Outlook Overview: Cyclical and Structural Forces

· The difference between 2nd round inflation effects from higher energy prices and 1st round effects that central banks can look through swings on whether the Straits of Hormuz will remain open in the coming months after the U.S./Iran interim agreement (here). Despite some tensions, we expect the Straits will reopen and remain open. Thus the adverse economic effects and 2nd round inflation effects for most non-Middle Eastern countries will likely be small to modest. This makes it less likely that other central banks following the ECB/SARB/BI in hiking to guard against 2nd round effects and we see the ECB hike being reversed in 2027 – BOJ is on a different rhythm with exiting ultra-easing monetary policy as the focus. The new Fed Chair Warsh removed the easing bias but sees high productivity in the U.S. delivering disinflation. We would also highlight the fragile state of consumption for low and middle income U.S. households (here), which we feel will slow the U.S. economy outside of the tech sector and argues for no hikes. Indeed, as inflation comes down in the U.S. in 2027, we still see two 25bps rate cuts.

· EM central banks will diverge and a few may follow the SARB/BI rate hike to guard against 2nd round effects. However, Brazil will slowly ease given the starting point of already restrictive policy, while Mexico will remain on hold as they do not want to upset the economy. Most EMs are also helped by more labor market slack than 2022. Meanwhile, China has managed to initially prove resilient in the face of the energy price shock from the Iran war, with a reduction in demand/rundown of oil inventories and a switch from LNG to coal for electricity production. However, consumption is soft but no PBOC rate cuts are likely in 2026, as the authorities are concerned about squeezing bank margins too much.

· The structural story from AI also remains an influence, with a healthy boost to U.S. growth from the semiconductor/data center boom. Cyclical productivity has improved in the U.S. but it is difficult to attribute this to AI alone, as tech usage accelerated during and after the COVID pandemic. Policymaking will also face a question of whether some disinflation benefit arrive soon or occur in the coming years and whether the datacenter build out is causing some sectoral inflation. The most critical long-term question is whether net labor shedding will be modest in aggregate (our baseline) or more rapid leading to adverse income/consumption impacts. Our view at this juncture is that the pace is somewhat quicker than the internet revolution that should bring some disinflation benefits in the coming years. However, benefits will be skewed to the U.S. and China where the quickest and broadest AI adoption is occurring.

· Outside of Iran, the odds of a China attack on Taiwan remain at 5-10% for 2026-27, given the very high risks involved (here). Meanwhile, we feel that a Russia-friendly peace deal in Ukraine could eventually arrive by H2 2027 due to exhaustion. Elsewhere, the Donroe doctrine should also be watched closely, as Trump adventurism is likely to still leave him inclined to pressure Cuba and Greenland later this year. We would still suspect that U.S./Europe could find a negotiated solution (here), while Trump will also be preoccupied with the mid-term elections in November. Finally, a multi-day war between India and Pakistan over Kashmir claims is likely in the next 3-12 months, but not a long war.

· For financial markets, the U.S./Iran interim agreement removes the worst case scenario of prolonged closure of the Straits and promises controlled energy prices and temporary inflation. For DM government bonds this turns the narrative against tightening risks and towards stable policy rates in 2026 and we feel the Fed/ECB/BOE will ease in 2027, which will bring yields down across the curve though with some traditional yield curve steepening. U.S. equities can be driven further by the tech story that is not overvalued, though the ride can become choppier with the AI labs listing in the U.S. Non-tech sector is also vulnerable to consumption slowing down to the weaker pace of income growth. By end-2026 we see a rebound in the S&P500 to 7700. Provided that AI labs growth remains strong, tech can lift the U.S. equity market again in 2027 and we see the S&P500 reaching 8200 by end-2027. Other DM equity markets and China will find it difficult to outperform the U.S. in 2026/27, as markets are no longer cheap. Brazil is our favorite over the next 18 months, as policy rate cuts helps boost the fwd P/E ratio and drive the market higher. In FX, the Iran war trends unwind into Q3 with AUD and NOK retracing, but then seeing carry trades return given their high yields and controlled government debt/GDP trajectories. The USD can see a slow decline resuming versus most DM currencies into 2027, though H2 2026 will likely be choppy.

· Risks to our views: Upside inflation risks have been reduced with the U.S./Iran interim deal, and our alternative scenario of Iran threatening a temporary closure of the Straits of Hormuz on Israel attacks on Lebanon would only add around 10% to oil prices (here). The main macro risk is that the lagged effects of the higher energy prices from March-June 2026 could cause a greater growth hit than expected. This would accelerate the shift for some DM and EM central banks from tightening risks towards easing in 2027.

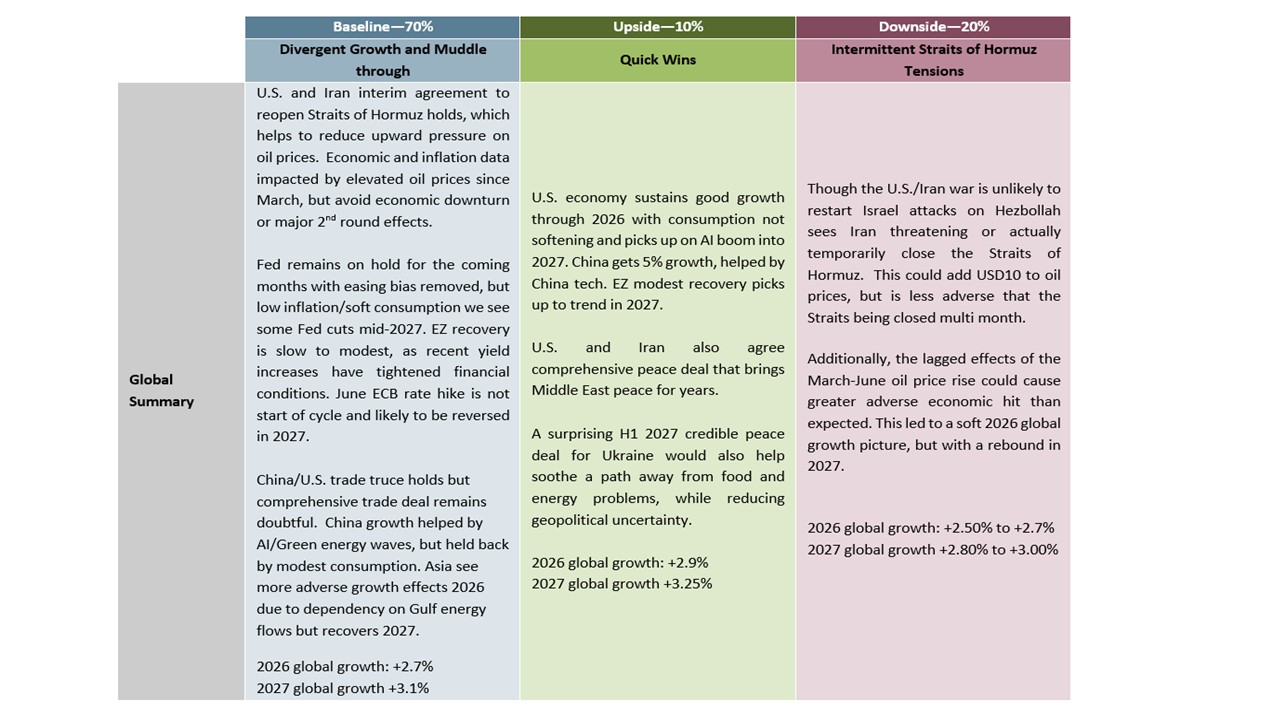

Figure 1: Economic Scenarios

Source: Continuum Economics

Market Implications

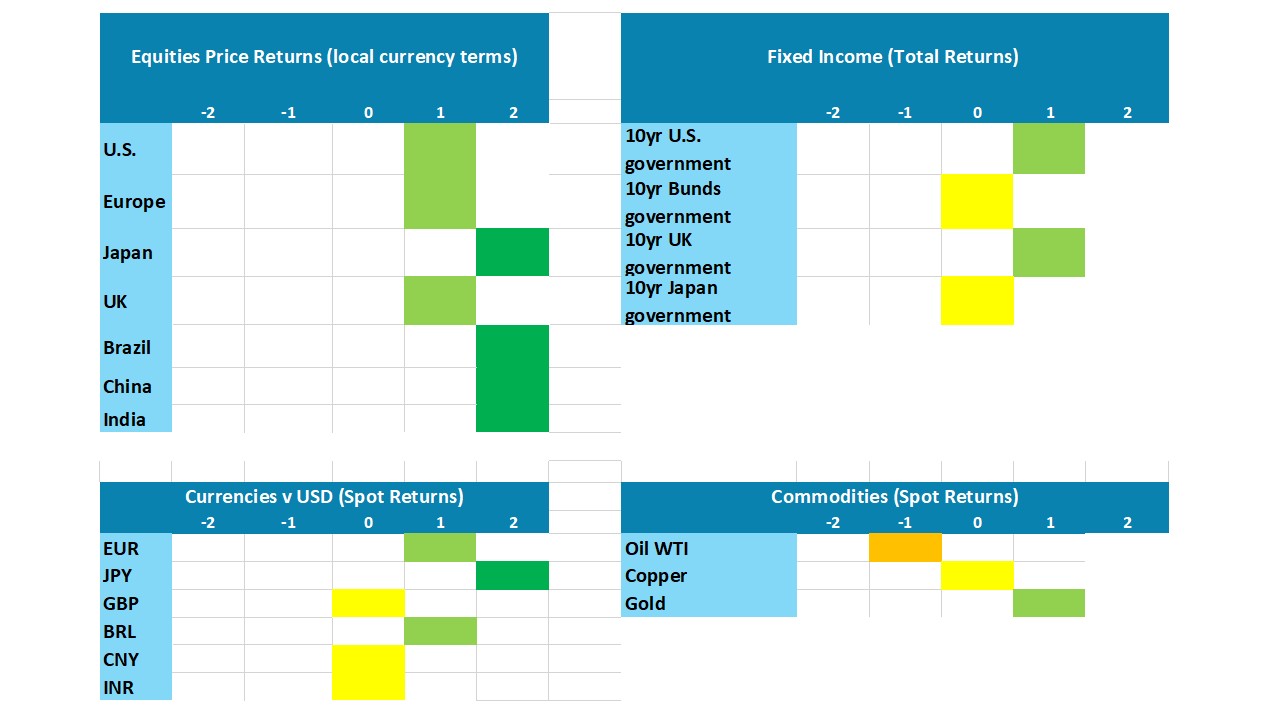

Figure 2: Asset Allocation for the Next 18 Months

Source: Continuum Economics Note: Asset views in absolute total returns from levels on June 23 2026 (e.g., 0 = -5 to +5%, +1 = 5-10%, +2 = 10% plus).

· Government Bonds. 2yr U.S. Treasury Yields could come down, as a consumption slowdown stops the Fed from tightening and prompts 50bps of cuts in 2027. 10yr is expected to to drift down, but with yield curve steepening. 10yr JGB yields will keep rising however, as the BOJ QT exceeds 6% of GDP and investors demand a yield premium.

· Equities. The S&P500 could run up to 7700 in 2026 helped by the U.S./Iran interim agreement, but we note the vulnerability in the non-tech sector. It now appears more certain that the AI labs explosive revenue growth will continue in 2027, but also that household vulnerability will be greater. We thus look for a modest rally to 8200 for the S&P500 driven by tech.

· FX. The Iran war trends will unwind into Q3 with AUD and NOK retracing, but then seeing carry trades return given their high yields and controlled government debt/GDP trajectories. The USD can see a slow decline resuming versus most DM currencies into 2027, though H2 2026 will likely be choppy. (The JPY remains extremely undervalued but needs a catalyst). In EM, the Brazilian Real still appears attractive on a total return basis in 2026/27, helped by wide nominal and real interest rate differentials.

· Commodities. With an interim U.S./Iran deal, we see oil prices at USD80 by end-2026, as inventory drawdown switches to a slow rebuild and supports oil prices above normal. Inventories less of a factor in 2027 and we see prices at USD70 by end-2027.

Figure 3: Key Events

| July 2026 | USMCA Renegotiations | President Trump has made clear that he wants to renegotiate USMCA and new threats will be used as a negotiating tool by summer. However, a deal will likely be reached by end 2026/early 2027, with USTR Greer indicating that an addendum could be added to the existing agreement with bilateral sub deals for Canada and Mexico. Odds of the U.S. not renewing USMCA are low. |

| September 13, 2026 | Sweden General Election | The current right-wing coalition still has very slim effective majority in parliament even with the far-right Sweden Democrats offering support. This is all the result of the 2022 election, which brought a fragmented result but locking out the Social Democrats even though they remained the largest party. This fragmentation was a result of a more polarized parliament, and polls suggest more of the same, but with a general drip more to the left. But even if left-leaning parties return to power, it is unlikely to change much given the current focus on defence but where an election issue may be a speedier defence build-up. |

| By September 20, 2026 | Russia Parliamentary Elections | Russia is set to hold its next parliamentary elections by September 20, 2026 to determine the State Duma,-the lower house of the Federal Assembly. All 450 seats are up for election, with 226 needed for a majority. As of current polling trends, United Russia (YeR) leads with around 35%-40% support; the Communist Party (KPRF) trails with around 10%; and Liberal Democratic Party (LDPR) also holds 8%-10%. We expect United Russia, led by Dmitry Medvedev, remains dominant after its 2021 victory. |

| October 4 and 25, 2026 | Brazil General Election | In 2026, Brazil will hold general elections to elect the next President, renew all the Chamber of Deputies seats, and two-thirds of the Senate, while also electing the governors of all Brazilian states. Lula has pulled ahead in recent polls, as Flavio Bolsonaro has been hurt by a friend being involved in the Banco Master scandal. However, given normal pre-election volatility, we still view the race is too close to call at this stage. |

| November 3, 2026 | U.S. Mid Term Elections | All seats in the House and a third of the seats in the Senate will be up for election. With the current Republican majority in the House being marginal, disappointment with the Trump administration, particularly on inflation, is likely to see the Democrats gain control. It will be harder for the Democrats to make the necessary gain of 4 seats in the Senate, with five possible pick-ups for the Democrats, but two Democrat-held states looking close too. If control of at least one of the chambers is close, the results may face legal challenges. |

| May 2027 | French Presidential Election | Opinion polls suggest that if/when a fresh legislature election occurs, this will not change parliament materially meaning insufficient fiscal consolidation. President Macron has ruled out fresh parliamentary elections and they are not due until 2029. The 2027 presidential election will likely see all other main parties supporting a candidate to stop the National Rally getting the presidency. However, it is not yet clear who this will be, and the outcome unlikely to resolve the slow progress in reducing the budget deficit. We feel France will face fiscal pressure and could face a fiscal crisis. |

| Aug 2027 | Spain General Election | The election has to occur by Aug 22, although one could occur much earlier if the current Socialist administration run of scandals deepens enough. PM Sanchez has tried to rule out a snap vote out and insisted he will stand for office again. Either way it does look as if there will be a change in who runs the country, given the right of centre People’s Party’s lead in the polls, the question being how much of a swing to the right would occur depending upon who the PP go into coalition with. |

| Sep-Oct 2027 | Italian General Election | The election has to occur by late December, but is more likely to occur earlier, probably in September. As for the possible result, important wins for Italy's opposition in southern regional elections have recently exposed cracks in the ruling conservative bloc's dominance, raising doubts over PM Meloni's ability to secure a second term. However, at this juncture, Meloni’s coalition (her Brothers of Italy party, Forza Italia and the far-right League) are ahead in national polls while the opposition needs to unify more after years of mutual hostility. |

| Oct 2027 | Turkiye Presidential Election | Parliamentary elections in Turkiye are scheduled to occur no later than May 14, 2028, alongside presidential elections. We expect the elections to be held in October/November 2027, earlier than the scheduled time. This timing is critical, as an early election called by Parliament is the only constitutional path for President Erdogan to seek another term. The presidential race will be between AKP’s candidate and an opposition candidate supported by CHP. Because the CHP’s official presidential candidate, Ekrem Imamoglu, is still jailed, the party will likely have to replace him—potentially with Ankara Mayor Mansur Yavaş—if he isn't released by 2027. The upcoming parliamentary elections are expected to be a tight race between the CHP and the AKP/MHP People's Alliance. That said, current leadership struggles within the CHP remain a major wild card that could shift the entire scene. |

| Oct-Nov 2027 | Argentina General Election | President Javier Milei’s administration’s approval ratings have fallen below 40%, as economic growth is concentrated in export sectors and households are being squeezed by negative real wages. Additionally, the government has been involved in a number of scandals, with which voters are not happy about given Milei’s promises on ending corruption. We think the October/November 2027 presidential election could be close, though opposition parties need to unify around a credible candidate and also shake off voter concerns about the major corruption of previous administrations. It is also worth remembering that polls underestimated Milei’s support ahead of last October’s elections. |