EMEA Outlook: Adverse Global Developments and Domestic Uncertainties Dominate

· In South Africa, we foresee average headline inflation will stand at 3.8% and 3.5% in 2026 and 2027, respectively based on our baseline of a 4-8-week war in Iran and energy prices easing from Q2. Upside risks to inflation remain such as 2nd round effects of oil price hikes, utility costs, and logistical constraints. We see growth to be 1.2% and 1.4% in 2026 and 2027, respectively. Risks to the growth outlook are broadly balanced, with faster reform implementation, improved investor sentiment, and no load shedding so far in 2026 representing an upside risk to growth trajectory, while uncertainties about the U.S. and Chinese economies and the risk of a prolonged war in Iran could cause problems. Our end-year policy rate predictions remain at 6.75% for 2026 and 6.25% for 2027.

· In Turkiye, deteriorated pricing behavior, high inflation expectations and sticky services prices continue to risk the disinflationary process coupled with recent rally in energy prices and currency volatility. Our average inflation forecast increased to 28.4% for 2026 due to higher energy price we now forecast. We think Central Bank of Republic of Turkiye (CBRT) will likely cut the key rate to 32% by end-2026, while stubborn inflation and energy prices will limit the size of the cuts. We forecast the economy to expand by 3.3% in 2026 and 3.8% in 2027 backed by robust investments, construction projects and government spending while high inflation, energy prices and tighter fiscal stance will continue to dent growth. A high risk exists that the presidential election could occur Oct-Nov 2027 rather than 2028.

· In Russia, the Ukraine war continues to create high military spending, strong fiscal stimulus in addition to aggravation of staff shortages. Our baseline scenario in Ukraine is the war dragging on throughtout 2026 (70%) and the alternative is a Russia friendly peace deal (30%) likely in 2027. Our 2026 average headline inflation forecast is 5.9% YoY owing to lagged impacts of previous aggressive monetary tightening, and relative resilience of RUB despite sanctions and supply chain inefficiencies. Our end-year policy rate prediction stands at 13% for 2026 as we foresee Central Bank of Russia (CBR) will continue its easing cycle the rest of 2026, but with a slower pace. We envisage growth to hit 1.1% in 2026 as higher oil prices in Q2/Q3 and temporary sanctions relief could boost Russia crude exports to help relieve fiscal pressures and stimulate growth.

Forecast changes: From our December outlook, we lifted our 2026 end-year key policy rate for Turkiye to 32.0% due to stubborn inflation and recent hikes in oil prices; and hiked our 2026 average inflation forecast for Turkiye to 28.4% due to inflationary risks and sticky services (particularly education and housing) prices. We slightly decreased 2026 growth forecasts for South Africa and Turkiye due to 2nd round effects of energy price surges.

Fragmentation in EMEA: Geopolitical Headwinds, Energy Volatility and Diverse Domestic Dynamics

We believe the volatile energy prices, global trade tariffs, slowing Chinese economy, ongoing wars in Iran and Ukraine and country‑specific dynamics will continue to shape the EMEA outlook. Geopolitical tensions remain elevated, also leaving EM markets jittery and impact financing of global imbalances. Based on our baseline of a 4-8-week war in Iran, energy prices should be easing from Q2. Even so, the pace of monetary easing across EMEA remains uneven, reflecting differing progress toward inflation targets and varying domestic conditions.

Although not our primary in-house scenario, a multi-month conflict in Iran would likely trigger stagflationary shocks that could hurt GDP growth as well as boosting inflation more than our baseline forecasts. If the Iran war drags on for months, energy costs could rise putting pressure also on the current account balances for EM countries as capital flows could weaken. This could particularly put further downward pressure on the ZAR and TRY. (Note: With oil prices potentially surging toward USD 120–130, EM central banks might be forced to cancel planned interest rate cuts or, in some cases, implement modest rate hikes to counteract second-round inflationary effects. EM central banks will likely want to avoid rate hikes if the war is 4-8 weeks.

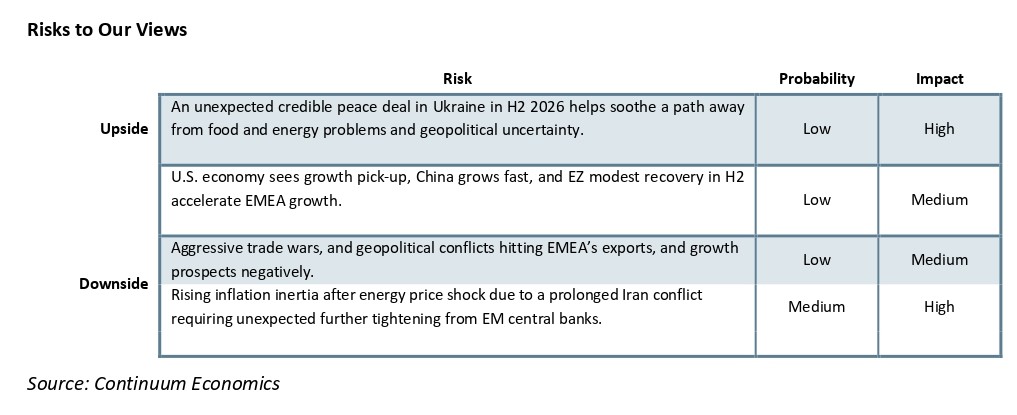

Figure 1: South Africa, Russia (LHS) and Turkiye Inflation (RHS) (%, YoY), January 2010 – March 2026

Source: Continuum Economics, Datastream

South Africa

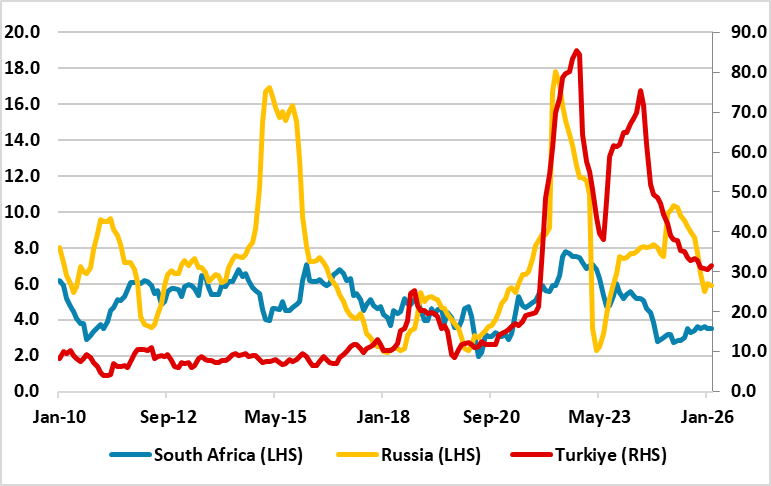

South Africa had enjoyed moderate inflation remaining within SARB’s target band of 2% and 4%. Annual inflation stood at 3.5% YoY in February supported by suspended power cuts (loadshedding), stronger ZAR, lower oil prices and decrease in inflation expectations. In Q1 2026 (the second survey after the inflation target changed to 3%), the average five-year inflation expectations declined slightly to a record low of 3.6% (from 3.7% previously). Next-year inflation expectations also declined marginally from 3.7% to 3.6%.

The macroeconomic outlook remains positive owing to moderate progress on reforms. South Africa was officially removed from the Financial Action Task Force's (FATF) greylist in October and the country securing its first credit rating upgrade in two decades in November were significant developments. We believe there is potential for further improvement in fiscal metrics and debt stabilization. While the November medium-term budget update signaled that government debt is coming under control and the fiscal situation is stable, the ongoing conflict in Iran could shift this outlook. Gasoline prices will rise and produce a temporary increase in CPI in Q2. However, this time around power cuts may not amplify the energy hit.

On the power cuts front, South Africa’s national electricity utility company Eskom announced on March 13 that South Africa has now experienced 300 consecutive days without an interrupted supply, with only 26 hours of loadshedding recorded in April and May and the energy availability factor (EAF) rose to 65.85% for the financial year to date (April 1, 2025 to February 12, 2026). Despite no load shedding so far in 2026, some energy analysts think blackouts are still a threat and further power disruptions are likely while continued investment build out of energy infrastructure remain the key.

Despite this, services inflation remains concerning as it stays above 4%. The SARB aims to see CPI moving closer to the 3% target, establishing low inflation as the new normal for South Africa. However, the recent spike in oil prices—alongside rising utility costs—is expected to hinder this progress. We anticipate that a weakening rand, driven by higher oil prices and surging food costs (due to increased fertilizer expenses), will likely push inflation over 4% in Q2/Q3. Any climate-related agricultural disruptions will worsen the situation. Consequently, we expect convergence to the 3% target will be slower than initially projected. While we expect inflation to ease in late Q3/Q4 as the Iran conflict potentially subsides, but this recovery will take time. Accordingly, interest rates are likely to remain unchanged at 6.75% in the near term.

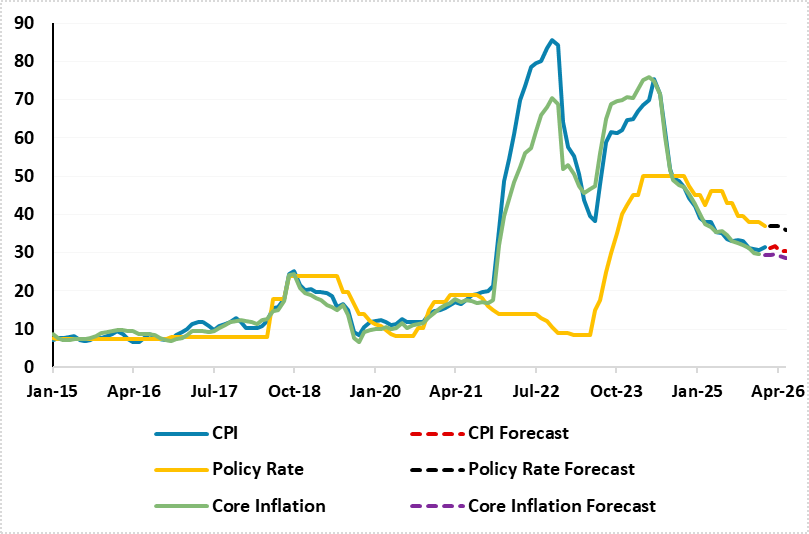

Figure 2: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2010 – June 2026

Source: Continuum Economics

Under current conditions, we forecast that average inflation will reach 3.8% in 2026 and 3.5% in 2027, supported in part by the lagging effects of previous monetary tightening. We believe the inflation trajectory will be driven primarily by global developments, trade tariffs, and the government’s commitment to addressing electricity shortages, logistical constraints, and financing requirements.

Thus, we think SARB will likely halt its cutting cycle H1. We expect SARB could consider reducing the rates in H2 2026, which will depend on the inflation trajectory, though this is not our baseline scenario since SARB will likely act cautious against any expected inflation uptick taking the new inflation target into consideration. Our end-year key rate predictions remain at 6.75% and 6.25% for 2026 and 2027, respectively. SARB will likely continue cuts in 2027 once the Iran conflict loses momentum, most of the geopolitical risk premium dissipates and oil prices decline with market dynamics.

Meanwhile, political friction, slow reforms, and fiscal slippage remain key internal risks. Although some analysts forecast the ANC-DA coalition will collapse before 2029, our baseline scenario assumes it will remain intact.

South Africa’s growth looks stable, with the economy having expanded for four consecutive quarters, driven by household consumption. The economy expanded by 1.1% in 2025 —its fastest pace in three years—supported by the agriculture, trade, and finance sectors. Despite SARB forecasts growth moving higher and approaching 2% over the medium term due to sustained investment recovery, we assess growth to hit 1.2% in 2026 on the back of improved investor sentiment supported by lower rates compared to recent years, and no loadshedding while energy costs, expected surge in inflation and logistical constrains could limit the growth trajectory.

Domestic factors such as persistent structural challenges such as unemployment and lack of fiscal space will continue to temper the outlook. (note: Unemployment remains stubbornly high in South Africa, which require urgent labor market reforms to unlock inclusive growth. We think continued implementation of Operation Vulindlela reforms - targeting energy, logistics, water, and digital infrastructure – will also be key to unlocking productivity and competitiveness). Further gains in economic performance would come from reaching a prudent public debt level, lowering administered price inflation, and continuing structural reforms that raise potential growth.

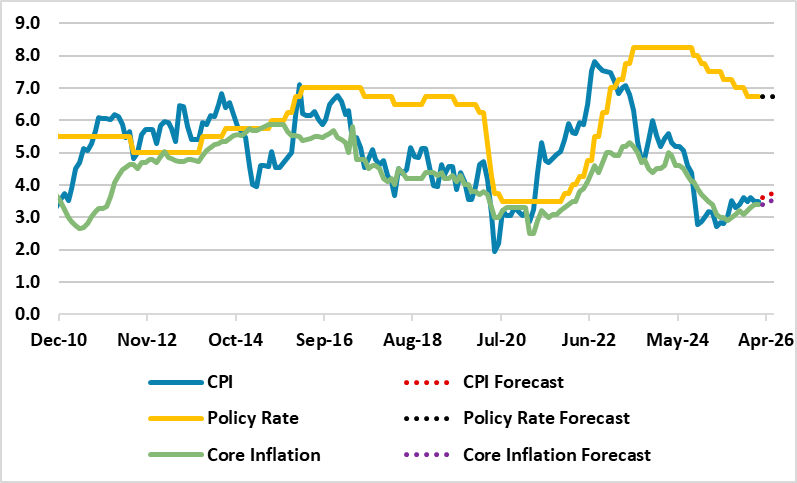

Figure 3: SARB Interest Rate Forecast (%), 2019 – 2028

Source: SARB Forecast Report (January 2026)

Turkiye

Annual inflation slightly edged up to 31.5% in February due to rising food, transportation and housing prices. Despite this we expected the underlying inflation (tight money and fiscal policies) slowdown to continue very moderately, though the pace is slow. Inflation expectations also remain elevated in Turkiye underscored by the CBRT’s release of its inaugural Household Expectations Survey on February 24, which revealed that households' 12-month-ahead inflation expectations held steady at 48.8%, while their expectation for the USD/TRY exchange rate reached 51.56 over the same period.

In its first inflation report of 2026, the CBRT maintained its official interim target of 16%. However, the regulator notably shifted the forecast range upward to 15%–21% (from the previous 13%–19%). Additionally, the bank raised its 2026 food inflation forecast from 18% to 19%. Under current circumstances, we assess CBRT would consider cutting rates very moderately in Q2/Q3 due to energy price risks. Any further potential upside surprises in food and energy prices could derail the recovery.

However, we think that inflation is likely to remain above the CBRT’s upper forecast band by year-end. Our average inflation forecast for 2026 has increased to 28.4% when compared with 26.5% in December outlook. We continue to envisage it will be difficult to grind sticky inflation from 30%s to 10%s rapidly, taking into account that inflation (especially services) has become stickier and requiring high nominal and real interest rates to remain for some time. Inflation expectations and pricing behavior remain high. We feel TRY also remains exposed to any major changes in the global risk sentiment and domestic political shifts, while a sudden depreciation could easily reverse disinflation gains. (Note: Opposition’s presidential candidate, Ekrem Imamoglu is still in jail and prosecutors accuse Imamoglu of 142 corruption offences that command jail terms ranging from 828 to 2,352 years).

Although not our primary in-house scenario, a multi-month conflict in Iran could hurt Turkiye GDP growth as well as boosting inflation more than our baseline. If Iran war drags on for months, energy costs could rise and also cause current account deficit of Turkiye to widen. We think capital flows could weaken and risk premiums could increase coupled with loss of investor confidence. The other risks for Turkiye stemming from war in Iran include rising transportation costs, delivery delays and declining export competitiveness across multiple sectors. Higher energy prices and logistical disruptions push fertilizer costs up further, increasing production costs for key crops such as wheat, corn and sunflower and potentially feeding into food inflation. These could also put downward pressure on the TRY. (Note: It is worth noting that with oil prices potentially surging toward USD 120–130 in this scenario, that the CBRT might be forced to cancel planned interest rate cuts or implement modest rate hikes to counteract second-round inflationary effects).

It appears it would be necessary to make concessions on growth to achieve inflation in the 10 percent’s, but this remains unlikely. We anticipate domestic risks will keep inflation pressures alive for a longer period, and it will be very unlikely to reach a single digit inflation by 2028 despite CBRT’s expectations. (Note: An unexpected end to the Russia-Ukraine war in 2026 would provide downward pressure on Turkish inflation, though this is not our baseline scenario).

Despite CBRT cut the policy rate by 100 bps to 37% during the MPC meeting on January 22, the regulator halted the easing cycle on March 12 due to adverse global developments and CPI inflation surge in February. We expect CBRT will continue its cutting cycle in 2026, but with caution due to inflation risks. Our end-year key rate prediction for 2026 has increased to 32% from 29% in the December outlook due to stubborn inflation and hikes in energy prices. CBRT will likely accelerate cuts in 2027 once the Iran conflict loses momentum, most of the geopolitical risk premium dissipates and oil prices realigns with market dynamics.

It is worth mentioning that parliamentary elections in Turkiye are scheduled to occur no later than May 14, 2028, alongside presidential elections. We expect the elections to be held in October/November 2027, earlier than the scheduled time. This timing is critical, as an early election called by Parliament is the only constitutional path for President Erdogan to seek another term. It will not be surprising if Erdogan would want a faster easing cycle in 2027 aiming to pump up the economy, which could significantly change CBRT’s plans for 2027 and onwards.

Another major issue related to CBRT is its credibility. Taking into account that sustained economic recovery hinges on the independence of the CBRT and rule-of-law reforms, we think any backsliding could easily trigger market volatility. There is serious domestic criticism about the credibility of the CBRT since inflation continues to significantly deviate from the CBRT’s targets, CBRT changes inflation targets frequently and CBRT’s decisions are partly controlled by the current government, particularly in the last five years, causing CBRT’s forward communication to be weak and discredited.

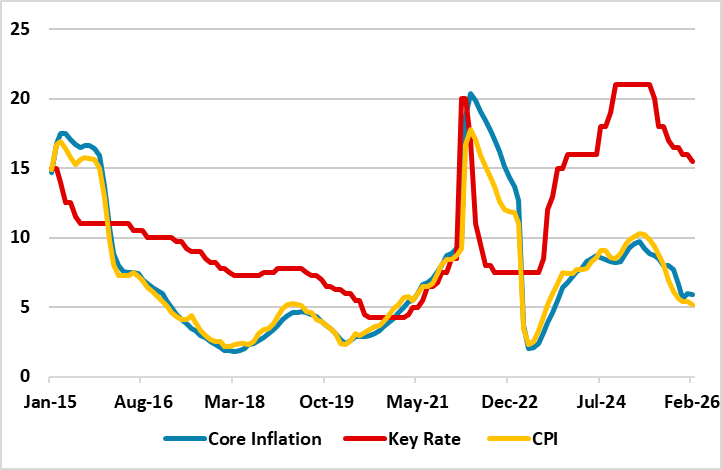

Figure 4: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – April 2026

Source: Continuum Economics

Despite the weight of high interest rates and inflation continue to dominate growth outlook, the Turkish economy expanded by 3.6% y/y in 2025, underpinned by domestic demand while the main drag came from net trade. We think 2026 growth will be likely be less than 2025, hitting 3.3% y/y due to tight monetary and income policies coupled with adverse impacts of energy costs, while resilient household consumption and infrastructure projects will be the main growth drivers. (Note: The government has launched the Century Housing Project, a major initiative to build 500,000 social housing units across all 81 provinces in addition to ongoing construction projects for the ones affected from earthquakes in 2023).

We foresee 2027 growth will likely be higher than 2026 with 3.8% supported by increasing business confidence helped by the positive impact of the rate cuts assuming no dramatic impact from weaker external demand and no major political turbulence. We think a decline in the inflation rate and rate cuts could boost confidence in the medium term, coupled with accelerated structural reforms, and stable global conditions could lift growth back toward potential of around 4% after 2027/28.

On the other side of the coin, tight monetary and income policies, any unexpected resurgence of inflation, any accelerated TRY depreciation, and high interest rates could derail the recovery and reignite macro instability. There is still a downside risk that growth can be lower than expected, particularly considering all the tightening measures in place, though elections late 2027 could trigger increase in government spending and growth.

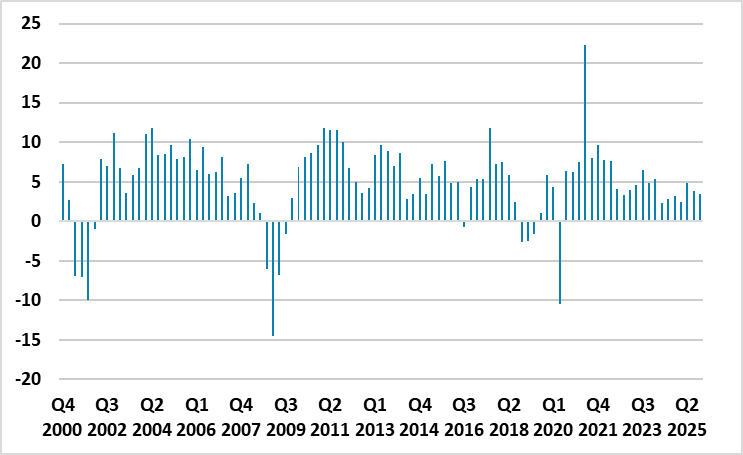

Figure 5: GDP Growth (%, YoY), Q1 2000 – Q4 2025

Source: Continuum Economics

Russia

The Russian economy continues to navigate structural challenges, ranging from persistent sanctions and supply chain fragmentation to demographic decline and fiscal volatility. The overall environment for doing business in and with Russia also remains unfavorable, while the conflict in Ukraine is the primary determinant of the economic outlook.

On the inflation front, CPI moderately down to 5.9% y/y in February owing to the lagged impacts of previous tight monetary policy and the relatively resilient RUB. Our CPI forecasts stand at 5.9% and 5.2% in 2026 and 2027 since we expect inflation will continue to soften as previous tight monetary policy affect bank lending and private consumption. High domestic gas and oil production will curtail domestic energy prices in contrast to global energy prices. Higher global oil prices in Q2/Q3 and temporary sanctions relief due to the Iran conflict could boost Russia crude exports help relieve fiscal pressures, and stimulate growth. (Note: Higher oil revenues may facilitate expanded military spending, potentially triggering demand-pull inflation. Conversely, they could moderately decelerate inflation via the FX channel, although the impact of sanctions would likely limit this effect. We expect the net result to be a secondary rather than a dominant factor).

Though CBR is projecting that inflation returns to the 4.5-5.5% target in 2026, we think reaching this target will be tough due to continued military spending, labor shortages, and supply-chain disruptions coupled with adverse effects of the value-added tax (VAT) increase in 2026 and excise taxes. Backed by a softening inflation, CBR continues its easing cycle in 2026 and reduced the key rate to 15% per annum on March 20 highlighting inflationary pressures continue to decline despite risks. We think CBR will likely resume cutting rates (moderately) if the inflation trajectory allows, RUB stabilizes and inflation expectations converge towards CBR’s forecasts. Our end-year key rate forecast is at 13% and 10.5% for 2026 and 2027, respectively. Russia will have to keep rates high as the country need higher real yields. As an alternative scenario, we think a faster CBR easing cycle is possible in 2027, if a full scale peace deal is signed in Ukraine relieving the Russian economy and Putin wants a domestic demand boost as military spending slows.

As mentioned, the inflation trajectory and rate decisions will depend on how peace negotiations in Ukraine will proceed. A peace deal could help Russian economy to feel relief since military spending growth will slow; RUB will likely strengthen, average headline inflation will soften, and fiscal pressure will ease, particularly if sanctions will be lifted.

The probability of the conflict in Ukraine continuing throughout 2026 has risen to 70%. This shift is driven by a pivot in Washington’s attention toward the escalating conflict with Iran, which has effectively sidelined Ukraine on the U.S. foreign policy agenda. Furthermore, the battlefield remains in a state of grinding attrition, with limited tactical breakthroughs and significant unresolved issues, most notably the status of the eastern Donbas and territories in the eastern oblasts. While the Trump administration previously aimed for a swift resolution, current mediation efforts have reached a zone of stagnation. A Russia-friendly peace deal is now viewed as a lower-probability outcome (30%) for the near term, likely slipping into 2027. This timeline reflects the exhaustion of both parties and the complexity of revising the current 28-point framework. We continue to think Ukraine remains in a weaker negotiating place and, at some point Ukraine will have to admit giving up some land to Russia. Under this Russia-friendly peace deal framework, the deal would likely involve Russia annexing parts of the four occupied Ukrainian oblasts while securing a commitment that Ukraine will not join NATO or host foreign troops.

Figure 6: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – February 2026

Source: Continuum Economics

When it comes to growth, the main driver for Russian GDP growth remains the surge in military spending, supported by the improved consumer demand amid greater outlays on social support, higher wages and strong fiscal stimulus. Russia's GDP expanded by a moderate 1.0% y/y in 2025 showing the economic slowdown in Russia is more evident now. Central Bank of Russia’s previous aggressive monetary tightening coupled with sanctions, supply side constraints, relative RUB resilience, low crude oil prices and stubborn price pressures are all economic headwinds.

Despite sanctions, Russia maintains energy export flows to non-Western markets, particularly China, India, and parts of Africa. Russia is currently the primary beneficiary of the disruption in the Middle East, specifically due to the closure of the Strait of Hormuz. Hikes in oil prices will partly stabilize the current war economy but does not address the underlying destruction of Russia's productive capacity. Capacity utilization reached its maximum in years, and labor force supply problems due to troop call ups is unlikely to change in the near term.

We envisage growth to hit 1.1% and 1.4% in 2026 and 2027, respectively, as the previous tightening cycle is still feeding through and easing effects will only come through fully into H2 2027/2028. The key for Russian economic growth in the next few years will be if a deal in Ukraine will be sealed, when (and which) sanctions will be lifted and the duration of Iran war.