France: Prime Minister – Another One Bites the Dust

Either side of the English Channel, politicians are competing to see whether France or the UK can provide a prime minister with the shortest time in power. In the UK that was Liz Truss whose 49 days at the helm of the government in 2022 has now been surpassed by French PM Lecornu who has resigned less than a month after his appointment, after right-wing allies indicated they would withdraw from his government. This underscores that France now has a problem not only in any President Macron-produced administration staying in power but actually even in forming any fresh government. Given that fiscally, existing budget measures from the previous year will continue, this suggests no immediate fiscal crisis even though the hefty budget cuts markets and Macron is seeking will continue to be elusive. However, three key issues need highlighting.

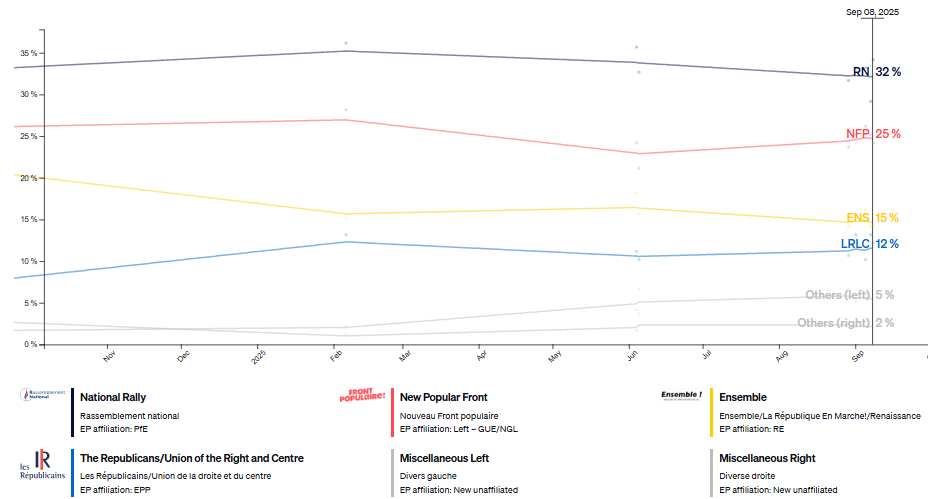

Figure 1: Parliament Divided Three Ways

Source: Politico

First, despite extending existing budget laws, the budget situation is actually getting worse as the French economy buckles, some of which is a reflection of political uncertainty. PMI data very much suggest that the economy is contracting, not least in the very rate sensitive construction sector. Indeed, the PMI numbers for the sector, out today, point to a dearth of new projects, with underlying data signalling a quicker reduction in new order inflows. As a result, the PMI for the sector posted 42.9 in September, down from 46.7 in August, signalling a sharp and accelerated contraction.

Secondly, a fresh election is both unlikely to occur and/or help solve the stand-off in parliament where the French voting system effectively undermines the right-wing National Rally’s opinion poll lead. Instead, and ahead of key local and mayoral election next March, the three-way split within parliament is seeing the various parties concerned via for votes - and this means not backing unpopular budget cuts.

Third, France’s current politics-driven fiscal woes suggests the much vaunted TPI tool that the ECB flaunts is highly unlikely to be used. Luckily for France (at least compared to the UK) it is the current low level of ECB policy rates that is cushioning the French market on a relative basis. Thus with policy rates possibly falling further, whatever surfaces as the next French government can afford to kick the fiscal can further down the road. However, this may be only for the time being as when the ECB starts to tighten afresh, or when/if speculation about such action emerges more forcefully market scrutiny of France will intensify, especially as this may coincide with heightened French political uncertainty in 2027 related to the then-likely presidential election. The question is whether this possibility will make the ECB try and place any such market thinking!

I,Andrew Wroblewski, the Senior Economist Western Europe declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.