Big EM: Diverging Fiscal Trends

· EM government bond spreads are controlled as 2nd round inflation effects are likely to be less than 2022, due to less buoyant domestic demand/slacker labour markets and less global supply chain pressure ex oil/oil products. Brazil is expected to cut rates and others will likely not hike, but rather pause in H2 2026. However, multi-year fiscal consolidation remains key, which is important for India/Mexico and S Africa. It is a swing factor in Brazil given the October presidential election, but cumulative BCB easing can narrow the spread versus the U.S. in 2027. China nominal and real yields are too low, but this is likely to continue with financial repression from China authorities, and investors risk aversion in the wake of the residential property bust.

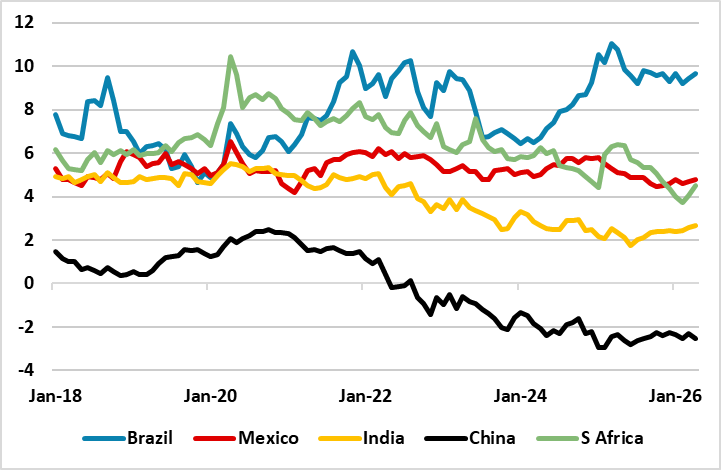

EM government bond spreads versus U.S. Treasuries have fluctuated during the Iran war, but without major widening. What are the future prospects?

Figure 1: 10yr EM Government Bond Spreads versus U.S. Treasuries (%)

Source: Datastream/Continuum Economics

Big EM’s have different exposure to energy imports from the Gulf, with China and India dependent and the other nations less exposed and also having domestic energy sources to call upon. China also has huge commercial and strategic stockpiles of oil/a surge in EV usage that is a diversifier from oil transport products and a switch from LNG toward coal fired powered stations. India with low stockpiles is vulnerable and will see CPI inflation ratchet up to 5% later in the year once the dampening effect of subsides becomes less noticeable. However, the big five EM countries are not warning of rate hikes, given that the 2nd round effects are expected to be small. Unlike in 2022, domestic demand is not strong/labor markets are looser/global supply chain conditions ex Gulf is much better. Indeed, the Brazilian and Mexican central banks have cut rates since the Iran war started, given the dominance of domestic disinflation over the risk of higher energy prices for transport. This is one reason why 10yr government bond spreads are currently similar to the outbreak of the war – S Africa did see a widen of spreads in March, but this was profit-taking after a superb narrowing in 2025.

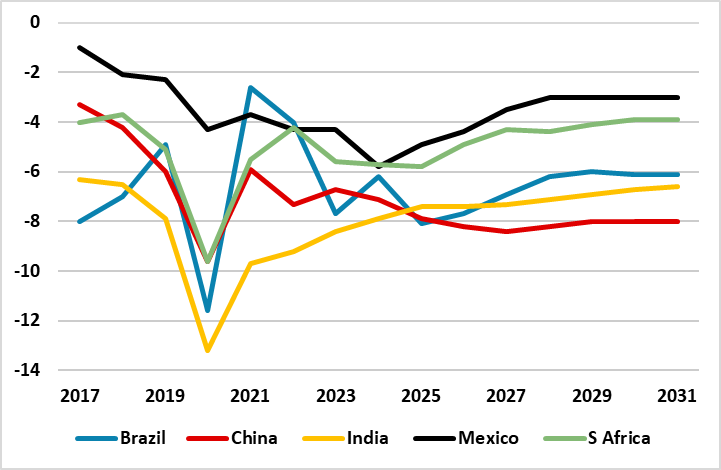

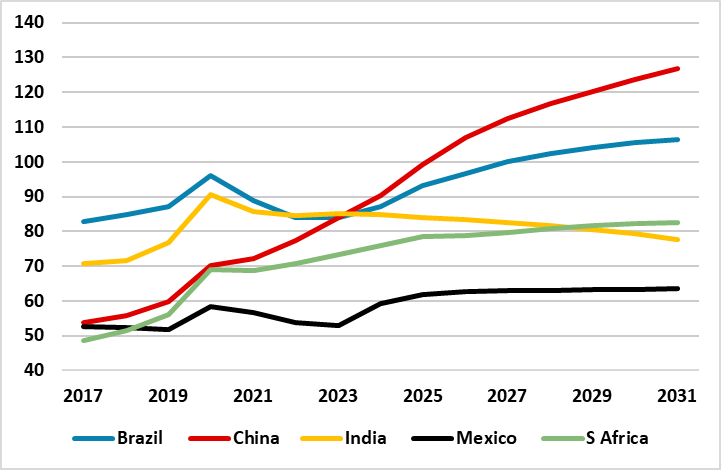

The other key feature is the attitude of investors toward big EM’s. India and Mexico have picked up foreign interest from global asset manager playing for a yield pick-up versus DM government bonds. India high nominal GDP trajectory in the coming years means that the government debt/GDP trajectory is gently falling over a multi-year period (Figure 3). Mexico has a lower general government debt trajectory and a more controlled budget deficit than other EM’s (Figure 2) or the U.S.

Figure 2: Big EM’s General Government Budget Deficit/GDP (%), 2017 - 2031

Source: IMF April 2026 Fiscal Monitor

S Africa has made some improvement in its budget deficit trajectory, which has pleased rating agencies and foreign investors. (Note: S Africa has secured its first credit upgrade in two decades late 2025 after S&P Global Ratings lifted the country’s sovereign ratings by one notch to BB on the back of reforms and growing fiscal revenue). While this is good, the coalition government’s cohesion is key to keeping a primary surplus and this hard-won fiscal credibility. The government debt/GDP ratio is still high and any weakening of fiscal credibility could mean higher government debt/GDP in the coming years. This is not our baseline as political space exists in 2026 with the next election in 2029, but the domestic politics needs to be monitored particularly due to frictions between the coalition parties.

Brazil has scope for yield spread to narrow versus U.S. Treasuries in 2027, but the next 6 months are restrained by the approach of the October presidential election. Flavio Bolsonaro is now tied with Lula in 2nd round polls, and this could mean a more market friendly government after the October election but also potential fiscal slippage by the Lula administration. BCB also wants to see what happens in fiscal policy, which argues for further gradual rate cuts through the remainder of 2026 to 12% i.e. a further 250bps of policy rate cuts. This could end up steepening the Brazil 10-2yr curve, but could still see some narrowing of the still very large nominal and real yield spreads versus the U.S.

Figure 3: Big EM’s General Government Debt/GDP (%), 2017 - 2031

Source: IMF April Fiscal Monitor

China’s low government bond yields reflect two domestic forces. Firstly, China’s authorities moral suasion to buy new central and local government debt helps financial repression. This is despite the surge of general government debt in recent years, which exceeds all other big EM’s (Figure 3). It used to be that central government debt was a moderate proportion of general government debt, with the rest mainly local government and LGFV debt that paid high interest rates. However, the Yuan10trn consolidate of LGFV debt, plus ongoing large fiscal deficits (Figure 2) is increasing the proportion of central and local government debt. This is not impacting Chinese central government bond pricing yet, due to pressure from domestic authorities. The 2nd issue is the risk aversion of some investors in the China economy is depressing the nominal and real yields of China government bonds. This risk aversion is a function of the structural bust in the residential property market. Though tier 1 cities are seeing less adverse residential property markets in 2026, the situation in tier 3 cities remains of one of excess housing inventories. No signs exist of a major bottom in the national China residential property market and this suggest the risk aversion could drag on and suppress China government bond yields.