U.S. Labour: In Praise of Older Workers

· While financial pressures are prompting U.S. workers to delay retirement and work longer, this is not being realized due to deteriorating health/labour market skills mismatches and other issues. More work from older workers is unlikely to be the solution to shrinking net immigration. Meanwhile, older and other households among the bottom 50% are financially constrained, which can restrain their consumption and sustain the K shaped consumption in the U.S.

Could an increasing proportion of older U.S. workers help to offset the impact of less net immigration into the U.S.?

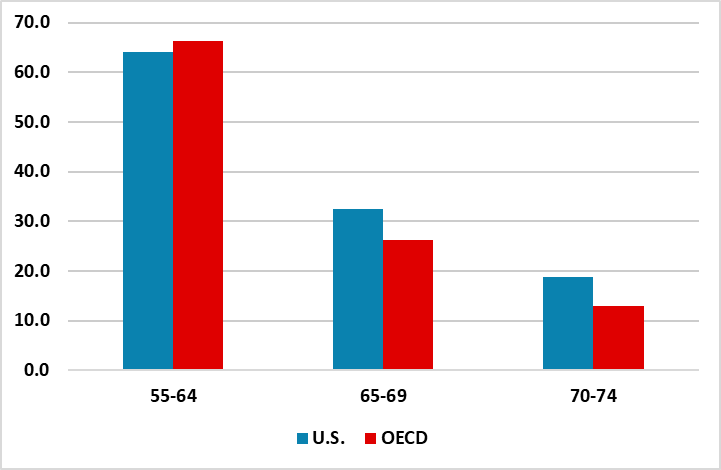

Figure 1: Employment Rates by Age (% of Population)

Source: OECD

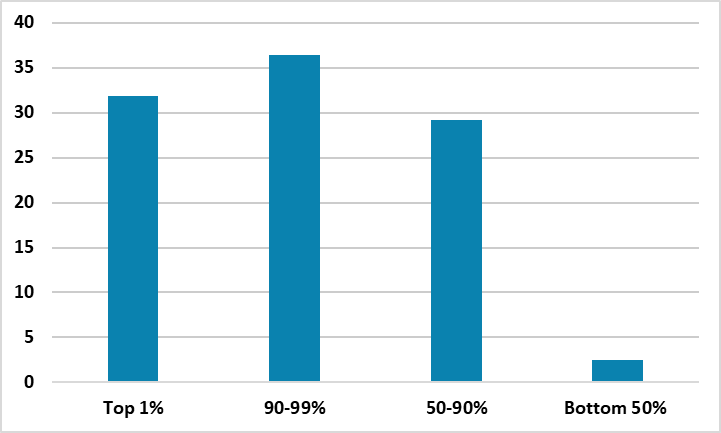

U.S. workers on average work longer than other OECD countries, with higher employment rates over 55 and into the 70’s (Figure 1). The ingrained U.S. work ethic is one force, with older workers providing knowledge and experience to balance a workforce. However, it also reflects financial pressure for large section of the U.S. workforce. Figure 2 shows the wealth distribution in the U.S., with the bottom 50% have a low share of wealth. This leaves a reliance on social security and Medicare into retirement, with private pensions now down to 15% versus 63% in 1989 – 401k have replaced more formal pensions, but lower income group have less 401k on retirement. This is causing financial pressures to want to delay retirement and work for longer.

Figure 2: U.S. Wealth Distribution By Percentile (%)

Source: Federal Reserve (here)

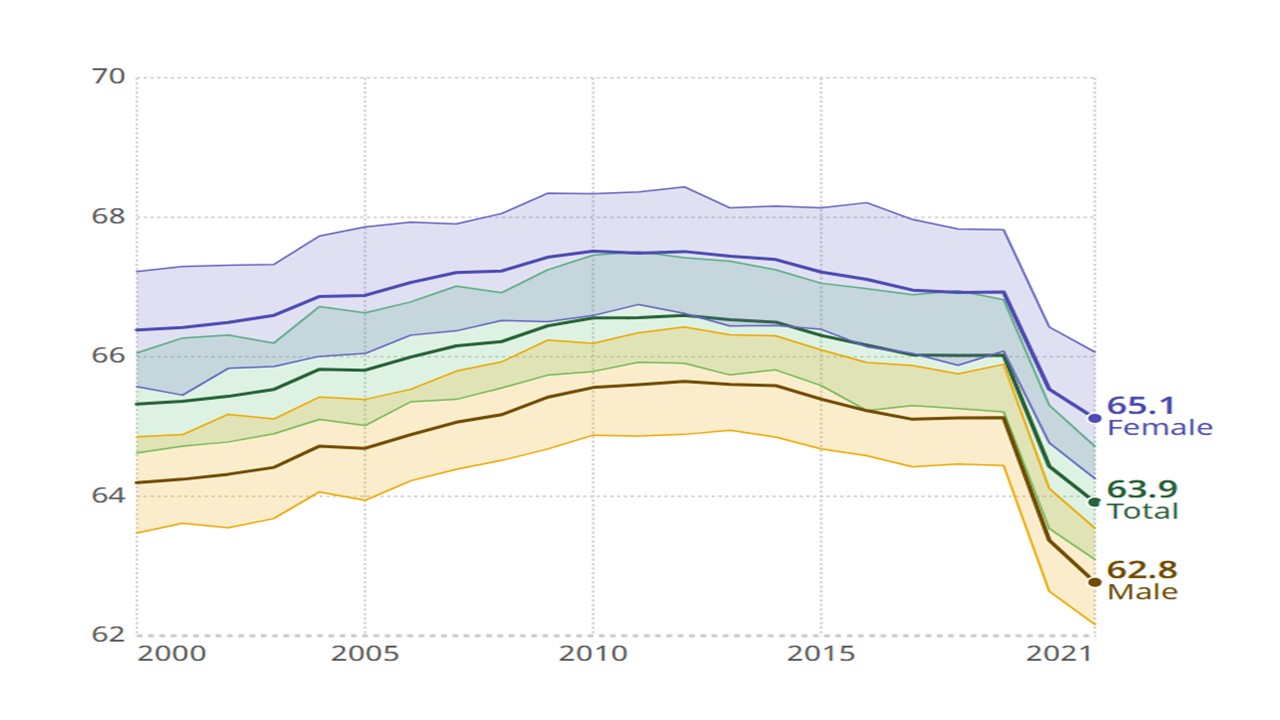

However, potential labour supply from older workers does not always translate into job growth. Transamerica Center for Retirement Studies in 2024 found that a large portion were forced into early retirement mainly for health-related reasons; employability issues and family reasons. Healthy life expectancy (Figure 3) has fallen in the wake of the COVID crisis, but medical think tanks also cite obesity, diabetes and drugs as additional reasons for worsening health trends among Americans. Meanwhile, employability issues includes skills mismatches; some companies bias against older workers and bias against employing ex-felons (a larger proportion than other countries). It is unclear whether AI will be an influence, as blue collar jobs are better protected given that widespread humanoid robotics usage is still 10 years away (here). Overall, though the U.S. workforce wants to work longer and retire later, it is not clear that opportunities will exist.

Figure 3: Healthy Life Expectancy (Number of Years)

Source: WHO

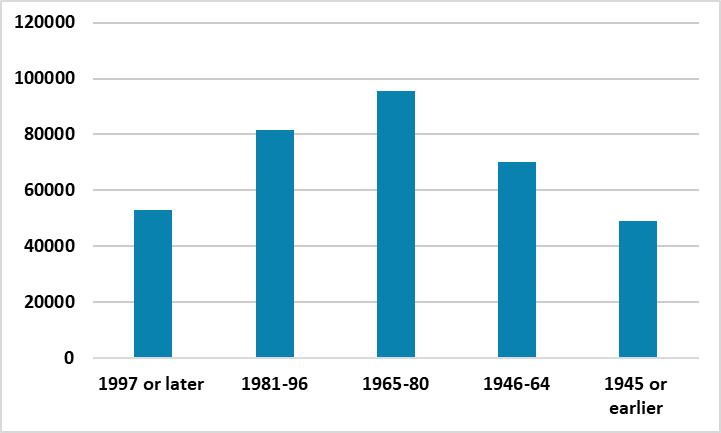

This all has an impact on consumption. Peak consumption years are 45-60 (Figure 4), before lower income in retirement causes many U.S. households to reduce expenditure nearing retirement and then in retirement. This all contrasts with the boom in U.S. consumption among the top 20% driven by the surge in housing and equity wealth, where the top 20% now account for 56% of U.S. consumer spending (here). This has prompted economists to term the phrase K shaped economy to contrast the difference between the top 20% and the rest of U.S. households. So far this has sustained overall U.S. consumption. However, if any catalyst were to trigger more normal spending in the top 20% (e.g. U.S. equity bear market), then this would likely make clearer the struggle of the bottom 50% and could depress consumption growth rates.

Figure 4: Household Expenditure per Annum by Birth Year (2023 USD)

Source: Bureau of Labor Statistics (2023)