BCB Minutes: Caution Rather than Optimism

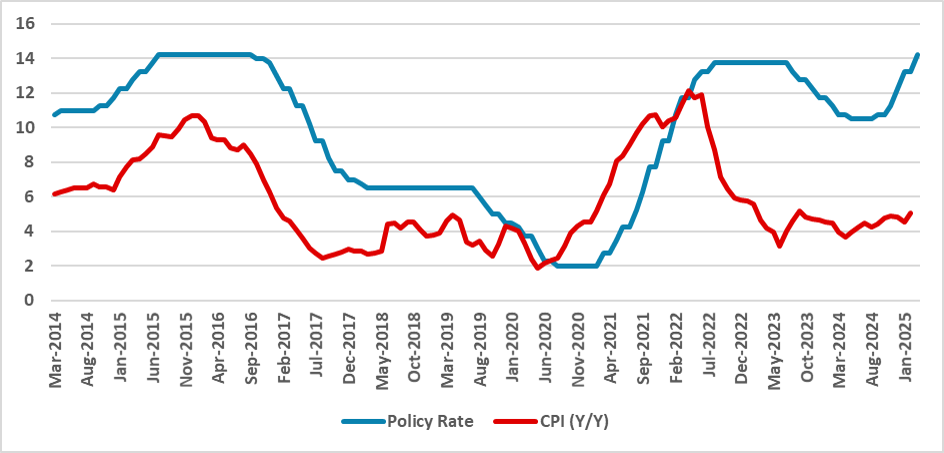

The Brazilian Central Bank (BCB) raised the policy rate by 100bps to 14.25% amid signs of economic deceleration, including slower growth, job creation, and consumption. The BCB highlighted external uncertainties, such as U.S. trade policy, and domestic challenges with rising inflation. It emphasized maintaining an unobstructed monetary policy, particularly through the credit and expectations channels. The BCB plans a smaller rate hike in the next meeting, we expect it to be the last hike with cuts occurring only in 2026.

Figure 1: Brazil Policy Rate and Inflation (%)

Souce: IBGE and BCB

The Brazilian Central Bank (BCB) has released the minutes of their last meeting (here), in which they opted to hike the policy rate by 100bps to 14.25%. In general, the minutes expanded on the BCB's thinking, detailing most of the risks the BCB faces. Although the minutes maintained the hawkish tone of the communiqué, the BCB also expanded on the economic activity, which has shown incipient signs of deceleration.

Regarding the external environment, the Committee highlighted the uncertainty about U.S. trade policy and its impact on the pace of deceleration, disinflation, and the Fed’s monetary policy, affecting growth in other countries.

On the domestic front, the situation is challenging, according to the BCB. A large paragraph was dedicated to growth. According to the BCB, the economy showed incipient signs of deceleration, with growth slowing, job creation slowing down, and consumption declining after thirteen months. Soft data regarding consumers and enterprises also indicated signs of deceleration. Although the BCB stated that significant uncertainty surrounds this deceleration, they also noted that it is a necessary condition for the convergence of inflation. On the other hand, current inflation and inflation expectations increased, indicating a deterioration of the scenario. Services inflation has increased recently in a scenario of a positive output gap.

Interestingly, the board emphasized the need to maintain the monetary policy channel unobstructed, especially regarding the credit channel, which the government could use through public banks to increase credit supply and influence the expectations channel. Although it is unclear how the government could obstruct the expectations channel, we believe a credible fiscal policy, in which agents clearly believe in the stabilization of the debt-to-GDP ratio, would be helpful in fulfilling this condition. The Committee also believes that inflation in food and beverages is likely spreading to other inflation groups, with which we disagree. In a scenario of slowing demand and an appreciating exchange rate, food price growth, which was impacted by exchange rate depreciation and international food prices, tends to be restricted.

The BCB opted to communicate an additional hike for their next meeting, with a smaller magnitude. Given the BCB's scenario, we believe there is a 60% chance of a 75bps hike and a 40% chance of a 50bps hike. In any case, we believe it will be the last hike. As Q1 data comes out and it becomes clear the economy is decelerating, we believe inflation will start to fade, and inflation expectations will be revised. We expect cuts to occur only in 2026.