Argentina: Reserves Depleting, New Devaluation?

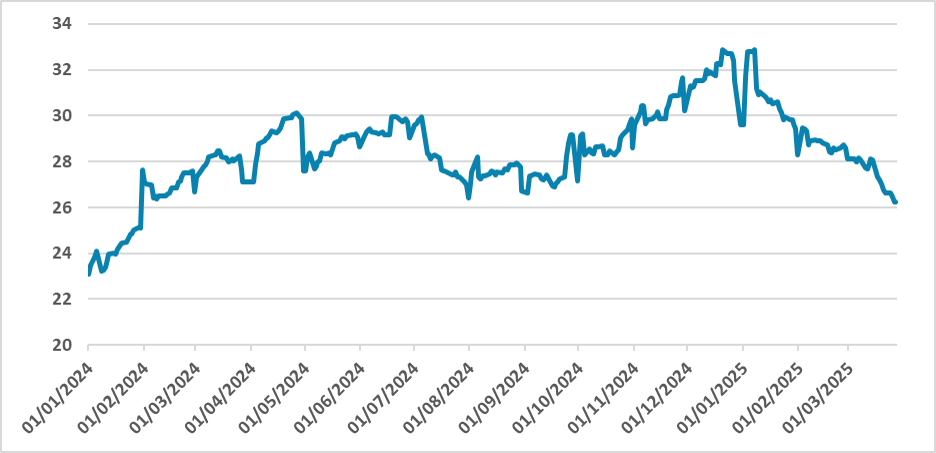

Argentina's foreign reserves have recently fallen to USD 26 billion, the lowest since February 2024, largely due to Central Bank bond payments and difficulties acquiring USD. While internal demand recovers, imports are outpacing exports, complicating reserve accumulation. Additionally, maturing Central Bank bonds will require significant disbursements. The government is negotiating a USD 20 billion IMF deal to address these issues, but the solution is temporary. Argentina needs sustainable export growth to increase reserves and avoid further devaluation and inflation.

Figure 1: Argentina Foreign Reserve (USD Bln)

Source: BCAR

Argentina's reserves have depleted recently, touching USD 26 billion, the lowest level since February 2024. Most of this depletion is related to the payment of Central Bank bonds in USD and the country's difficulty in acquiring USD, as the current account has started to register a deficit. In the first months of Milei’s administration, the devaluation shock, coupled with a strong fiscal adjustment, put Argentina into a recession, meaning lower internal demand and a more favorable external sector, which maintained current account surpluses.

However, with the recovery of internal demand and an appreciating exchange rate, imports are surpassing exports again, complicating the BCAR's strategy of accumulating reserves, which is essential to address Argentina's macroeconomic imbalances. Another complicating factor is the maturing Central Bank bonds this year. Estimates suggest that the Central Bank will need to disburse around USD 9 billion to fulfill this obligation, which will place a significant toll on the already depleted foreign reserves of the Central Bank.

An immediate solution for the government is to seek a new deal with the IMF, which has already indicated that it is nearly finalized, as the government has launched a decree authorizing the signing of the deal (here). Rumors suggest that the total package will provide fresh funds for Argentina, totaling a USD 20 billion deal. However, rumors also indicate that around USD 8 billion will be made available immediately so the Central Bank can make payments without taking a toll on its reserves.

Nevertheless, this solution seems to be only palliative. Argentina needs to increase its foreign reserves in a sustainable manner by boosting exports of goods and services. One dilemma is related to the exchange rate. The government seeks to anchor general prices by initially applying a 2% crawling peg and has recently reduced the pace to 1% monthly devaluation. This means the real exchange rate is appreciating in real terms, as it is growing below the internal rate of inflation. This means that foreign goods are becoming less expensive, and now, with the economic recovery, imports will increase faster than exports. However, applying a strong devaluation risks another inflationary spiral, which the government seems to want to avoid at all costs. If exports of gas and soybeans cannot increase reserves accumulation, the clock will be ticking for another devaluation.