Marginal Fall in October: Turkiye’s CPI Cooled off to 48.1% YoY

Bottom line: After CPI plummeted to 49.4% y/y in September backed by the lagged impacts of the tightening cycle, relative slowdown in credit growth, and tighter fiscal stance, inflation hit 48.6% in October as food, education and rental pricing pressures continued to build while the deceleration pace in inflation significantly decreased. We envisage the falling trend will marginally continue in the rest of Q4 supported by moderate slowdown in domestic demand and credit growth despite services inflation remains sticky. Our end-year inflation remains at 43-44% despite Central Bank of Republic of Turkiye’s (CBRT) end-2024 prediction is 38%.

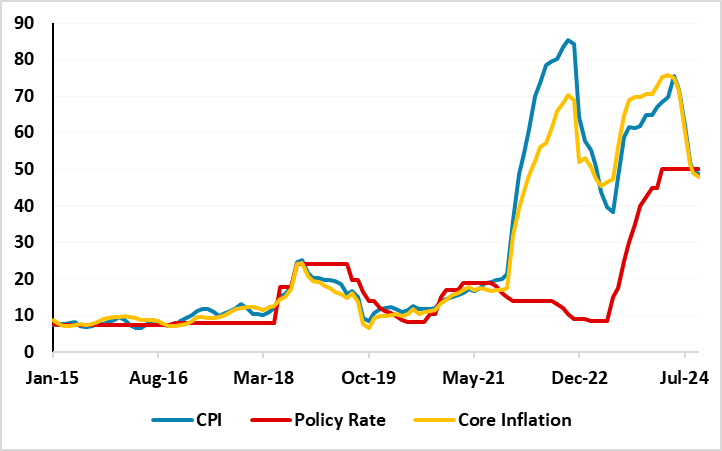

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – October 2024

Source: Continuum Economics

As we expected the deceleration trend in inflation continued in October supported by moderate slowdown in domestic demand and relative TRY stability. (Note: TRY lost 0.3% of its value against the U.S. dollar in October.) CPI cooled off to 48.6% y/y in October from 49.4% in September but slower less-than-expected as market expectations were centred around 48.1%.

When annual rate of changes (%) in the CPI’s main groups are examined in October, transportation with 26.1% was the main group with the lowest annual increase while education recorded the highest annual increase with 93.7%. It is worth mentioning that housing (89.4%), hotels, cafes and restaurants (62.1%) also recorded remarkable YoY increases. Food costs were among the biggest movers rising 4.3% in October, with housing costs up 2.9% for the month. MoM Inflation rose by 2.88% in October as monthly inflation remains sticky at around 3% in the last months.

Core inflation (CPI-C) recorded a 2.8% MoM increase, scaling up to 47.8% on an annual basis. The domestic PPI was up 1.3% MoM in October for an annual rise of 32.2%, the data showed.

Despite CBRT predicts inflation will to fall to 38% and 14% at end-2024 and end-2025, respectively, and medium-term program (MTP) sees end-2024 and 2025 inflation of 41.5% and 17.5% respectively, we predict end-year inflation will likely hit around 43-44% given high inflation expectations, stickiness in services inflation, and geopolitical risks keep inflation pressures alive.

In this regard, CBRT recently reiterated that its tight monetary stance is expected to lead to i) a decline in the underlying trend of monthly inflation by moderating domestic demand, ii) real appreciation in the TRY, and ii) improvement in inflation expectations. As there is a growing uncertainty about the disinflation process, particularly after August due to inflation easing only marginally in Q3, we feel this will cause CBRT to hold the policy rate unchanged at 50% in the rest of 2024.

We expect cautious and hawkish CBRT to start cutting rates in Q1 2025, if inflation trajectory allows in Q4 and there is a permanent improvement in annual CPI as signalled by CBRT deputy governor Cevdet Akcay who recently emphasized “We will stay tight until the underlying trend of monthly inflation comes down on a sustainable basis.” (Note: Our end year key rate prediction is 50.0% for 2024, and 30.0% for 2025 given residual inflationary risks, and we believe 500bps cuts in every quarter in 2025).

As CPI softened in Q3 and early Q4 ignited by lagged impacts of aggressive tightening, slowdown in credit growth and relative TRY stability underpinning the inflation relief, we envisage that inflation will continue to decelerate during the rest of Q4, but the extent of the decline will be determined by administrative price adjustments, TRY volatility and tax adjustments.