China: Mixed Early 2025 Data and Policy Stimulus

Headline industrial production and retail sales were better than expected, but the breakdown of the data shows a mixed picture for consumption and residential investment remains a negative drag on GDP before the 20% U.S. tariffs hits. Meanwhile, though the weekend policy announcement on boosting domestic demand and consumption is welcome, further details will likely be incremental rather than aggressive. We stick with a 4.5% GDP forecast for 2025.

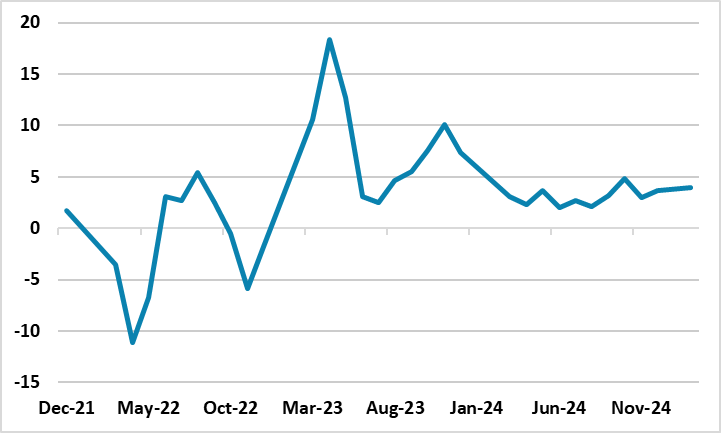

Figure 1: Retail Sales Yr/Yr (%)

Source: Datastream

The January-February economic releases provide a mixed impression of the underlying momentum of the economy. Though the 5.9% Yr/Yr gain in industrial production and 4.0% in retail sales were better than expected, the breakdown shows the economic imbalance in the economy. Industrial production was led by high tech production at 9.1% Yr/Yr, but the fixed investment breakdown shows private investment close to zero and dominated by SOE investment. Meanwhile, car sales in the retail sales data fell to -4.4% Yr/Yr versus +0.5% in December and residential construction was -9.8% Yr/Yr. This underlines the unbalanced nature of the economy going into early 2025 before the adverse effects of the extra 20% tariffs by the U.S. hit exports and production from the March figures onwards.

Meanwhile, China authorities announced a focus on boosting consumption and domestic demand with two main parts. Firstly, boosting household incomes, though no specific policy details were forthcoming. Secondly, to provide more support for safety net e.g. education/pensions, which is the correct approach as this could reduce precautionary savings and then boost consumption on a structural basis. However, no specific policy details have yet been provided and we continue to feel that the specific will be incremental rather than aggressive. The March NPC did see some extra money allocated to safety nets, but this totaled around Yuan120bln and we would see this as being insufficient for an economy of China’s size. Additionally, the total fiscal stimulus so far at Yuan2.5trn is at the low end of expectations. Though the NPC press conference promised more fiscal stimulus, the authorities appear to not be in a hurry. Meanwhile, China press are full of articles today noting that the PBOC is not in any hurry to ease monetary policy. We now look for 10bps off the 7 day reverse repo rate in June and 25bps off the RRR rate in May, which is slow easing to avoid Yuan depreciation and upsetting the U.S. still further.