U.S. March CPI - Subdued core rate provides relief

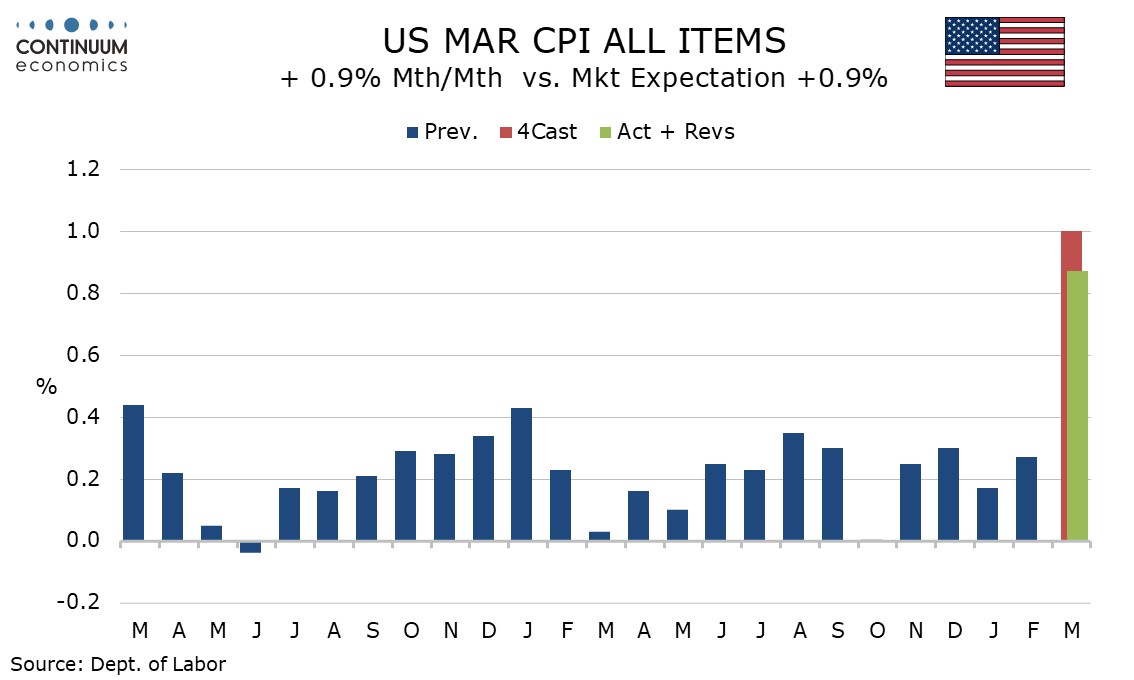

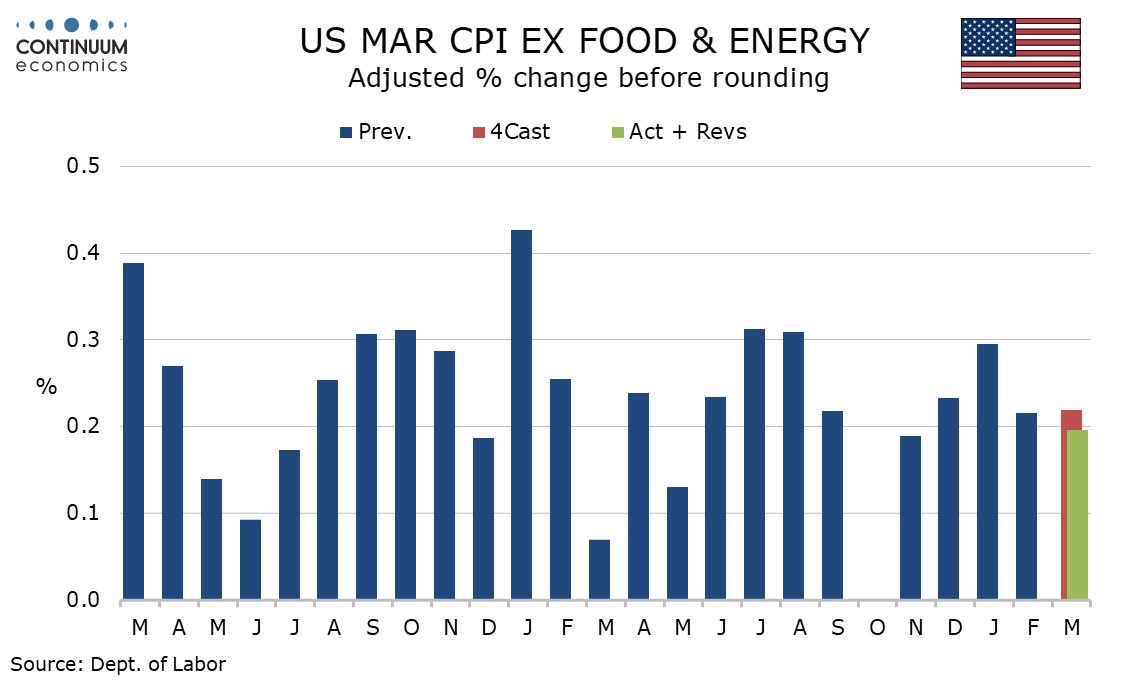

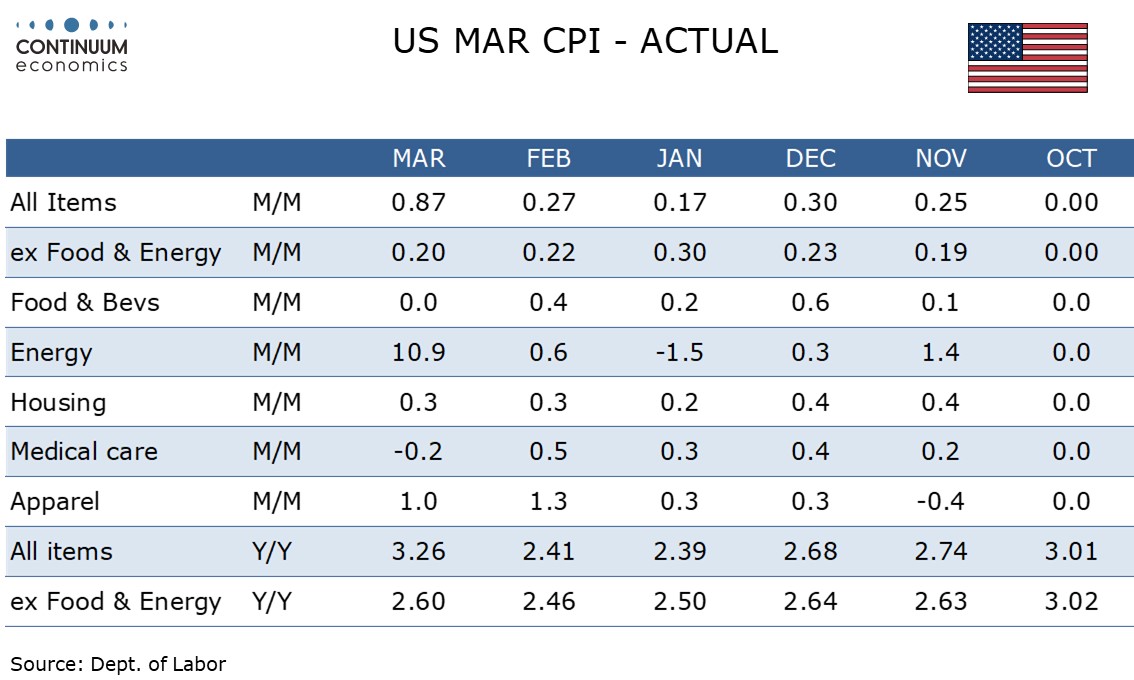

March CPI is as the market expected with a 0.9% increase (0.865% before rounding) led by a surge in energy, but the core rate ex food and energy shows little sign of feed through, rising by a lower than expected 0.2%, with the gain before rounding at 0.196%, the slowest since November’s subdued two-month outcome. Medical care was a significant source of restraint.

Energy prices rose by 10.9%, led by a 21.2% surge in gasoline. Energy services increased by 0.4%, stronger than two preceding gains of 0.2% but not alarming. Food was unchanged, a slowing from a 0.4% increase in February, but there are upside risks going forward with fertilizer supplies disrupted by the closing of the Strait of Hormuz.

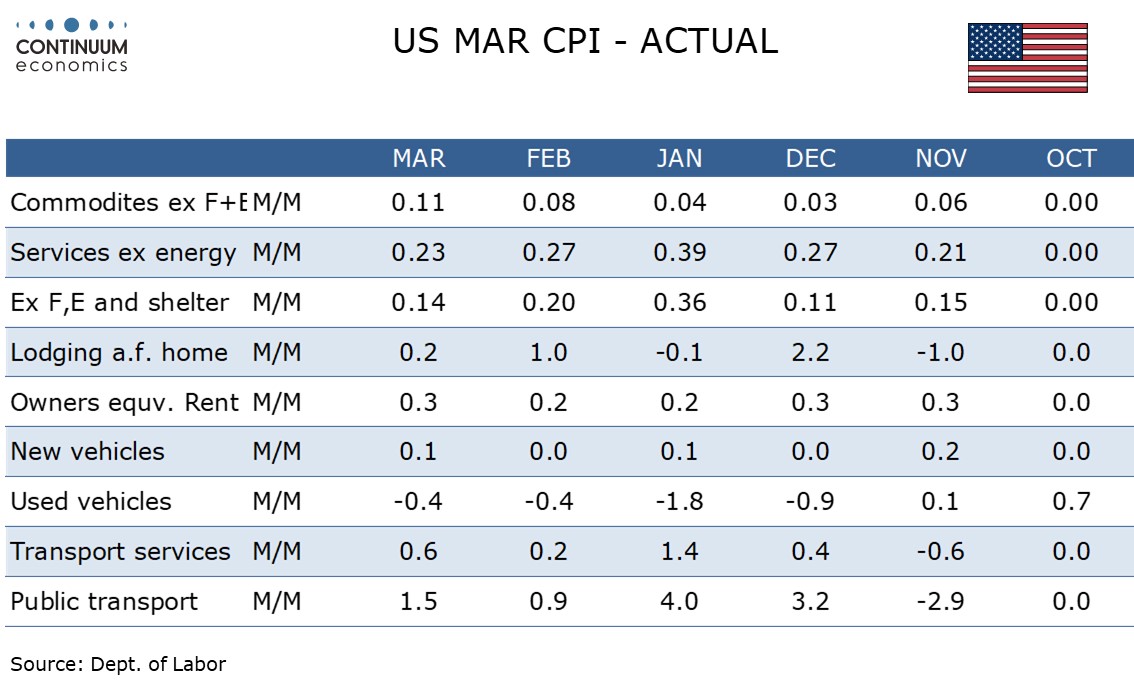

Commodities less food and energy rose by 0.1% for a second straight month. The breakdown is similar to February’s. with apparel showing a second straight strong month, rising by 1.0%, but used autos declining for a fourth straight month, by 0.4%. New autos rose by a marginal 0.1%. Medical care commodities at -1.0% are a downside surprise.

Services less energy rose by 0.2%, slower than the three preceding months. Medical care services were unchanged, also surprising on the downside. Shelter at 0.3% was slightly stronger than two preceding gains of 0.2% while air fares with a 2.7% increase are hinting at some feed through from energy. CPI ex food, shelter and energy rose by only 0.1%, 0.14% before rounding.

Yr/yr CPI at 3.4% from 2.4% is the highest since April 2024. The yr/yr pace ex food and energy edged up to 2.6% from tow straight months at 2.5% to return to its pace of November and December. The core rate will come as a relief to the Fed and keep talk of tightening on hold, though the Fed will remain cautious about easing in this highly uncertain environment.