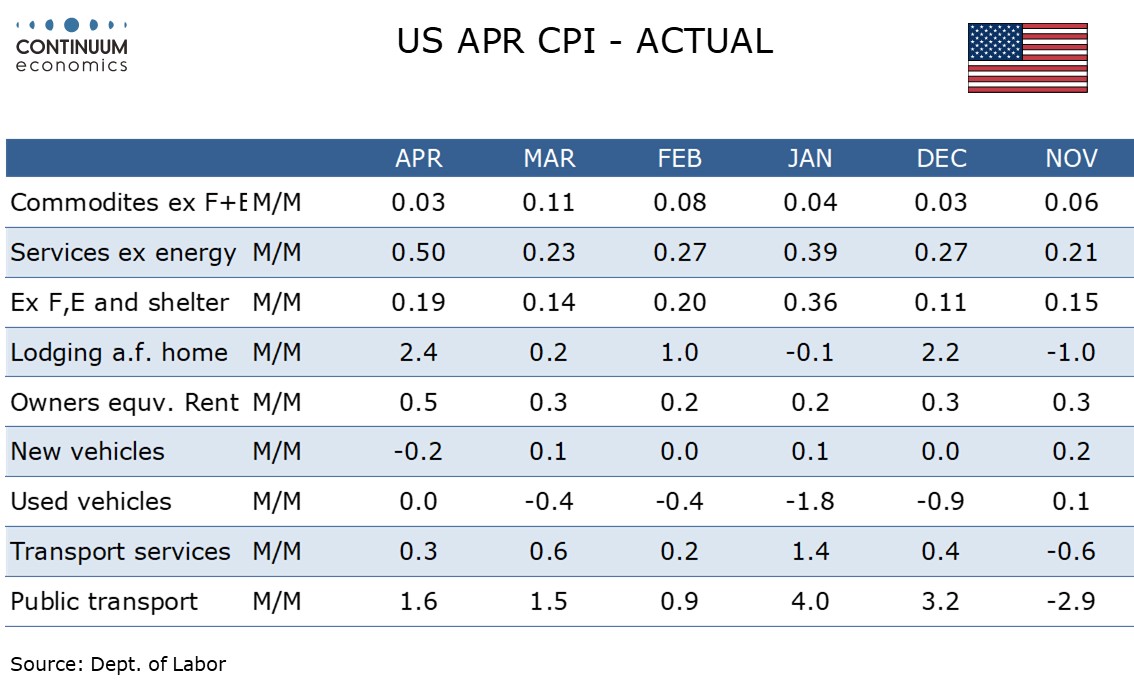

Shelter rose by 0.6%, double March’s pace, with owners’ equivalent rent up by 0.533%, its highest before rounding since April 2023. Here some measurements are taken every six months and with there having been no October 2025 CPI due to the government shutdown this month’s data is effectively boosted by the missing October 2025 data. Shelter got an additional boost from a 2.4% increase in lodging away from home, a volatile component.

CPI ex food, energy and shelter rose by a moderate 0.19% before rounding, in line with recent trend. Air fares rose by 2.7% after a 2.6% increase in March, implying some feed through from energy prices, but these are not exceptional gains for this volatile component. Transport services saw a moderate 0.3% increase, restrained by a fall in car and truck rental and with most subcomponents subdued.

Commodities ex food and energy were unchanged. Used autos were flat after four straight declines but new autos saw a 0.2% decline. Medical care commodities fell by 0.4%, a second straight decline (medical services were flat). Apparel however saw a third straight gain, rising by 0.6%.

A 5.4% rise in gasoline led a 3.8% rise in energy though energy services were quite firm too with a rise of 1.6%. Gasoline prices look set to rise further in May. Food with a 0.5% increase may also be showing signs of impact from the Middle East, with risk of more to come.

Yr/yr growth of 3.8% from 3.3% is the highest since May 2023. Ex food and energy yr/yr growth picked up to 2.8% from 2.6% in march and 2.5% in January and February, reaching its highest since 3.0% in September, just before October’s missing month.