GBP: Foreign Investor Flows

· Inbound inflows into the UK have been solid in the last few years attracted by yield pick-up and fiscal consolidation for gilts and cheap comparable valuations in UK equities. UK BOP data suggests something would have to go really wrong to stop inbound portfolio flows e.g. UK recession or a Labour government that abandons fiscal consolidation in favor of aggressive U.S. style stimulus. These are low to modest probability scenarios and any change in Labour leadership is likely to produce a temporary but not a deep selloff in GBP on small to modest changes in the fiscal rules.

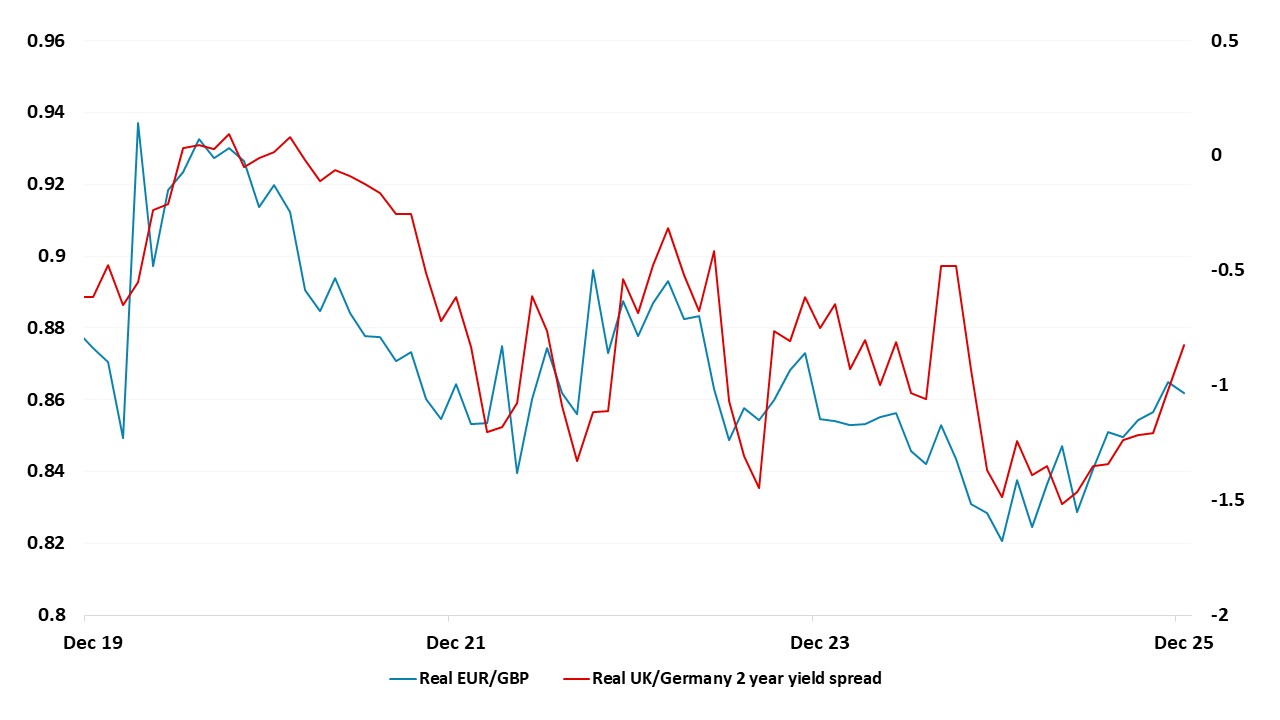

· In terms of 2026 GBP forecasts, we see the BOE cutting by 75bps, while we see the ECB cutting by 50bps. This can hurt GBP against the EUR (Figure 4) and we forecast EURGBP at 0.90 end 2026.

Though the UK has a sluggish economy and the prospect of a change of Prime Minister, what is happening to foreign investor inflows?

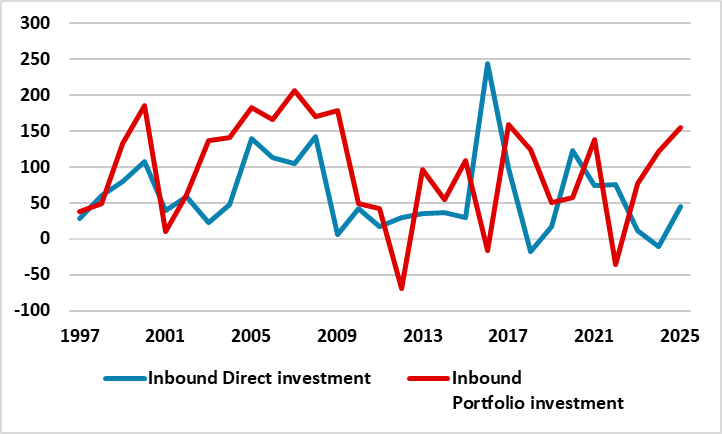

Figure 1: Inbound Direct and Portfolio Investment Transactions (GBP Blns)

Source: ONS BOP Data (2025 figure are Q1-Q3 annualized)

Looking at UK balance of payment data on capital account transactions shows that inflows into the UK for portfolios have rebounded after the sharp dip in 2022 (global risk off on DM rate hikes). For gilts, while some are worried about UK fiscal trends, other global investors draw the sharp contrast between fiscal consolidation in the UK and lax fiscal policy in U.S./France. With the BOE expected to further slow the pace of QT from September 2026, the supply picture is getting less intense and any moderate rise in gilt yields may be used to buy gilts multi-year. The high risk that PM Starmer and Chancellor Reeves could be replaced this year (here) means that inflows could be more volatile, until fiscal policy is clarified. However, we would only see small to modest relaxation of the fiscal rules under a new PM/Chancellor and this would still leave the UK on fiscal consolidation path and a much better trajectory than the U.S. Global investors are also attracted to UK equities for investment and M&A reasons, as comparable UK companies are still at lower valuations than their U.S. peers and on UK equity only metrics – some bad news is still discounted. Provided the UK avoids a recession, this equity inflow should be solid, as growth muddles through and the BOE is likely to cut interest rates to 3% in 2026.

Direct investment inflows however remain on a lower trajectory than before the 2016 Brexit vote, with a 2017-25 average of GBP46bln versus GBP69bln per annum average 1997-2016. Whether a new Labour PM/Chancellor would consider a formal entry into the EU customs union is uncertain. While the economic arguments are strong, UK politics is leaning against too much legal immigration.

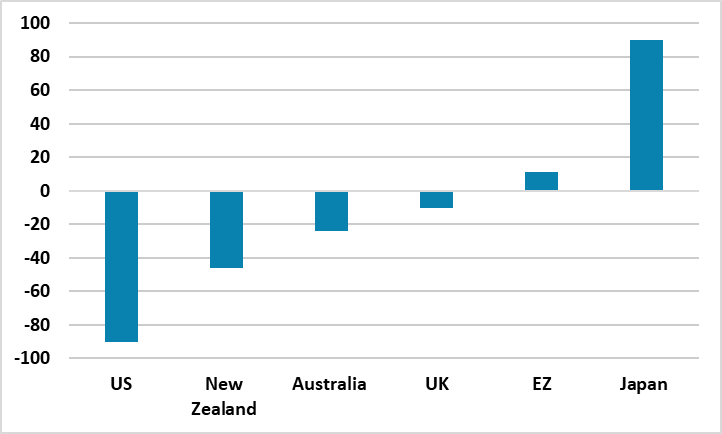

Figure 2: Net International Investment Position to GDP (%)

Source: IMF External Sector Report 2025

From a wider perspective, the UK net international investment position remains well under control, in contrast to the U.S. (Figure 2). Though the UK has had persistent C/A deficits, UK investors have been able to achieve high returns overseas than the UK pays foreign investors and this has kept the NIIP under control.

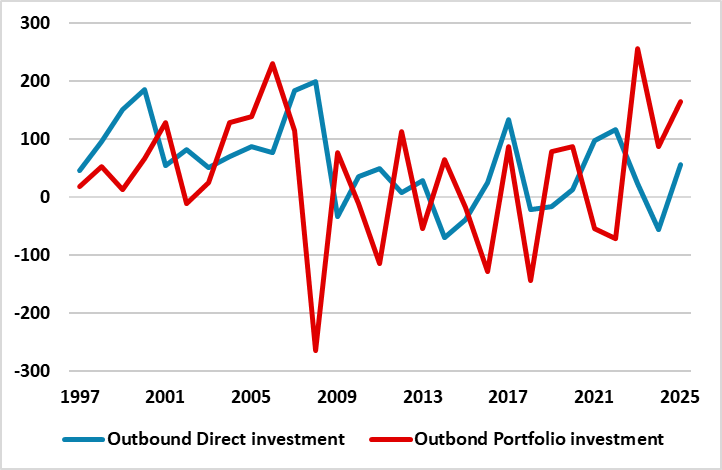

Meanwhile, outbound portfolio flows tend to be a function of whether global markets are risk on or off. 2008, 2011 and 2022 saw net repatriation transactions for global portfolio holdings by UK investors (Figure 3). However, it is worth noting that the 2017-25 average at GBP55bln is higher than the pre-Brexit vote average of GBP28.5bln 1997-2016. Direct investment outflows from the UK are more modest after the 2016 Brexit vote and from a BOP viewpoint offsets the lower inbound direct investment inflows.

Figure 3: Outbound Direct and Portfolio Investment Transactions (GBP Blns)

Source: ONS BOP Data (2025 figure are Q1-Q3 annualized)

Overall, the UK BOP data suggests something would have to go really wrong to stop inbound portfolio flows e.g. UK recession or a Labour government that abandons fiscal consolidation in favor of aggressive U.S. style stimulus. These are low to modest probability scenarios and any change in Labour leadership is likely to produce a temporary but not a deep selloff in GBP.

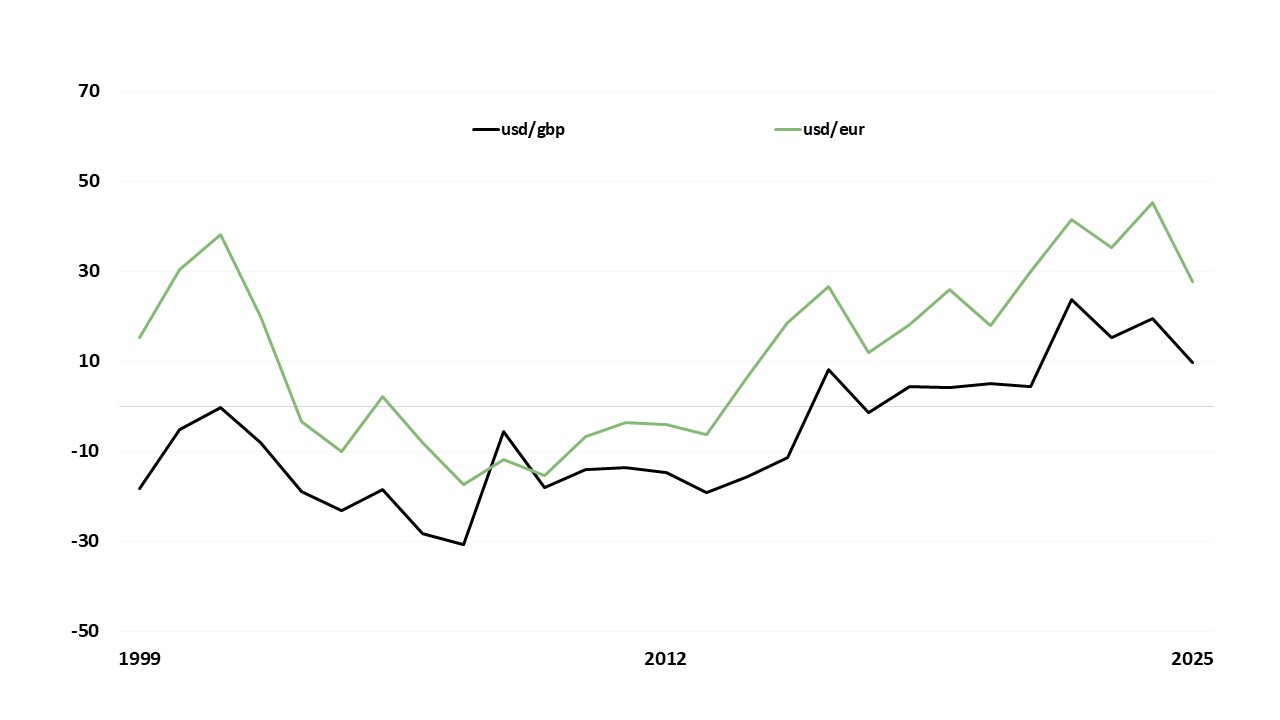

In terms of 2026 GBP forecasts, we see the BOE cutting by 75bps, while we see the ECB cutting by 50bps. This can hurt GBP against the EUR (Figure 4) and we forecast EURGBP at 0.90 end 2026. One of the other drivers in the USD general trend, which we feel is down multi-year. The EUR is more undervalued versus the USD (Figure 5) than GBP and further EUR gains against the USD will likely see the GBP losing ground versus the EUR.

Figure 4: Real EUR/GBP and real 2 year yield spread

Source: Datastream, CE

Figure 5: % difference from USD PPP

Source: OECD, CE