BoE Preview (Mar 19): MPC Agree to Disagree?

The rate cut that seemed partly flagged by the narrow vote against easing in early February now looks highly unlikely this month. Indeed, it is also likely that the four who dissented in favor of cutting last time around will vote with the majority in favour of no change. But while the MPC as a whole will not have to reveal too much about any shift in policy bias given that it does not have to provide updated forecasts until its April 30 meeting, the individual member views will show continued divides. Indeed, while February’s four dissenters will suggest they are probably deferring easing, some of the more hawkish members may be more open about considering hikes to guard against or combat any rise in inflation expectations that they think may trigger a fresh rise in wage pressures. We consider such thinking to be misplaced given the labor market is loosening and where companies face a fresh squeeze on profits. Given financial conditions, we still see at least two more 25 bp rate cuts ahead but now deferred to no sooner than late summer.

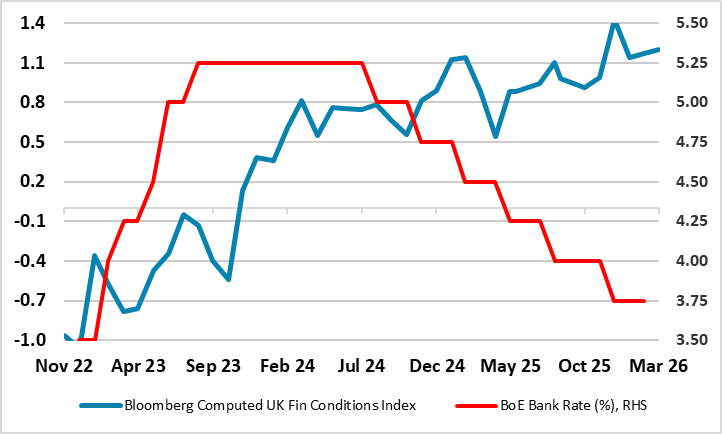

Figure 1: Bank Rate and Financial Conditions Diverge (% and level)

Source: Bloomberg, BOE, Continuum Economics

Indeed, we have long argued that the weak economy and labor market allied to tight(er) financial conditions would build the case for three 25 bp cuts in 2026 to 3.0%, the latter being a level that the dovish camp on the MPC would consider to be neutral. And a cut as soon as this month seemed very likely given that an easing was averted by just one vote within the nine-strong MPC in February, this partly reflecting downgraded GDP and inflation projections with the latter seen by the BOE falling to target by mid-year and largely staying there out to 2028.

Of course, the backdrop and outlook has changed and we have highlighted several scenarios as to how the Middle East conflict will pan out. But under what we consider the most likely outcome (which envisages limited further fighting) we see oil and gas prices largely falling back to the pre-war levels within a year. Even so, this still results in UK CPI inflation being some 0.5 ppt higher than otherwise, ending this year at 2.5%. There may be upside risks to this outlook but we note both the moderate weighting of energy in the CPI basket (6%) and the possibility that fiscal measures may be put in place to alleviate the impact – at least for households.

We are also sceptical about meaningful second round effects occurring. Indeed, even if inflation expectations rose further (to date market based measure have risen more in the near-term with those for the longer term stable) this is unlikely to result in higher wage pressures give the current loose state of the labor market and the likely squeeze on profit margins forms may now face. This will be a reflection of an economic backdrop that may avoid recession but narrowly so and where GDP growth may be as low as 0.5% this year, ie almost half the BoE’s pared-back projection made last month. This reflects already weak demand. As a result, we see CPI inflation falling back to (if not below) target in H2 2027.

Such updated forecasts are something the BoE will not need to do at this juncture, instead awaiting more details and data ahead of it next formal projection on April 30. But it too will very probably offer scenarios, probably adding to the two alternatives it has recently focused on, namely the current central picture which envisages the risks to inflation from weaker activity alongside one that encompasses more inflation persistence. Indeed, a third scenario based around a supply shock is possible.

Admittedly, this may not paper over clear(er) divides that may be seen in the individual member views that the BoE now offers after every MPC meeting. This is likely to see the hawks focus on added inflation persistence risks and the doves more on downside real economy hazards, though with neither camp departing from a view that policy should be left on hold until more clarity about the length, breadth and repercussions of the conflict are available. But we lean more to the dovish side, not least given weakness already evident in the economy which as suggested above partly stem from global factors but also tight financial conditions.

In this regard, while the MPC suggests that it has reduced the restrictiveness of policy, we think this is a complacent, if not misplaced, analysis. Instead, we argue that the monetary policy’s impact encompasses more than just the official policy rate, also taking in bond rate, spreads and the exchange rate. Indeed, a barometer of financial condition actually suggest a more restrictive backdrop is still unfolding even given the drop in Bank Rate (Figure 1). This is partly backed up by the recent BoE Agents survey in which small firms still report that ‘high street bank credit is not available’. Although very much less certain about the timing given current events, we therefore still see at least two more 25 bp rate cuts ahead but now deferred to no sooner than late summer and may extend into 2027.