Eurozone: Even Tighter Corporate Credit Standards Continues and More Loans Applications Rejected

Given the ever clearer fall-out from the conflict in the Gulf, it was hardly a surprise of even tighter credit standards (Figure 1), thereby merely accentuating trends in the four previous Bank Lending Surveys (BLS). At least as far as firms and especially consumers seeking credit are concerned, the BLS again underscores that banks are rationing, if not out rightly curbing, the supply of credit (NB; the BLS noted a further net increase in the share of rejected loan applications – Figure 2). As such, the latest BLS both corroborates and continues an ever worrying pattern, namely weakness in corporate credit demand and supply and which suggest ever more clearly that banks are increasing lending standards to firms, and seemingly not just to those exposed to the export sectors. The backdrop therefore looks like EZ firms and consumers are not just facing an increase in the cost of credit but also a reduction in its supply. To us this very much underscores that the ECB therefore needs to reassess its complacent view of the monetary as well as the real economy backdrop, particularly regarding credit dynamics as this is only accentuating tight(er) financial conditions.

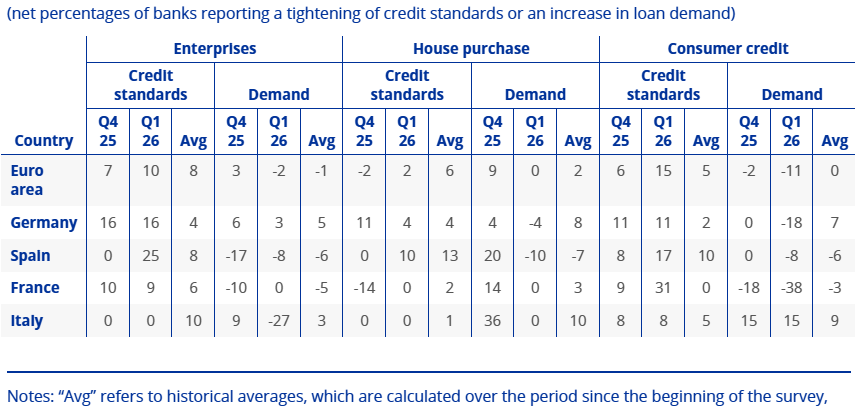

Figure 1: BLS Sees Broadly Tighter Credit Standards and Weaker Loan Demand

Source: ECB - Latest BLS results for the largest EZ countries

This week is an important and busy one in terms of updating the EZ monetary backdrop and outlook. Wednesday sees official money and credit data, but where today’s BLS provides hints as to where lending and borrowing trends may develop. In this regard, the BLS offers concerning messages and chimes with yesterday’s ECB-compiled survey on the access to finance of enterprises (SAFE) due which provides information on developments in the financial situations of firms and the availability of external financing. In other words, the BLS offers insights into how lenders are thinking while the SAFE offers similar insights but into how borrowers are thinking. As for the latest SAFE results, these showed a continued tightening in firms’ overall financing conditions in the first quarter of 2026, a trend observed consistently across firm sizes.

This very chimes with the April BLS. This reported that banks tightened credit standards across all loan categories, driven by higher perceived risks and lower risk tolerance to a degree where credit standards for both firms and consumer credit are above long-term averages (Figure 1). In addition, banks expect to tighten credit standards further in the current quarter, influenced by geopolitical tensions, energy developments, and higher funding costs. These insights into supply come alongside demand insights with that from both firms and households expected to decrease, resulting from reduced financing for fixed investments, lower consumer confidence, and decreased spending on durables. Indeed, as Figure 1 also shows loan demand is clearly weaker than average across all loan categories. Regardless, the data very much suggest that where banks are lending, it is increasingly on the basis of having collateral, something backed up in the BLS which suggests that nearly half of EZ banks use securitisation to grant new loans, manage credit risk and enhance liquidity and funding, relying on non-bank financial entities to purchase securitised loans

More troubling, banks reported a further net increase in the share of rejected loan applications across all loan categories, particularly for firms and with a much more marked net increase for consumer credit, this also probably a reflection of bank’s collateral priorities. Even so, the extent of rejected loans is well above recent and pre-pandemic averages. The ECB reaction on Thursday to all of these monetary updates will be interesting – to put it mildly!

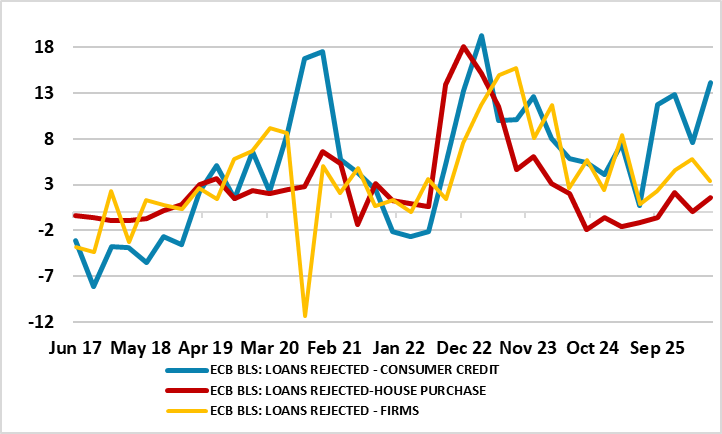

Figure 2: Loan Rejection Rates Rising and Above Long-Term Averages

Source: ECB - share of rejected loan applications relative to all loan applications in that loan category

Last time around the tighter credit conditions, let alone the increase in rejected loan applications was largely ignored. It may do again this week, but the thrust of the BLS, including an acknowledgment of rising effective interest rates, merely reinforces our view of tightening financial conditions. Indeed, it is worth noting that while banks reported only a moderate rise in credit standards for lending to banks, the fact that more and more loan applications are being rejected is surely the ultimate sign of reduced credit supply!

And this assumes that changes in policy rates have been fully passed on by banks to borrowers, something that does not seem to have been the case during the most recent easing cycle. Indeed, while the ECB discount rate (now down to 2%) is some 2 ppt below the peak last seen in mid-2024, the effective cost of borrowing for firms has fallen by only 1.7 ppt while that for household by a puny 45 bp!