U.S. February CPI - Core rate has slowed, but inflation not yet defeated

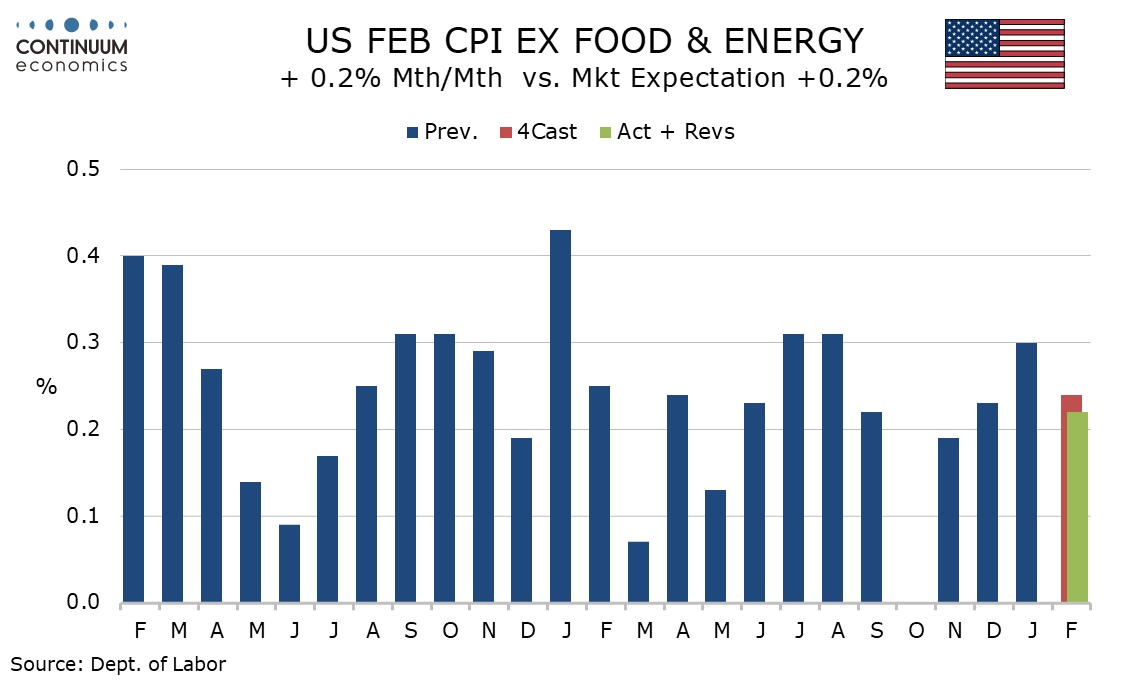

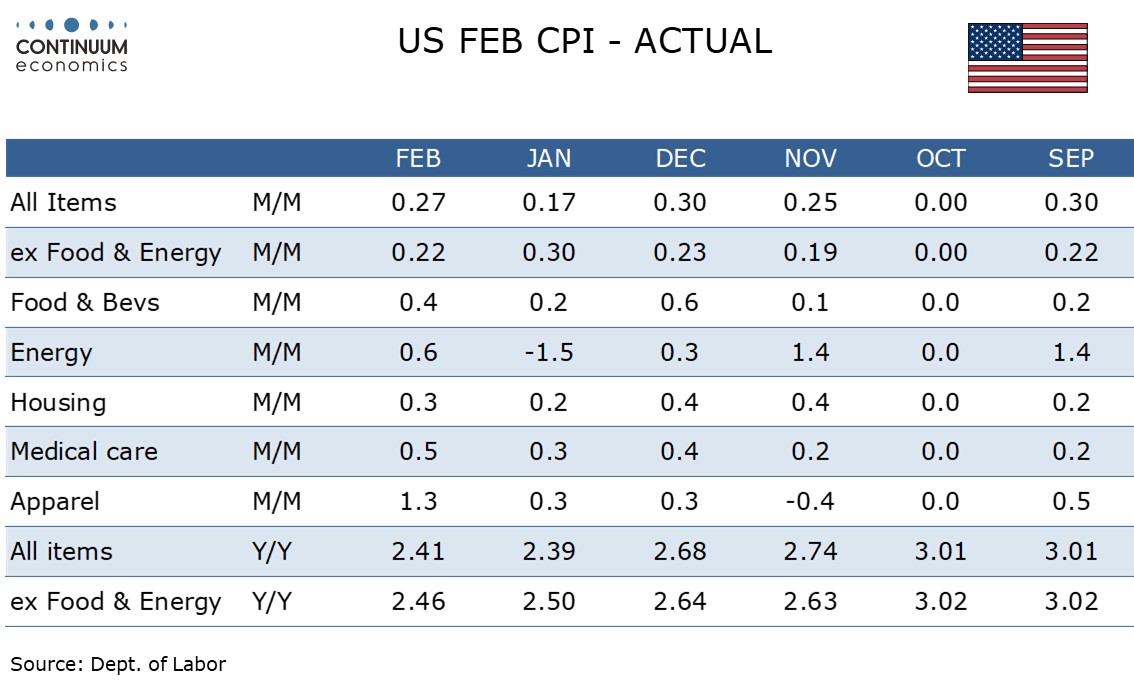

February CPI is in line with expectations at 0.3% overall, 0.2% ex food and energy, with the respective gains before rounding being 0.267% and a reasonably subdued 0.216%. Yr/yr rates are unchanged at 2.4% overall and 2.5% ex food and energy. The data is not alarming but inflationary pressures remained above target even before the latest oil price spike.

Energy rose by 0.8% with gasoline up by 0.6% with a strong rise looking assured in March. Within the energy detail there was also a surge of 11.1% in fuel oil after a 5.7% January decline. Food was on the firm side of trend, rising by 0.4%.

Commodities less food and energy rose by 0.1% after two flat months. Used autos remain a restraint but less so, falling by 0.4% after declines of 1.8% in January and 0.9% in December. Apparel saw a strong month at 1.3% but information technology commodities fell by 3.1%.

Shelter less energy rose by 0.3% after a 0.4% increase in January. Air fares remain firm rising by 1.4% though significantly less than January’s 6.5%. Overall transport services rose by a modest 0.2% with auto insurance falling by 0.3%, extending a 0.4% January decline. Shelter was subdued at 0.2% despite a 1.0% increase in lodging away from home but medical care services increased by 0.6%.

Yr/yr rates before rounding showed the overall pace marginally higher at 2.414% from 2.386% but the core rate slowing to 2.457% from 2.504%. This is the slowest ex food and energy pace since March 2021.

Usually, core CPI outperforms the core PCE price index but recently core PCE prices have moved ahead of core CPI, in part on strength in the PPI components that contribute to core PCE prices. Core inflation has fallen, but the Fed cannot declare victory yet.