Eurozone Outlook: Conflicts of Interest

· Under our more likely view of limited further fighting in the Middle East, we see oil and gas prices largely falling back to the pre-war levels within a year, with the current situation very different from that of 2022 and the Ukraine War in which the EZ lost access to Russian gas as that ‘shock’ was super-imposed on an EZ economy where demand was recovering from the pandemic amid clear shortages.

· Even so, we now see 2026 HICP inflation some 0.5 ppt higher than envisaged three months ago, averaging 2.2% but with a dip back below 2% on the cards by mid-2027 and with the HICP outlook on average for 2027 little changed at 1.9%. But there is also a weaker real economy, hit not just by the impact of the Middle East conflict but also from financial conditions remaining tighter than the ECB policy rate levels.

· While the ECB has now underscored that rate hikes are certainly possible, we still regard the next move in rates to be a further cut, though probably only one more 25 bp move later this year, something that the real and monetary economy may very well be demanding.

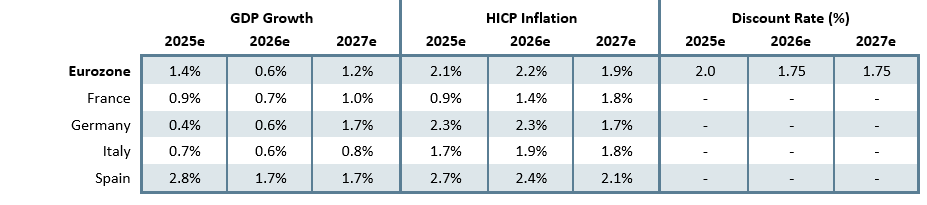

Forecast changes: Compared to the last outlook, we have made a clear downgrade to the overall EZ growth outlook, more so for this year but pencilled in a less marked but fiscally driven pick-up for 2027. As notable then is the upwardly-revised HICP outlook, but a still-soft and below-target on average for 2027. But inflation risks mean we now only expect one further ECB rate cut.

Our Forecasts

Source: Continuum Economics, Eurostat

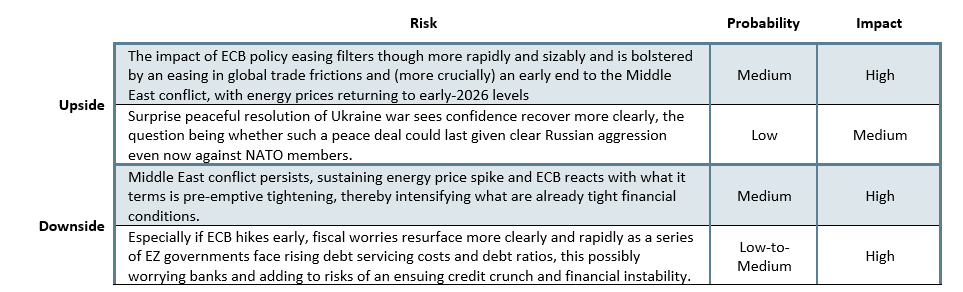

Risks to Our Views

Source: Continuum Economics

Eurozone: Inflation Rise Limited?

Like the ECB and others have done, we have identified alternative likely scenarios regarding the length and breadth of the Middle East conflict. But under our very much more likely view of limited further fighting we see oil and gas prices largely falling back to the pre-war levels within a year. This view is also a result of the fact that the EZ economy is better positioned to absorb shocks, with the current situation very different from that of 2022 and the Ukraine War in which it lost access to Russian gas as that ‘shock’ was super-imposed on an EZ economy where demand was recovering from the pandemic amid clear shortages. Admittedly, a clear and fresh rise in inflation is already emerging given what is happening to early-March retail fuel prices and with some second round effects that will affect rates into 2027 (though where actual inflation at the end of next year may be lower than previously thought). Indeed, we now see 2026 HICP inflation some 0.5 ppt higher than envisaged three months ago, averaging 2.2% but with a dip back below 2% on the cards by mid-2027 and with the HICP outlook on average for next year little changed at 1.9%.

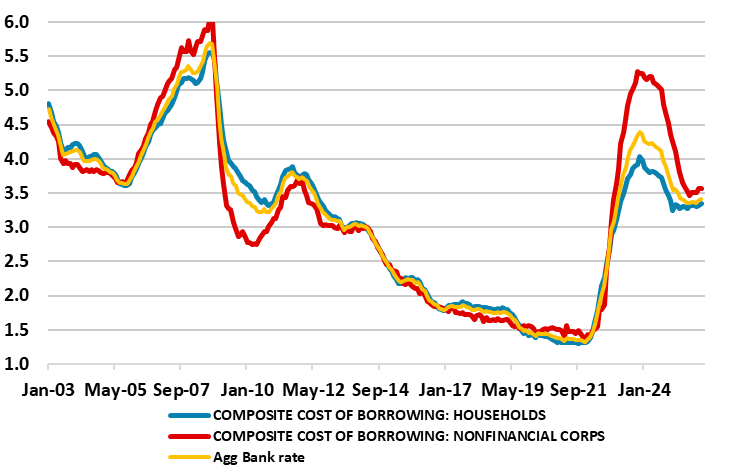

This will be partly on account of the likely real economy damage from the conflict but also reflects our long-standing view that the ECB has been complacent, downplaying what we regard are downside real economy and monetary risks which may now be materialising. These range from ignoring the fact that a third of what looks to be above trend growth last year was abnormal (due to an aberrant surge in Ireland), the lagged U.S. tariff impact and what we think are financial conditions that have actually been tightening even before the impact of the conflict on markets. In fact, banks have not only been tightening credit standards for some months now but are actually refusing to lend to an increasing amount of companies and are now raising effective rates to customers (Figure 1), this making the next ECB bank lending survey (due Apr 28) all the more important. There is also the Chinese export dumping factor, this likely to depress consumer goods prices and hit GDP via increased EZ imports! Indeed, not only have imports of Chinese goods increased substantially in value terms, as import prices have declined, the increase in volume terms has been even larger, also bringing clear evidence of a pass through into lower EZ goods inflation. The latter may also reflect the appreciation of the euro while further declining prices for imported goods should eventually work their way via second-round effects and weigh on services inflation as well.

In fact, and explaining out below-consensus outlook, downside risks for the real economy already seem to materialising in survey and monetary data, the former evident in the likes of PMI numbers that when include the recession bound construction sector tell a sorry tale. Moreover, it is still uncertain how businesses will react to the unclear trade situation with the U.S. and/or how the already wary banking sector will reassess risks, especially if the U.S. shifts its trade focus to services trade rather just goods. Notably even given the recent U.S. Supreme Court ruling suggesting otherwise, the EZ seems locked into 15% tariffs given its trade deal. But given the flow of data, and the risks ahead, we see near-flat GDP growth for this and the next two quarters, with a 0.2 ppt downgraded 0.6% 2026 average growth but somewhat better in 2027 at 1.2%, the latter also pared back 0.2 ppt!

But the 2027 outlook is more encouraging as both the German fiscal stimulus and EU-wide defense build-ups take effect, this actually pointing to a gradual q/q pick-up in GDP from late 2026. This outlook reflects a host of uncertainties, some to do with the timing of likely fiscal and defense initiatives and some to do with to what degree they may boost EZ growth only modestly due to the likely large import content to begin with. As for impact on the current account balance, the anticipated cyclical, and possibly structural, recovery in imports seen ahead, as well as what may be a weak global economy weighing on exports, will also mean that the improvement in the current account surplus last year (at around 2.6% of GDP) may reverse into 2026 and possibly even more so in 2027. This is also a headwind to GDP growth.

Figure 1: Tight(er) Financial Conditions Already Feeding Through

Source; ECB, CE (%)

Fiscally, to suggest the backdrop and outlook is mixed would be an understatement, now clouded further by higher borrowing costs and possible government intervention ahead to reduce the spike in oil and gas prices for consumers and maybe firms. The overall EZ budget situation is likely to see small increases to above 3% of GDP into 2027, with the primary deficit largely stable at -1.2% and the structural gap similar to the headline numbers. But this masks marked differences among EZ members not least the Big 4 we assess in the Outlook. Regardless, the fall in the EZ government debt ratio to 88.5% of GDP last year will likely soon be followed by a rise toward 91% in 2027. These fiscal divergences raise policy question and make the job of the ECB harder; it is thought the central bank may wish to be more vocal in its fiscal criticism through 2026. But this may make it harder to use its TPI tool on any credible basis if what are current fiscal problems turn into genuine crisis (eg France).

ECB: In Not Such a Good Place

With no change in policy expected and this being delivered unanimously this month, the ECB underlined its determination to ensure that inflation stabilises at the 2% target in the medium term. Unsurprisingly, it stressed how the Middle East conflict has made the outlook significantly more uncertain, creating upside risks for inflation and downside risks for economic growth. But is seemed to put more stress on there being a material impact on inflation through higher energy prices in the near-term but the medium-term implications depend both on the intensity and duration of the conflict. It did provide updated forecasts based on market thinking up to Mar 11 which we think are too pessimistic about inflation and too optimistic about growth. But given an updated profile in which its underlying focus on core inflation gradually eases back to target we think market rate hike thinking is very overblown. After all, it has eased policy for some time with the core rate much higher.

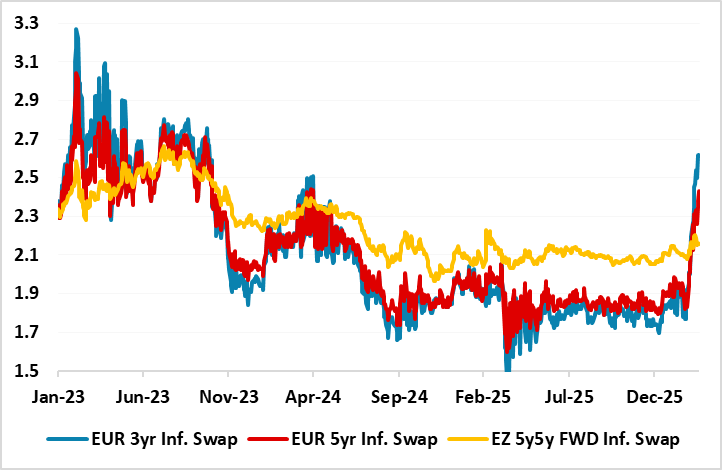

Figure 2: Inflation Expectations Higher But Limited to Shorter-Term

Source: Bloomberg

While somewhat deferred, we still regard the next move in rates to be a further cut, especially as real rates are very much higher that the energy shock of four years ago. Even if not, we think markets pricing in rate hikes is premature. However, the ECB has a history of policy mistakes with premature but short-lived hiking (ie 2008 and 2011). Such a risk cannot be ruled out again especially give the Council’s view of the ‘good place’ the EZ economy was in prior to the conflict even if the result of such action may be to intensify fiscal strains.

Germany: Double Negative Whammy?

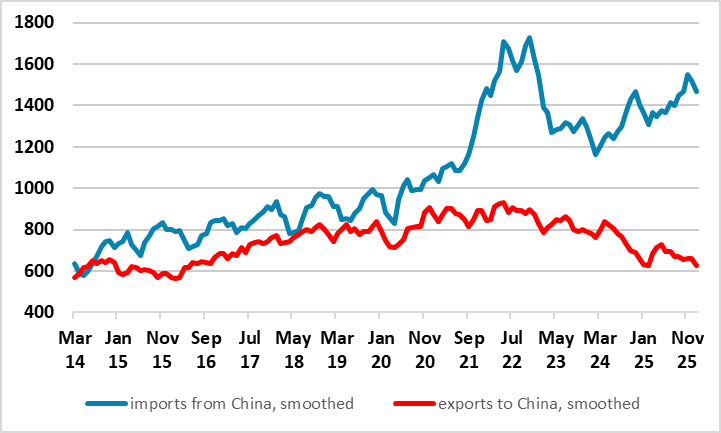

In contrast to the better than expected end to 2025, economic news so far this year has been very discouraging – and that was before the likely hit from the Middle East conflict emerged. Industrial output, orders and export all fell markedly in January. It does therefore seem as if tariffs, the stronger exchange rate, political tensions and uncertainty are very much still hurting Germany’s aging and out-dated economy. Reacting to trade weakness, Chancellor Merz last month called on China to appreciate its currency, remove subsidies for domestic manufacturers and reduce industrial overcapacity blamed for flooding German markets with cheap products (Figure 3) – this suggesting that the German government would not treat the surprise drop in January imports as indicative of a fresh trend. As for trends, even given the solid Q4 2025 performance, the German economy has on average, shrunk by an average 0.1% q/q since end-2022. And the question is now just whether Middle East fall-out will offset the planned landmark fiscal expansion, the first signs of which appeared at end-2025.

Figure 3: Germany’s Increasing Trade Divide with China

Source: German Fed Stats Office, EUR billion

But in reaction to Q1 weakness and the conflict’s’ likely impact we have made a 0.4 ppt downgrade to 0.6% for the growth picture this year, which implies a large output gap of up to 2% of GDP that makes us still confident of continued underlying disinflation. Admittedly, there will be a clear impact on CPI inflation from the conflict and we have raised the 2026 forecast by 0.6 ppt to 2.3% but this is seen being short-lived to a degree that we have pared back the 2027 outlook a notch to 1.7%, the latter helping shore up next year’s GDP outlook to 1.7%, alongside fiscal stimulus feeding through. Even so, it would be wrong to overstate the impact of the planned German debt surge. Multiple challenges will impede the government’s spending plans. First, there is the (in)famously slow procurement process for military equipment widely regarded as overly bureaucratic. Secondly, there are the existing capacity constraints in the German and European defence sector. Similar constraints may also hamper infrastructure investment so we suggest the fiscal reforms need to be accompanied by administrative reforms which may be drawn out by coalition differences. Moreover, Germany’s leaders have an array of factors to consider not least on the downside by subdued productivity growth and adverse demographics – NB: IFO recently revised its forecast for a 1% population decline by 2050 to nearly 5%! Thus the key is how the intended fiscal space can be utilised to boost the economy’s longer-term productive capacity which even with some inclusion of fiscal developments the European Commission still see at nothing more than around 0.6% even into 2027.

The bottom line is that a German budget could turn into one of well over 4% (both headline and structural) probably not this year but into 2027. As a result, the government debt ratio would rise from its current 63% of GDP toward 80% over the next decade possibly without negative repercussions – not least as Germany has already suggested EU-wide fiscal rules (which this initiative compromises) need to be relaxed. But added government spending will boost imports. As a result, it looks very likely that the circa-6% of GDP current account surplus seen in 2025 will be reduced down towards 4% in 2026 – both helping growth elsewhere and politically speaking addressing the source of what may be persistent trade tensions.

France: Polarized Politics Persist?

It may be that the Middle East conflict is accentuating divides as the electorate is reacting diversely to parties either pro or against President Trump, this seemingly the case with what seemed to be continued polarization in this month’s important local elections. Indeed, both the far left and the far right polled well, but where the National Rally may have undershot at least its expectations. This therefore offers little new in terms of assessing how next year’s presidential election may fare, where the risks remain very much that what are currently merely fiscal and political tensions could turn into a genuine crisis. The French political system is partly to blame; the two stage process of French elections means that parties of the left and of the centre will likely combine to stop any National Rally candidate (currently ahead in the polls) winning. This implies more parliamentary deadlock, which in turn points to a continued fiscal stalemate, the latter suggesting further credit agency criticism and even downgrades. This will only add to existing economic weakness that may be exacerbated by market-induced fiscal policy consolidation and greater budget problems. In this regard, the clock may already be ticking as the current minority administration was forced to use constitutional powers to push through a 2026 Budget bill, without parliamentary support, but needed to survive a no-confidence vote. It did so, but it is still likely that the budget gap this year will be no lower than the 5.4% of last seen last year, with the likelihood being that a new but politically weak president next year will not call fresh legislative elections meaning a fractured parliament will persist through to the next scheduled vote in 2029. As a result, the gross government debt ratio will rise even further toward 120% of GDP maybe as soon as next year.

Admittedly, it is the case that France’s fiscal woes are not a question of economic imbalances as France is running a (modest) current account surplus which we see persisting out into 2027. But it is still the case that France is penned in by the fact that overseas investors are significant holders of French sovereign debt, with non-residents holding over half of France's sovereign debt. It is also notable that French public spending is the (second) highest in the EU and seems set to rise (Figure 4).

Admittedly, French sovereign spreads remain well below that of the UK despite a higher debt and deficit in France. We suggest this is largely a result of France being part of the EZ and where the ECB offers some protection – albeit where France’s current politics-driven fiscal woes suggests the much vaunted TPI tool is highly unlikely to be used. Instead, it is the current low level of ECB policy rates that is cushioning the French market on a relative basis. Thus, given our view that policy rates will still likely fall further, the latest French government can afford to kick the fiscal can further down the road. However, this may be only for the time being as when the ECB starts to tighten afresh (or even visibly contemplate this), market scrutiny of France will intensify. The question is whether French fiscal fragility may act to dissuade the ECB from early tightening, this also being a key question and issue for 2027!

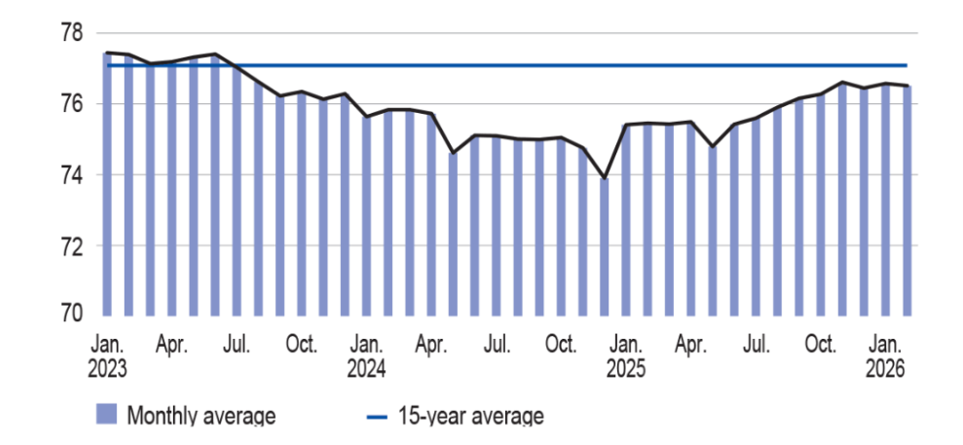

Despite the emerging energy price shock, we have made little change to the already soft and fragile French economic outlook for this year or next, though seeing GDP growth a notch lower this and next year to 0.7% and 1.0% respectively. The downgrade for this year would have been more marked but for the better-than-expected late 2025 outcome, this masking an end-2026 projection of around 0.5% and an economy with plenty of spare capacity (Figure 4). The real economy picture is helped by what will still be low inflation rates which we see at 1.4% and 1.8%, the latter unchanged from that envisaged three months ago.

Notably the pick-up in 2027 is on the back of fiscal expansion in Germany and better net exports partly related to increased EU defence sending (France’s large defense industry provides almost 10% of global arms exports). But the risks are clear from the above analysis. Notably, we do not see France being a major part of any clear defense-based fiscal expansion given its adverse budgetary backdrop and outlook.

Figure 4: France Has Plenty of Spare Capacity – Capacity Utilisation (%)

Source: Bank of France

Italy: Politics Vs Economics

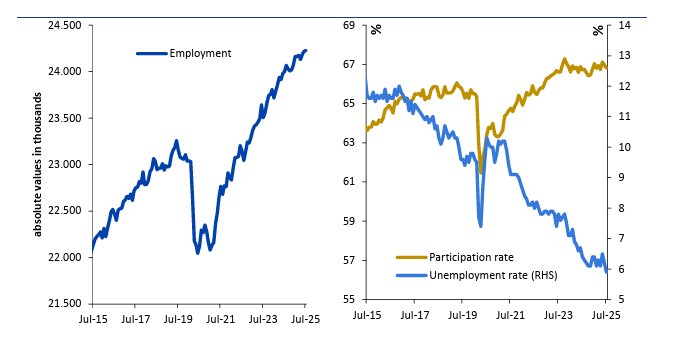

Although a general election is not due until end-2027, PM Meloni may be wary whether her Brothers of Italy Party can remain ahead in opinion polls until then. Already some slippage has been seen and a major constitutional referendum on judicial reform has just been voted against, a result which will very much damage the PM given that she has recently been very much driving the campaign for approval. Notably, electoral concerns may be behind her clear criticism of the U.S. attack on Iran, this all the more notable given the her relatively close relationship with Trump. But her motivation for this more pro-EU stance is that the conflict obviously has consequences for an already lacklustre Italian economy which if sustained could have electoral repercussions too. This is especially so for the consumer which is relatively more exposed to swings in energy. At this juncture, however, we see limited additional price pressures feeding through but CPI inflation this year may jump to 1.9%, 0.4 ppt higher than pre-conflict and largely stay there in 2027, albeit with a declining trend through the year. Regardless, this will have real economy consequences with our expectation for GDP growth still a meagre 0.6% for this year, boosted both by the Winter Olympics and by base effects after the solid end of 2025, though where that was a result of what may have been a large and possibly involuntary inventory build. Notably, into 2026, fixed investment is set to accelerate, buoyed by EU RRF-backed non-residential construction projects, this offsetting a housing investment outlook still retreating, as the phasing out of tax credits is only partly offset by privately funded works. There are upside risks too; Italy’s large arms exports (5% of the global market) may benefit from rising EU defense spending while household consumption, helped by a solid labor market (Figure 5 highlights record-high labor force participation) may still see actual real wage growth if our CPI projections prove anything like accurate. On the downside, over and beyond the tariff impact, bank lending is showing barely any positive growth in the corporate sector – this possibly as much a result of bank wariness amid stubborn non-performing loans of firms. Another downside risk is that the wind-down of the Superbonus actually triggers a larger and more persistent contraction in housing investment, the latter having been a key source of growth over 2021-23

Of course, such forecasts are tinged with even greater risks, these including the possibility that an Italian government becomes more mindful of next year’s election could decide to provide fiscal support to households. Admittedly, and as suggested elsewhere in this chapter it is not just Italy that may go down this avenue, but it may still perturb markets where fiscal worries seem contained but they are far from resolved

Figure 5: Record Labour Participation

Source: ISTAT

Partly this reflects genuine fiscal improvements, including a primary fiscal surplus, though largely a one-off result of the unwind the Superbonus scheme. But the government debt ratio still rose 2.4 points to over 137% last year and would rise further and faster if the government used apparent ‘fiscal space’ - the budget gap is officially expected to drop below 3% of GDP this year and inch lower into 2027. The bottom line is that while hardly yet in a fiscal vicious circle, budgetary dynamics are hardly friendly and that is without the added formidable challenges in meeting Italy’s NATO defence spending commitments (which at face value could ramp the debt ratio much higher and much earlier).

Spain: Trump vs Sanchez?

Like the rest of Europe, Spain is very much sensitive to the Middle East conflict. Under our main assumption of limited further fighting, we see GDP growth of just 1.7% this year, a clear contrast to the 2.8% 2025 figure. Admittedly, that is little changed from the view of three months ago but that is mainly due a more solid base effect caused by a more upbeat GDP outcome last quarter. Indeed, the q/q pattern we now envisage results is annualised growth of 1% with that for the current quarter possibly even weaker, hit by the severe storms seen into February. A better quarterly profile emerges into 2027 but with average growth still of 1.7%. And there may be downside risks to both years especially given the possibility that even if the current conflict ends relatively soon as we assume, Spain may come under fresh attack from the Trump administration seeking retaliation for Prime Minister Pedro Sánchez’s refusal to let U.S. military use jointly operated air bases on Spanish soil to attack Iran – NB this this was widely accepted by most Spanish political parties – this partly posturing ahead of the looming general election due no later than August this year. Notably, while very much having warned the EU of higher and maybe wider tariffs, Trump and Treasury Secretary Bessent threatened specifically to cut all trade ties with Spain. This may be more bluster than reality, not least as it would be hard for the U.S. to target Spain given its membership of the EU. But the risks are there and they may be sizeable given how vulnerable the country would be to a U.S. trade embargo. Admittedly, less than 1% of GDP stems from exports to the U.S., less than half the EZ average. But on the import side, the U.S. is Spain’s leading supplier of fossil fuels providing some 15% of crude oil and three times that of LNG imports. There are also the risks of financial sanctions on Spain, this notable given that Spain’s largest bank, Santander, is trying to increase its exposure to the US banking sector.

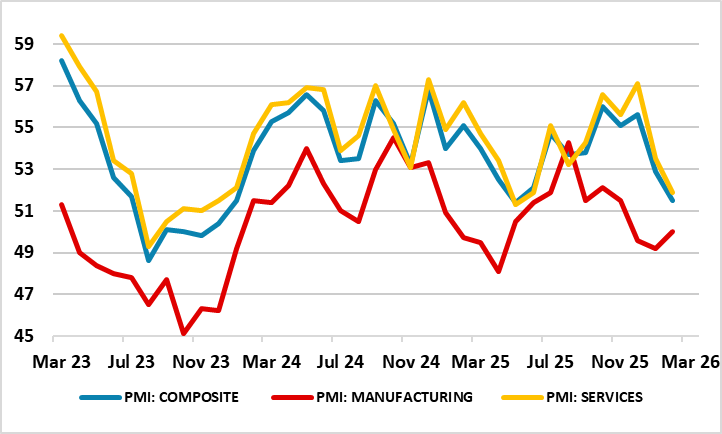

Regardless of how trade relations with the U.S. shift, Spain’s economy is already being affected by the attack on Iran and with surveys having suggested a slowing in activity already underway (Figure 6). Energy prices are already rising across the board, and although at this juncture we see limited second round effects, we have lifted our CPI projection this year by 0.5 ppt to 2.4%, but with little change to 2027 forecast of 2.1%. This will obviously have an adverse effect on real incomes with an added negative the likely impact on sentiment too. But there is also the likely negative impact on the tourist industry and not just from far less solid economic activity by Spain’s key trading partners but also from higher airfares and hotel costs, albeit some upside as some boost may come from tourism re-routed from the Gulf.

Figure 6: Economy Already Weakening?

Source: Markit, % balance

And these risks are superimposed over what may be more structural issues; Spain is very much in the hot seat when it comes to climate change, having suffered clear damage from storms, heatwaves and drought. There is also going to be no rapid defence build-up, amid an aversion to the military. The main one, however, being a more-pronounced-than-anticipated slowdown of migration flows will reduce the dynamism of the labour market, explaining the pared back outlook we have for private consumption and investment. Indeed, migration flows may see growth of over 3% last year but give way to nearer 2% this year and something similar into 2027. This may still feed what has been strong import growth of late meaning we see the current account deficit in 2026 and 2027 staying at the narrower circa 2.7% we see for 2025.

This demographic backdrop, almost unique to Spain within the EU, is best understood by the fact that per capita GDP growth last year was around 1.5%, admittedly still well above the EZ average, but highlighting the extent to which population and workforce growth have been supporting activity – NB productivity has been a more anaemic 0.5% which we think will persist into 2027, thereby reining back potential growth from its current circa 2.5%. But the clear beneficiary of this very solid overall GDP backdrop of recent years has been the marked swing on the fiscal side which had seen persistent budget gaps of around 7% of GDP a decade ago give way to a deficit last year just under 3%. This may even rise back this year however, given the weak economy and possible fiscal aid to households.

I,Andrew Wroblewski, the Senior Economist Western Europe declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.