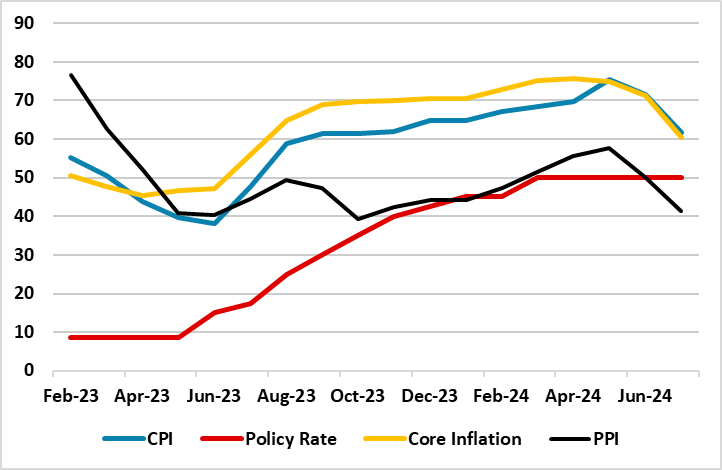

Turkiye Inflation Review: CPI Cooled Off to 61.8% in July

Bottom line: After easing to 71.6% annually and 1.6% monthly in June, down from 75.5% in May, consumer price index (CPI) cooled further down to 61.8% y/y in July. As we expected, favourable base effects, tightened monetary and fiscal policies, additional macro prudential measures, and relative Turkish lira (TRY) stability helped relieving the pressure on the inflation. We expect the falling trend will continue in August on base effects again, and CPI will likely hit 50%’s.

Figure 1: CPI, PPI, Core Inflation (YoY, % Change) and Policy Rate (%), February 2023 – July 2024

Source: Continuum Economics

Turkish Statistical Institute (TUIK) announced July inflation figures on August 5. Accordingly, CPI cooled down to 61.8% y/y in July, reaching its lowest level in the last nine months, after hitting 71.6% annually in June.

When annual rate of changes (%) in the CPI’s main groups are examined in July, clothing and footwear with 39.6% was the main group with the lowest annual increase while education recorded the highest annual increase with 104.5%. It is worth mentioning that housing (98.5%), hotels, cafes and restaurants (76%) also recorded remarkable YoY increases. While the annual inflation rate eased in July, it rose by 3.23% MoM compared to June. Core inflation (CPI-C) recorded a 2.5% MoM increase, scaling up to 60.2% on an annual basis. The domestic PPI was up 1.9% MoM in June for an annual rise of 41.4%, the data showed.

Treasury and Finance Minister Mehmet Simsek stated after the inflation release that monthly inflation increased in July due to temporary effects while annual inflation has decreased by 9.8 points since June, and added that "Our program, primarily aimed at disinflation, continues to yield positive results and the decrease in inflation will be felt more significantly in the upcoming period."

We envisage CPI to cool off to 50%’s in August on base effects again coupled with tightened monetary and fiscal policies, additional macro prudential measures, and relative TRY stability. Despite inflation is expected to ease in Q3, there remains upside risks such as recent hikes in taxes along with 38% surge in electricity and natural gas prices, and 25% hike in minimum monthly pension in July.

As CPI softened in July triggered by favourable base effects and relative TRY stability underpinning the inflation relief, we foresee that favourable base effects will continue to dominate the inflation outlook in Q3, but the extent of the decline will be determined by administrative price adjustments.

In spite of aggressive monetary tightening, we think buoyant domestic demand, stickiness in services inflation, deterioration in pricing behaviour, and inflation expectations will continue to cause pressure on the general level of prices in Q3/Q4. It is worth noting that CPI traditionally eases in Turkiye during summers, as energy consumption falls and tourism brings in foreign currencies.