UK CPI Preview (Oct 16): Inflation Below Target – BoE Splits Widen?

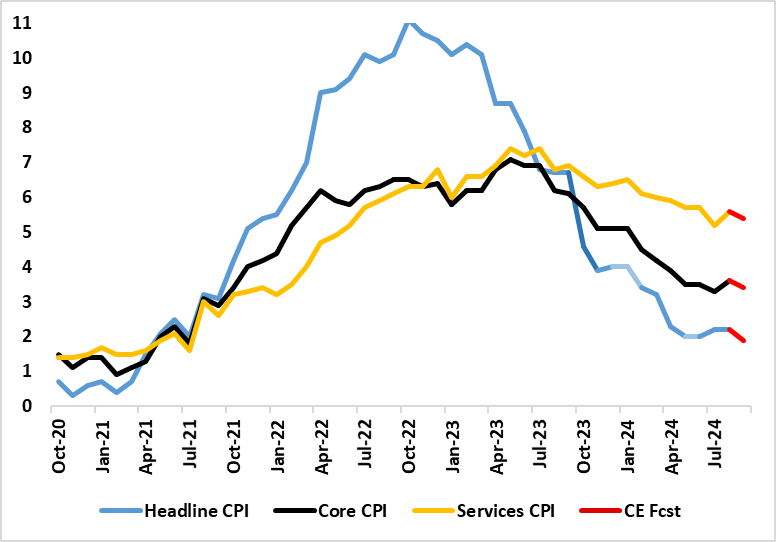

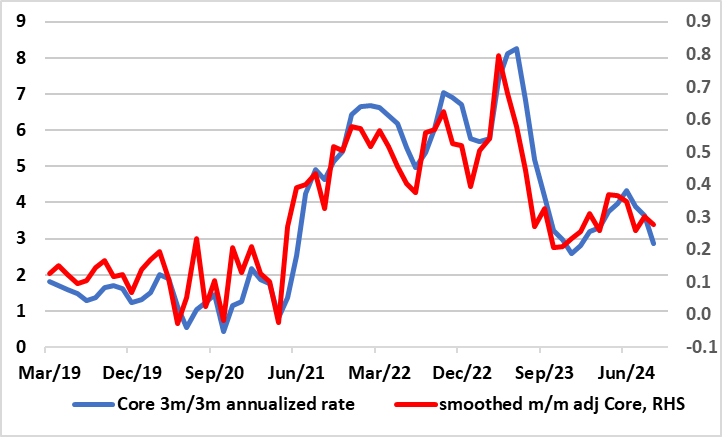

Helped by a fall in fuel prices, amplified by base effects, alongside some belated softening in services costs, UK inflation may drop to 1.9% in the September CPI (from 2.2%), thus falling below target since April 2021. Admittedly, the drop in services may be limited to a notch lower from September’s 5.6%, with the core falling similarly from 3.6% (Figure 1). Moreover, the drop in the headline is likely to be short-lived as this month’s rise in the energy price cap and a recovery in fuel prices may pull the headline rate back to around 2.3% in October and average a little higher for the whole of Q4. Regardless, the data backdrop is consistent with underlying inflation having fallen, especially when assessed in shorter-term dynamics (Figure 2). As such a CPI picture, now weaker than BoE thinking, should not prevent the much-vaunted Bank Rate cut at the looming November MPC meeting. But as for a possible further mover as soon as the December MPC meeting this is still a possibility rather than probability not least given apparent splits within the BoE hierarchy.

Figure 1: Broad Inflation Drop Ahead?

Source: ONS, Continuum Economics

The July CPI was notable for the clear and larger-than-expected fall in services inflation, one driven by a fall in restaurant/hotel inflation, this often seen as a bellwether indicator of price persistence. The August data showed mixed signs on such a basis as the overall CPI headline rate stayed at 2.2%, this chiming with the consensus and two notches under BoE thinking. Indeed, services inflation rose back 0.4 ppt to 5.6%, up from a two-year low but still below the BoE projection and was almost solely driven by a swing in (very volatile) airfares without which services would have fallen below 5% - this also accounting for the rise in the core rate. Moreover, restaurant inflation hit a new cycle low amid generally softer price pressures in which eight (of 12) CPI components fell.

BoE Debate

This is unlikely to have been the motivation behind BoE Governor Bailey’s interview last week in which he hinted that the BoE could be more aggressive in its easing cycle ahead. Admittedly, there are better signs in underlying services may have been influential. The headline measure of services inflation has been driven mainly by volatile and indexed categories of late, so the MPC has built a gauge that excludes those categories and this has seemingly fallen more markedly. But this has not persuaded his colleague and BoE Chief Economist Pill from citing policy caution ahead, with an apparent very open split emerging between the two principal members if the MPC about how gradual a rate easing cycle may be.

Figure 2: Adjusted Core CPI Pressures Falling Afresh

Source: ONS, Continuum Economics, smoothed is 3 mth mov average

This split is unlikely to prevent a rate cut next month, but if this involves another formal dissent from Pill, then a further easing in December would be more problematic. Indeed, the question is for how long could Pill formally dissent against an MPC majority, especially as his speech last week seemingly questioned the validity not only of the BoE’s formal CPI projections but also some of the assumption that his MPC colleagues had agreed (most notably whether the neutral policy rate has risen of late or not). Of course, other considerations will be important, not least the extent and speed to which other DM central banks may ease policy. This is linked to downside growth risks, which may be spilling over to the UK somewhat sooner and more sizably than the BoE has expected. The fiscal backdrop is also uncertain as the looming October 30 Budget could easily see a possible easing of the currently planned fiscal tightening even with some likely tax rises. Overall, the Nov 7 BoE policy decision will be more important for what is said, than done, especially as it seems that even a further projected undershoot of the inflation target will not placate the MPC hawks!