U.S. April Employment - Resilience should keep easing off the near term agenda

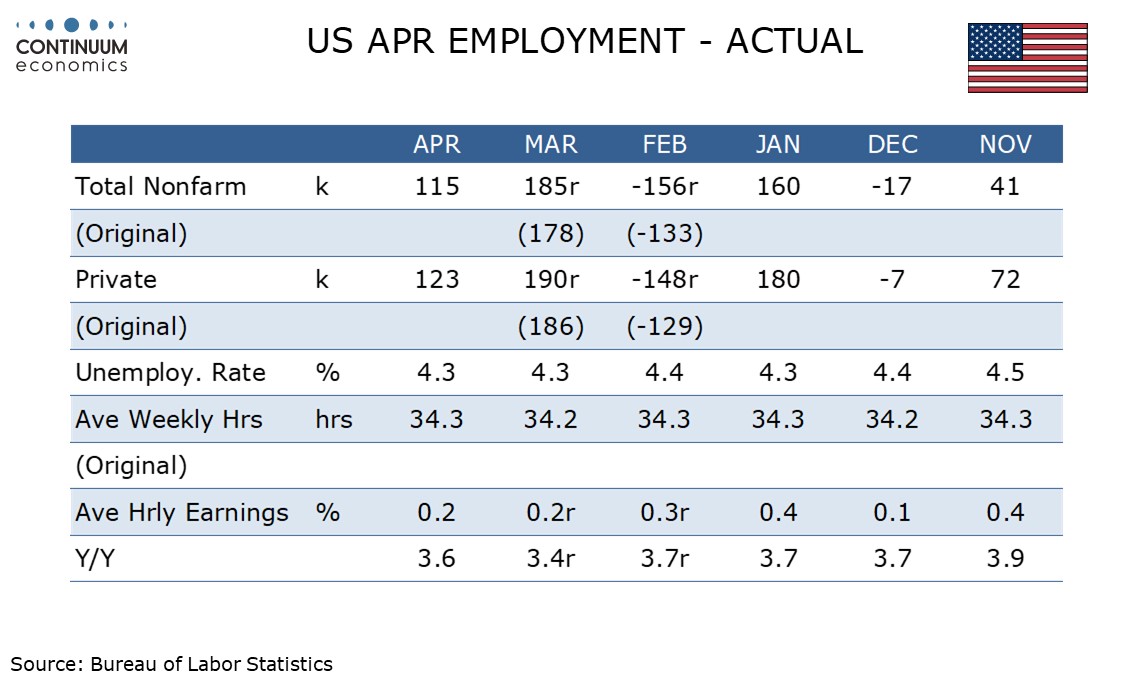

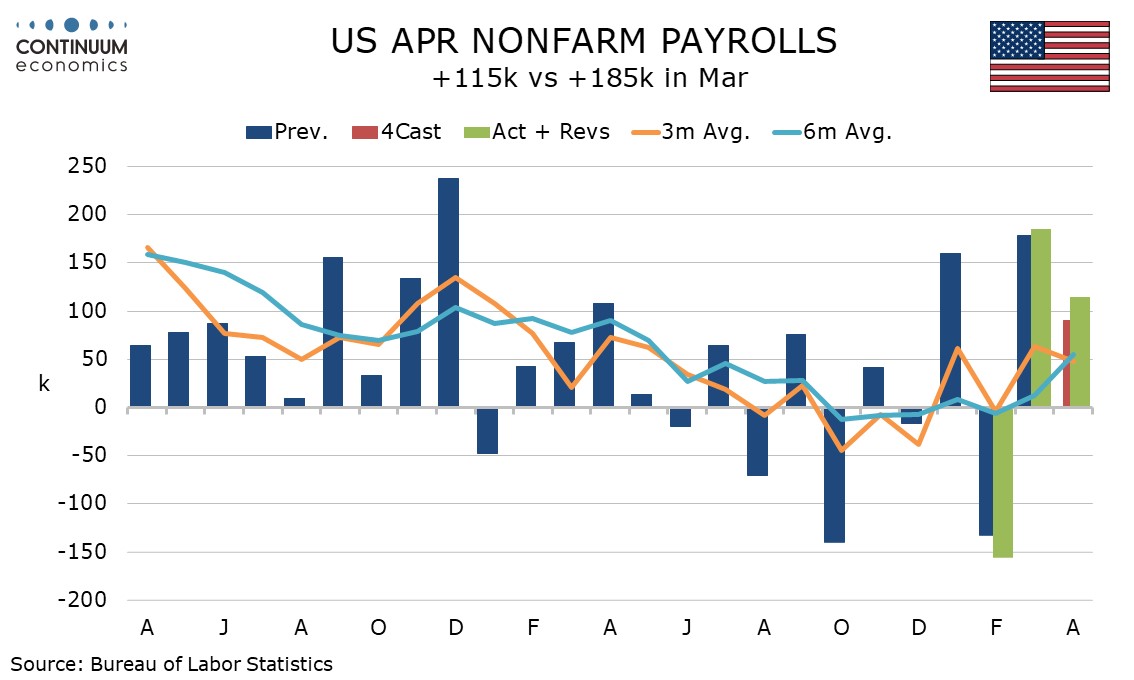

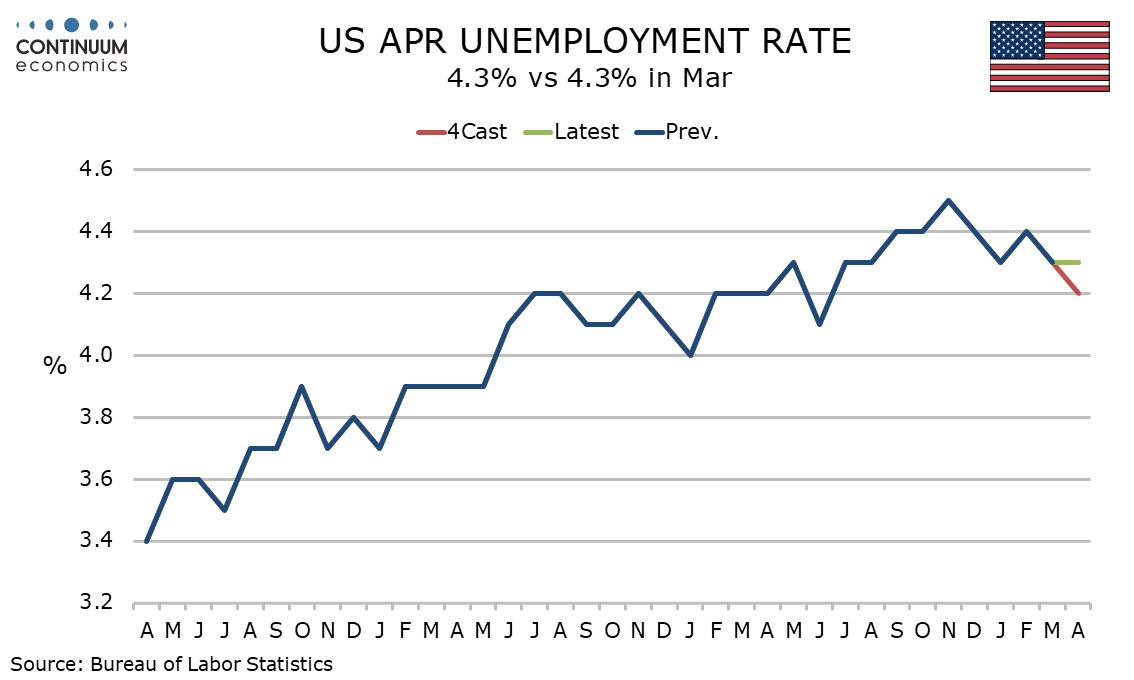

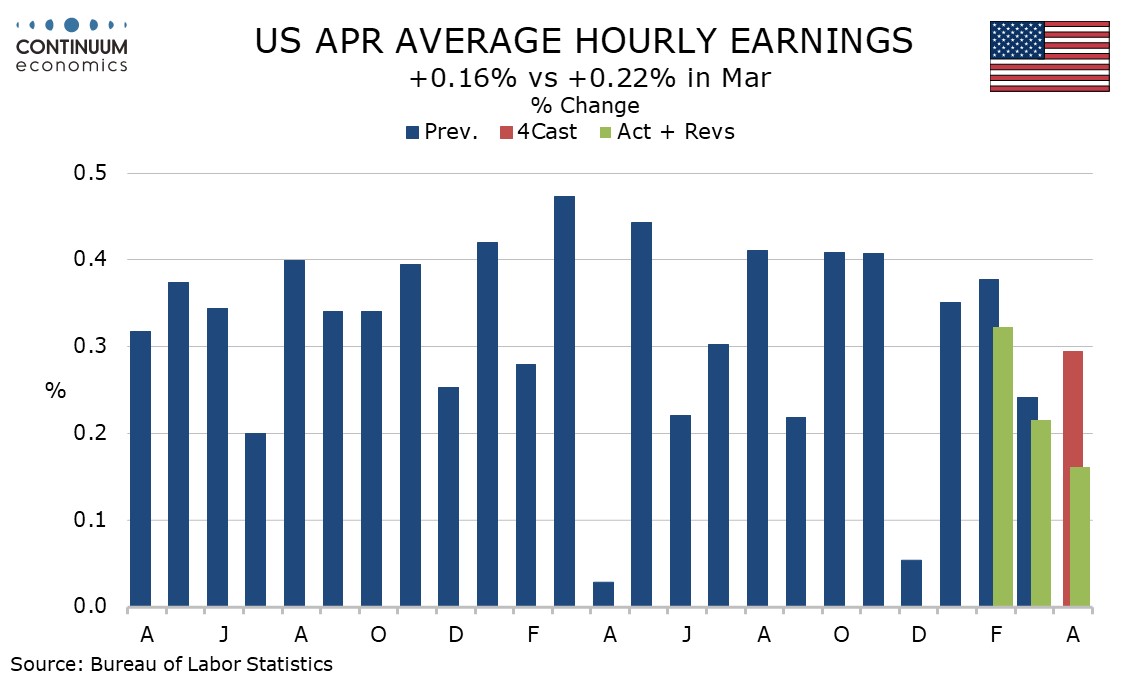

April’s non-farm payroll suggests the US economy continues to grow at a respectable pace in early Q2 with no signs of a hit from the oil shock yet. Payrolls increased by a stronger than expected 115k, with unemployment stable at 4.3% and the workweek stronger at 34.3 hours from 34.2. Average hourly earnings were slower than expected, up by 0.2%, which will be well behind April prices.

Revisions were modestly negative on net, with March revised up to 185k from 178k but February revised down to -156k from -133k. March’s strength was flattered by the rebound from February but trend is improving, with the private sector showing a 3-month average of 55k and a 6-month average of 68k, both over double where they were in December. Two weeks of very low initial claims since the payroll was surveyed suggests momentum is continuing into early May.

Payroll growth continues to be led by health care at 54k but retail at 22k and transport and warehousing at 30k both saw a second month of solid growth. Recent weakness in information at -13k and financial at -11k persists, while manufacturing saw a marginal 2k decline. Construction rose by 9k.

The unemployment details were less positive with employment down by 226k and the labor force down by 92k, lifting the rate to 4.34% from 4.26%, though both rounded to 4.3%. This is the third straight month that employment has fallen in the household survey, clearly underperforming payrolls.

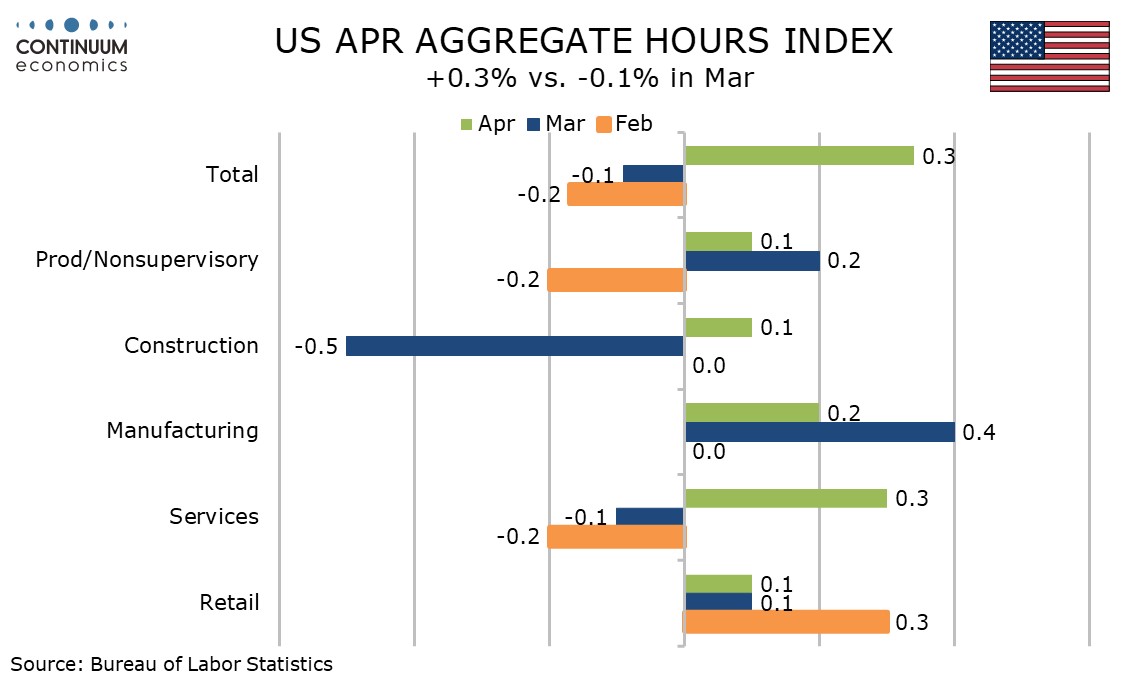

The workweek returned to 34.3 hours after a dip to 34.2 in March, leaving aggregate hours worked up by 0.3% after a 0.1% decline in March. Construction increased by 0.1%, manufacturing by 0.2% and services by 0.3%.

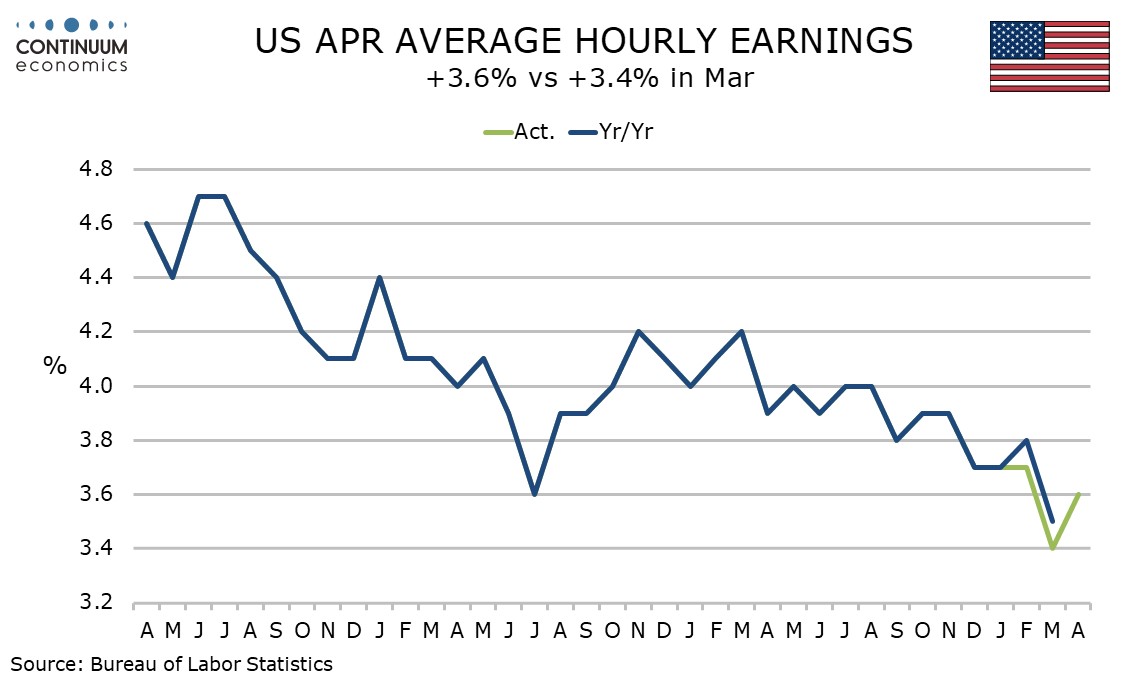

Average hourly earnings rose by 0.16% before rounding after a downwardly revised 0.22% in March suggesting trend is slowing even with yr/yr growth correcting to 3.6% from 3.4%, still below the 3.7% seen in December, January and February. Wage growth is falling behind rising prices but consumers may be getting some offset from lower taxes, helping to explain economic resilience.

Despite the loss of momentum in wages, the Fed’s inflation worries are not wage-generated. The employment data suggests little case for putting easing on the agenda with the labor market picture looking fairly stable.