China: PBOC Slow Cuts with 5% Nominal GDP

• The PBOC will likely cut slowly and gradually, as China seeks to avoid Yuan depreciation that could worsen the trade war with the U.S. Additionally, MOF last week forecast nominal GDP of 5%, which with a real GDP target of 5% means that MOF is also forecasting zero inflation. Close to zero inflation is thus consistent with only slow and 10bps easing steps in the 7-day reverse repo rate in the coming quarters.

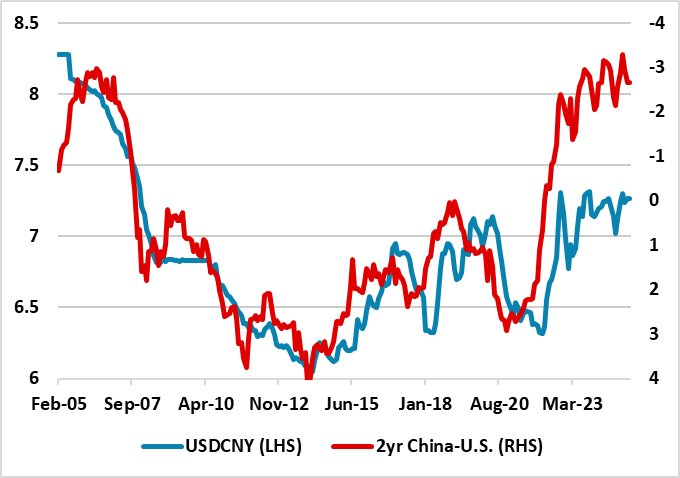

Figure 1: USDCNY and 2yr China-U.S. Government Bond Spread (%)

Source: Datastream/Continuum Economics

Source: Datastream/Continuum Economics

Additional PBOC monetary policy stimulus will likely be slow and gradual in 2025 for a number of reasons.

• Disinflation but 5% Nominal GDP target. The latest February CPI data shows that the aggressive disinflation remains with an excess of production over domestic demand squeezing prices. Though the headline decline of -0.7% was exaggerated due to food price declines, the core inflation rate fell to -0.1% Yr/Yr in February. The breakdown of the data shows the squeeze not only in goods inflation, but also services inflation that declined -0.4% Yr/Yr as consumption remains sluggish. Though the headline figure should rebound in March, we remain of the view that inflation will likely be +0.1% in 2025. However, it is worth noting that MOF last week forecast nominal GDP of 5%, which with a real GDP target of 5% means that MOF is also forecasting zero inflation.

• PBOC slow and gradual. Though the authorities are signalling that further monetary policy easing will be delivered, the pace will likely be slow and gradual. China does not want to widen the interest rate differentials versus the U.S. (Figure 1), as it could weaken the Yuan and prompt more tariffs from President Trump and a delay in the desired trade negotiations with the U.S. This means that the timing of Fed rate cuts will be an issue in determining cuts in the 7-day reverse repo rate currently at 1.5%. China could move ahead of the Fed still, but this will likely be a 10bps move. It could be that only three 10bps cuts are delivered in 2025. Two to three 25bps cuts in the RRR rate are also likely in 2025. Given the balance sheet repair by households, this is small to ineffective monetary policy stimulus.

• Fiscal policy and lending. This places the onus on fiscal policy. However, last week announcements were at the low end of expectations (here). Though policymakers signalled that more fiscal stimulus could be delivered, this will likely be incremental rather than aggressive – part of the delay is too assess the full implementation of trade tariffs by the U.S. Meanwhile, the extra Yuan500bln equity capital for major banks should help credit supply, but China really needs 10% M2 growth to ensure 5% real GDP. Without improved sentiment for households and private businesses, credit demand may not pick up and help delivering a lending boost. Overall, we continue to project 4.5% real GDP growth for 2025 and 2026.