BoE Review: A Fragile MPC Truce?

Very clearly, the BoE kept rates on hold with no dissents as it understandably waits for more information about the length, breadth and repercussions of the Iran war. The individual MPC member statements (as expected) showed diverging views as to the extent and reaction of what are now unfolding risks. But the MPC at least put to one side, the previous easing bias which pointed to further easing, instead reviving a more neutral stance, being ‘ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term’. The MPC minutes made clear that this is symmetric that policy may have to be more or less restrictive depending on the economic impact. What is notable is that this energy shock is justifiably viewed as being different to that of 2022, occurring at a point when the economy is operating with a margin of spare capacity. We think this very much reduces the chances of second round effects.

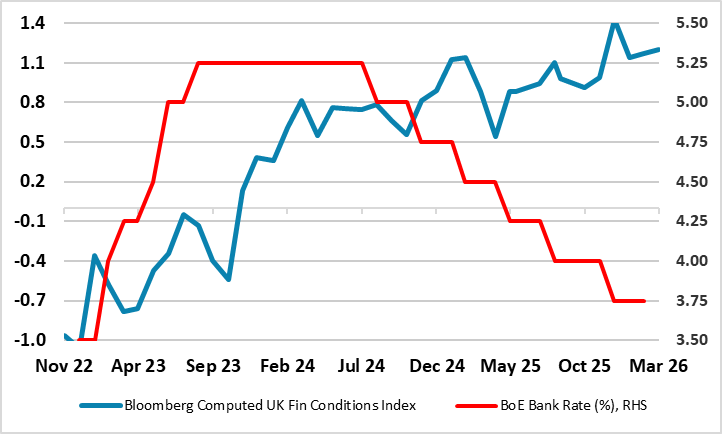

Figure 1: Bank Rate and Financial Conditions Diverge (% and level)

Source: Bloomberg, BOE, Continuum Economics

Given ever tighter financial conditions (Figure 1), which received several mentions in the BoE updates, we still see at least two and probably three more 25 bp rate cuts ahead but now deferred to starting no sooner than late summer and now extending into 2027. This is based on our baseline view of a 4-6 week Iran war and energy prices coming down from Q2. Very clearly, some of the more hawkish members may in the short-term become more open about considering hikes to guard against or combat any rise in inflation expectations that they think may trigger a fresh rise in wage pressures. In this regard, the April 30 BoE meeting will be important as it will present more formal forecasts and alternative scenarios.

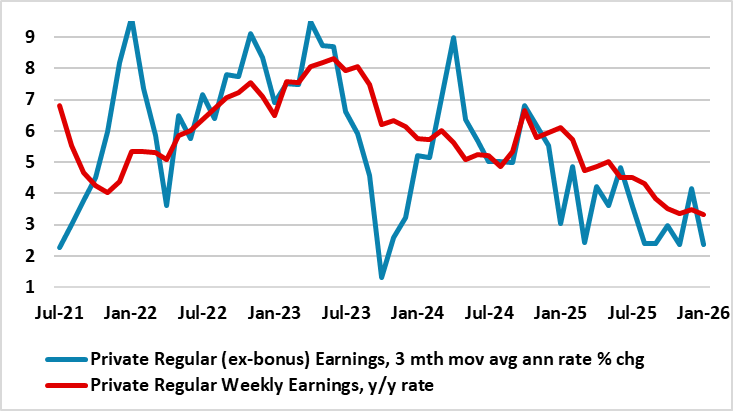

We consider such hawkish thinking to be misplaced given the labor market is already loosening and where companies face a fresh squeeze on profits. BoE Bailey’s individual comment noted downside and upside risks. Moreover, we concur with the risk that household and business confidence could deteriorate, further weighing on demand causing and reflecting a more rapid or larger rise in unemployment. These factors could widen the output gap somewhat, potentially constraining second-round effects, the latter already tempered by the pre-war backdrop which has been soft enough to have seemingly delivered a much softer wage pressures (Figure 2) to rates consistent with the BoE inflation target.

Figure 2: Weaker Wage Pressures Increasingly Evident?

Source: ONS, CE

Of course, the backdrop and outlook has changed and we have highlighted several scenarios as to how the Middle East conflict will pan out. But under what we consider the most likely outcome (which envisages limited further fighting) we see oil prices largely falling back to the pre-war levels within a year but gas prices falling back more slowly. Even so, this still results in UK CPI inflation being some 0.5 ppt higher than otherwise, ending this year at 2.75% but probably peaking above 3%. There may be upside risks to this outlook but we note both the moderate weighting of energy in the CPI basket (6%) and the possibility that fiscal measures may be put in place to alleviate the impact – at least for households.