Turkiye’s Inflation Slightly Decreased in March

Bottom line: Turkish Statistical Institute (TUIK) announced on April 3 that the inflation softened to 38.1% y/y in March from 39.1% y/y in February. We think favourable base effect, lagged impacts of previous tightening, relative Turkish lira (TRY) stability until March 20 and suppressed wages continued to relieve the price pressure. Taking into account that March’s inflation print demonstrated that fall in the inflation moderately resumed, we think Central Bank of Turkiye (CBRT) will likely continue its cutting cycle during the next MPC scheduled on April 17 reducing the key rate by another 250 bps to 40% despite unpredictable global outlook following Trump tariffs and domestic political unrest could also cause CBRT to keep rates stable at 42.5%.

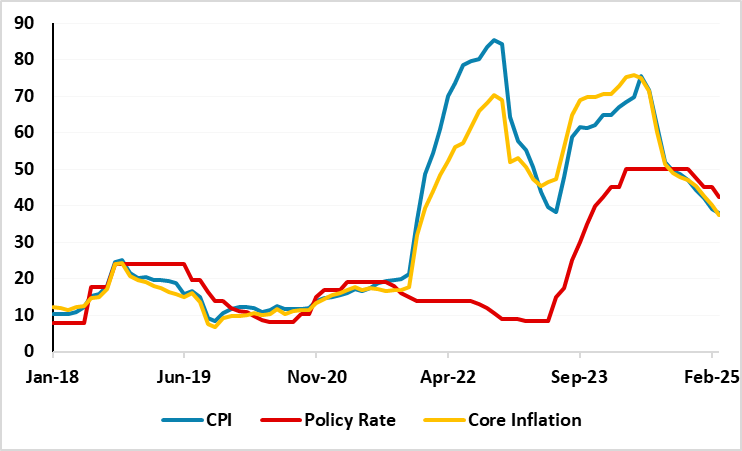

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2018 – March 2025

Source: Continuum Economics

The deceleration trend in inflation continued in Turkiye in March and inflation stood below forecasts as the inflation rate softened for ten consecutive months, marking its lowest level since December 2022. CPI cooled off to 38.1% y/y March from 39.1% in February with food, education and housing prices leading the rise in the index. MoM inflation rose by 2.46% in March, higher than 2.27% MoM inflation the previous month. Core inflation rose by 1.5% MoM, bringing the annual rate down to 37.4%, which has been supported by the relatively stable foreign exchange basket and the positive outlook for PPI. (Note: PPI came in 1.9% MoM, showing a drop to 23.5% on same month of the previous year basis).

Education prices recorded the highest annual increase with 80.4% YoY followed by housing prices were up by 68.6% YoY. Prices rose at a slower pace across a number of categories, such as footwear and clothing, which came in at 14.8% YoY in March, down from 20.8% YoY in the previous month. Transport inflation dropped to 21.6% YoY in March, down from 23.4% YoY in February. Energy prices surged by 42.0% at an annualized pace in March, eased from 43.9% in February.

We think lagged impacts of previous monetary tightening, favourable base effect, relative Turkish lira (TRY) stability until March 20, and less-than-expected hike in minimum wage in January coupled with Turkish regulation lowering patients’ co-payments at public hospitals helped relieving the price pressure in March.

Speaking about the inflation figure, Treasury and Finance Minister Mehmet Simsek said on April 3 that “We expect the impact of the recent volatility in the markets (following the arrest of Istanbul mayor) on inflation to be limited by tightening financial conditions.”

Taking into account that March’s inflation print demonstrated that fall in in the inflation rate moderately resumed, we think Central Bank of Turkiye (CBRT) will likely continue its cutting cycle during the next MPC scheduled on April 17 reducing the key rate by another 250 bps to 40% despite domestic inflation trajectory and unpredictable outlook for the global economy particularly after Trump tariffs continue to pose risks.

Additionally, we think the arrest of mayor of Istanbul on March 23 could risk the disinflationary process particularly if TRY plunges considering the political unrest and protest continue in Turkiye. (Note: We fell the CBRT could also consider halting the easing cycle at some point if inflationary impacts will dominate in Q2). It is difficult to foresee how domestic economy will be affected from political uncertainties in the next months. We envisage April and May inflation could be higher-than-expected due to currency losing value particularly after Imamoglu’s arrest.