U.S. October CPI - A more balanced report

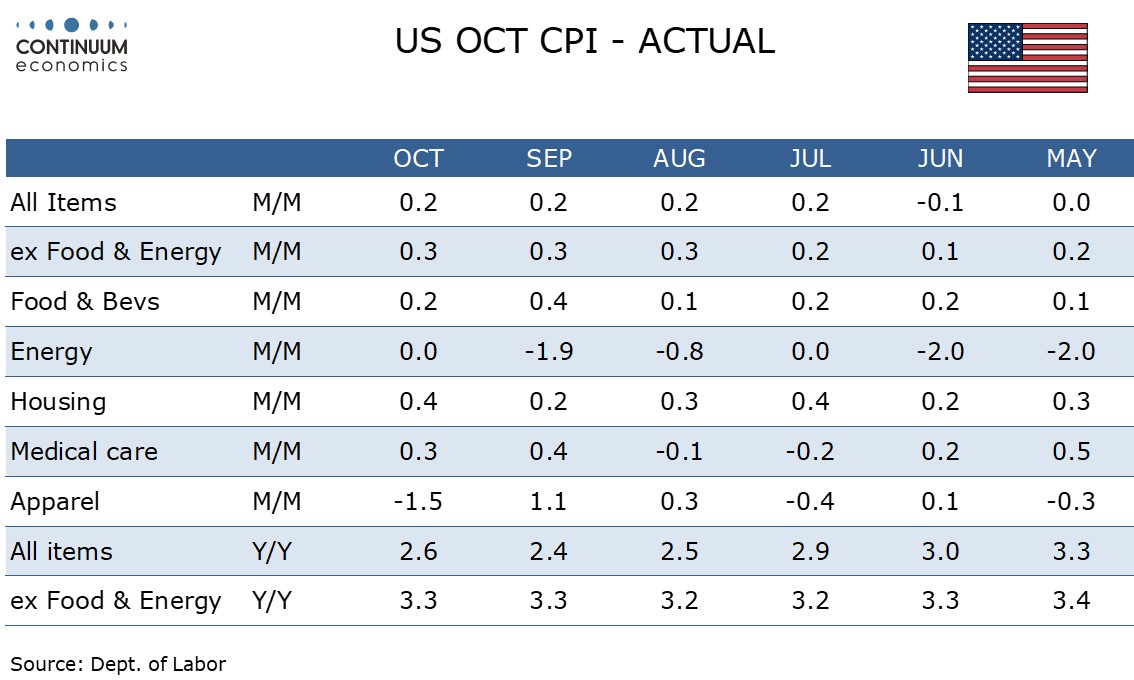

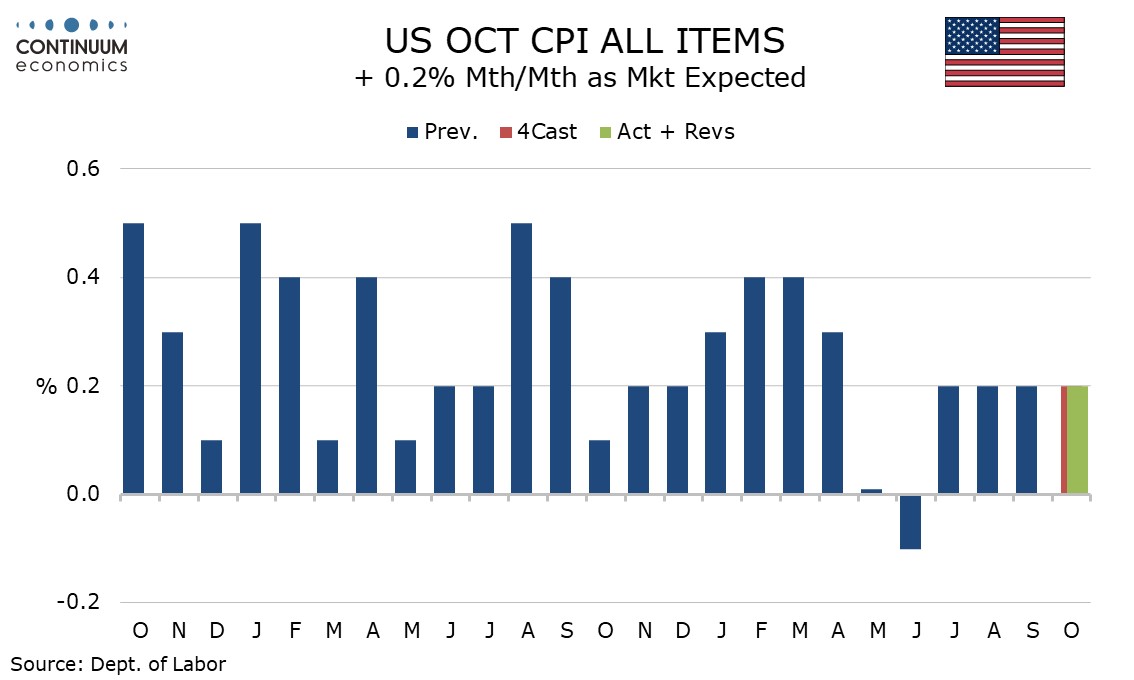

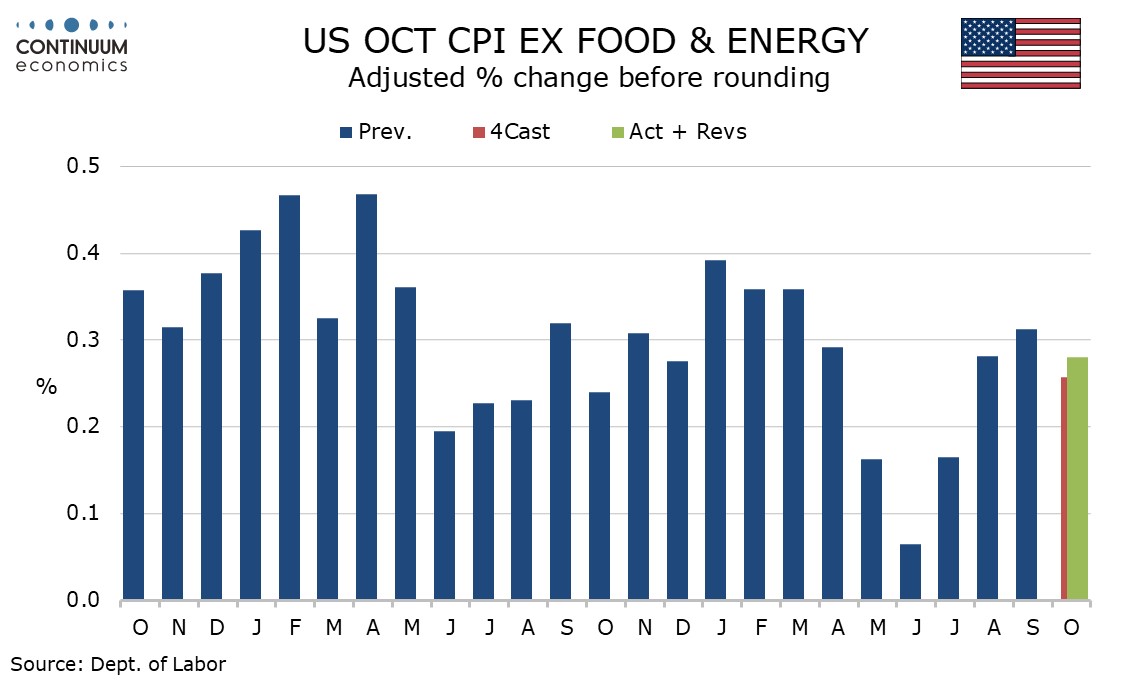

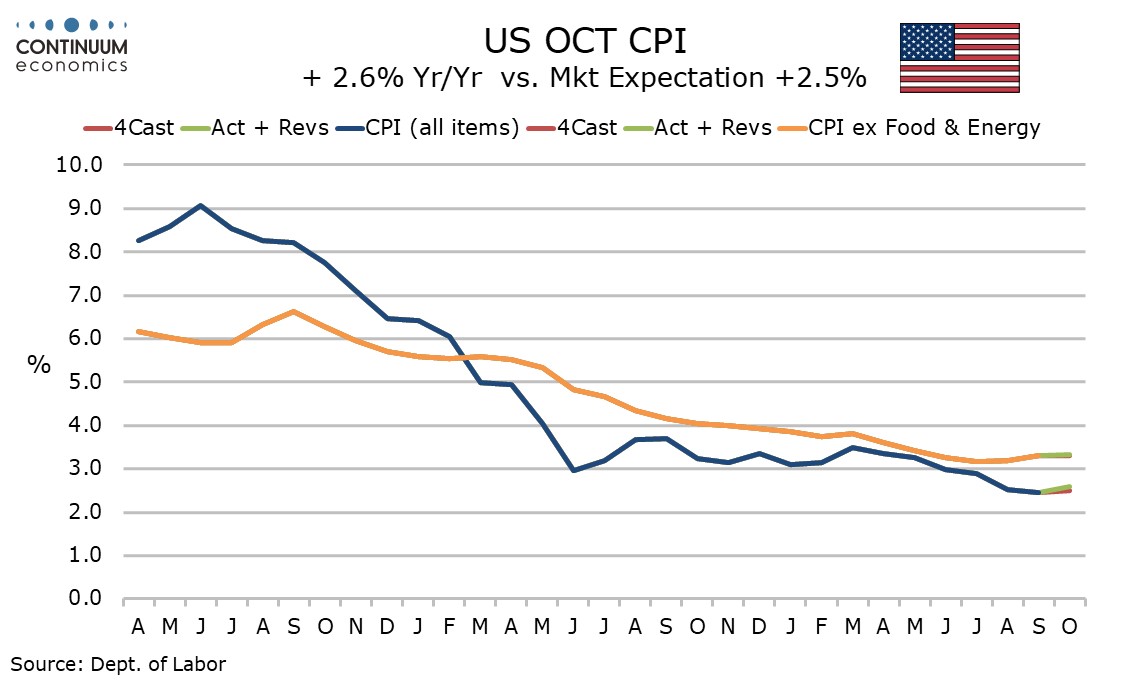

October CPI has seen the fourth straight rise of 0.2% overall and the third straight rise ex food and energy of 0.3%, both on consensus. Before rounding the gains were 0.24% and 0.28% respectively, the latter slower than September’s 0.31% but in line with August’s. The data leaves the December FOMC decision dependent on future data, with November’s employment report and CPI both due before the meeting.

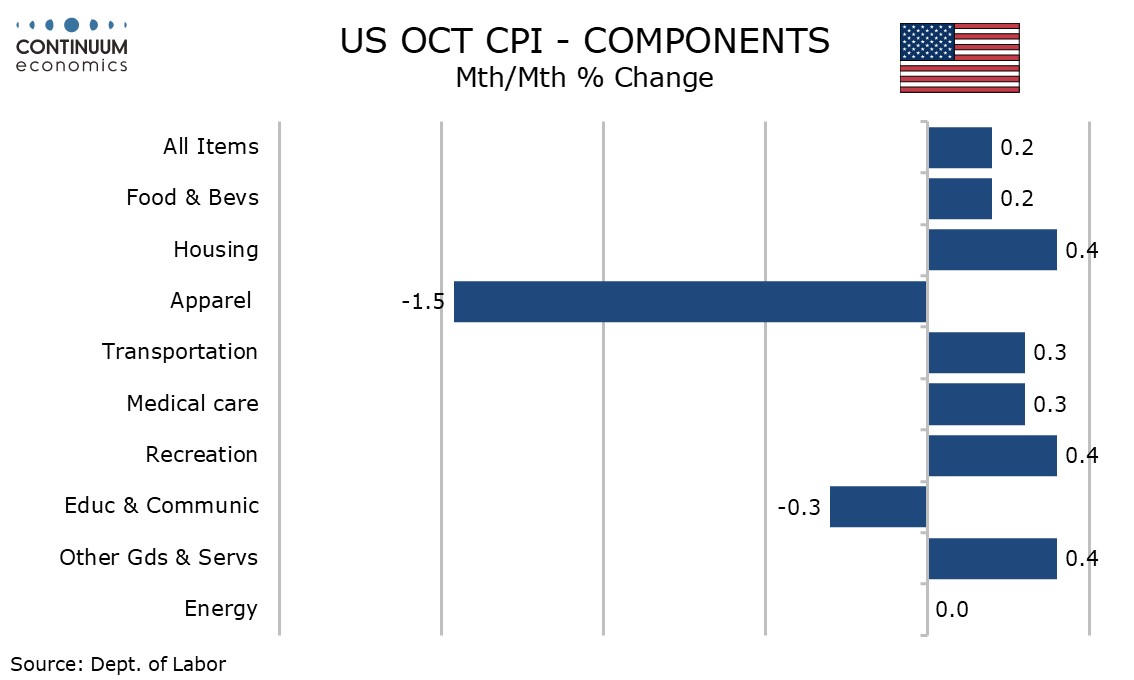

Energy prices were unchanged with a rise in electricity offsetting a dip in gasoline. Food rose a modest 0.2% leaving the overall outcome only marginally below the core before rounding. Commodities less food and energy were unchanged and appear to be stabilizing after recent declines. Services less energy with a 0.3% increase were on the low side of recent trend. The picture is becoming more balanced.

The commodities data was restrained by a 1.5% decline in apparel in a correction from a 1.1% increase in September, and the main reason why October’s core rate was slightly softer than September’s. Used auto however saw a strong 2.7% increase and deflation in that sector, a significant factor in recent slowing, appears to have run its course.

The commodities data was restrained by a 1.5% decline in apparel in a correction from a 1.1% increase in September, and the main reason why October’s core rate was slightly softer than September’s. Used auto however saw a strong 2.7% increase and deflation in that sector, a significant factor in recent slowing, appears to have run its course.

Airline fares remained firm with a 3.2% increase. Despite this transportation services slowed to a 0.4% increase from 1.2% in September largely due to auto insurance falling by 0.1% after a 1.2% September rise. Owners’ equivalent rent rise by 0.4% after a below trend 0.3% in October corrected a 0.5% increase in August. Lodging away from home, often a volatile sector, matched owners’ equivalent rent with a 0.4% increase.

Airline fares remained firm with a 3.2% increase. Despite this transportation services slowed to a 0.4% increase from 1.2% in September largely due to auto insurance falling by 0.1% after a 1.2% September rise. Owners’ equivalent rent rise by 0.4% after a below trend 0.3% in October corrected a 0.5% increase in August. Lodging away from home, often a volatile sector, matched owners’ equivalent rent with a 0.4% increase.

There is a reasonable balance between above trend and below trend components in this report, contrasting August when housing was above trend and most components subdued, and September when housing corrected lower but broader based strength was seen. The data is probably going to be seen as fairly neutral at the Fed, neither raising nor reducing confidence of a move back towards target, though the core rate is still too high to be consistent with target.

There is a reasonable balance between above trend and below trend components in this report, contrasting August when housing was above trend and most components subdued, and September when housing corrected lower but broader based strength was seen. The data is probably going to be seen as fairly neutral at the Fed, neither raising nor reducing confidence of a move back towards target, though the core rate is still too high to be consistent with target.

The yr/yr ex food and energy rate is unchanged at 3.3% and has been either 3.2% or 3.3% for the last five months, meaning a stalling of downward progress. The key to whether progress resumes will come when strong data in Q1 2024 drops out. Overall CPI edged up to 2.6% from 2.4% due to year ago weakness in energy.

The yr/yr ex food and energy rate is unchanged at 3.3% and has been either 3.2% or 3.3% for the last five months, meaning a stalling of downward progress. The key to whether progress resumes will come when strong data in Q1 2024 drops out. Overall CPI edged up to 2.6% from 2.4% due to year ago weakness in energy.