U.S./Iran Interim Deal and Reopening Strait of Hormuz

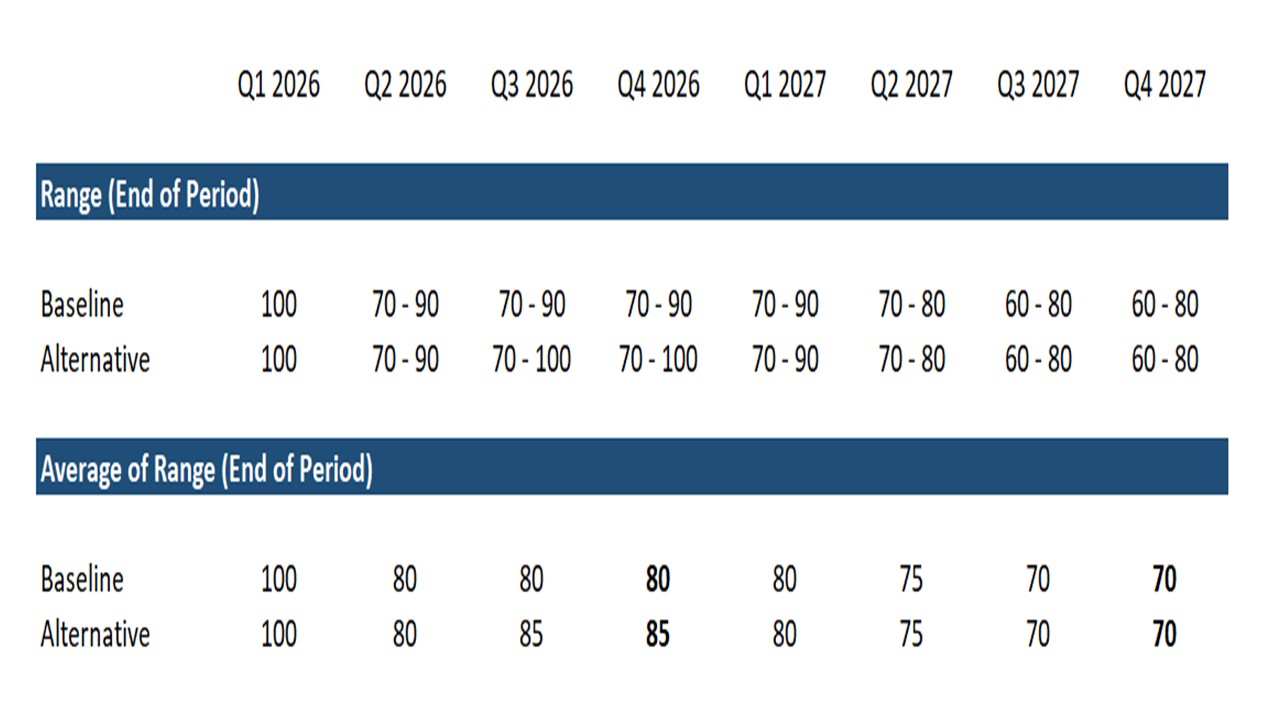

· Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). Our new alternative scenario (20%) is that Israel attacks Hezbollah to disrupt the deal and then Iran temporarily threatens to close the Strait, which could then add a risk premium to oil prices over the next 18 months. An actual temporary closure would produce a bigger risk premium.

Economic pressure has seen the U.S. and Iran reach an interim deal to reopen the Strait of Hormuz. What now for oil prices?

Figure 1: WTI Oil Price Projections (USD)

Source: Continuum Economics

Economic pressure has helped drive the June 14 interim agreement between Iran and the U.S., which is due to be signed June 19 in Switzerland. Iran’s loss of revenue from the U.S. blockade, plus the risk of damage to wells from shutdowns, helped drive the regime towards an agreement. The Trump administration, desperate to reverse politically toxic high gasoline and diesel prices, was willing to compromise to reach an agreement. Nevertheless, Iran feels that the agreement is linked to Lebanon peace as well, which Israel has not agreed to. We see two scenarios: the Strait of Hormuz remains open for the remainder of 2026 and 2027, or Iran threatens or actually imposes a temporary closure in response to new Israeli attacks on Lebanon. What is the Outlook for oil prices under the two scenarios?

Baseline (80%): Strait of Hormuz remains open for the remainder of 2026 and 2027. The agreement calls for a 30-day period to gradually reopen the Strait of Hormuz, which will see a gradual rise in oil/oil products/LNG and Nitrogen Fertilizers through the Strait of Hormuz. The agreement has already seen future prices react to the prospect of normal traffic by late July. While some dislocation could last for months, oil futures, global financial markets, and central bankers alike will treat the interim agreement as a watershed. Nuclear negotiations between the U.S. and Iran will be tricky and could drag on. However, the agreement has a minimum commitment that the IAEA will supervise the dilution of 440kg of highly enriched Uranium. Neither side will want a prolonged breakdown of the interim agreement, which would close the Strait of Hormuz again and cause economic pain. President Trump will also be politically reluctant to actually return to a closure of the Strait of Hormuz or to renewed hostilities, as he wants to move on to the mid-term elections and could be faced with a Cuba crisis next. A restart of major military hostilities between Iran and the U.S. is thus unlikely. In this scenario, our baseline is for a gradual reduction in oil prices. Iran may have the ability to impose a fee of ships later in the year, but shipowners would likely pay this and it would add marginally to the cost of oil. However, a number of countries have stopped production and restarts could take months rather than days. Secondly, the sharp rundown of inventories will likely slow noticeably by August, which removes a substitute for missing oil. Indeed, a rebuilding of commercial inventories is likely to be a priority around the world, just in case the Strait of Hormuz gets closed again. This all suggests that the decline in oil prices in H2 2026 will be slow and also in 2027 (Figure 1).

However, global central banks can now breath a sigh of relief, which at a minimum could delay further hikes (e.g. ECB in July or September) or stop hikes (e.g. BOE).

Alternative scenario (20%): Israel Escalation Triggers Temporary Strait Disruption. Israel does not like the interim agreement, as their objective is regime change in Iran. However, pressure from President Trump will ensure that Israel is reluctant to attack Iran directly, but it is highly likely that Israel will continue its military operations in southern Lebanon. This could lead Hezbollah to intermittently attack Israel, which could give Israel the excuse to hit Hezbollah and potentially southern Beirut. This could cause uproar in Iran, as Iran regards peace in Lebanon as part of the deal. This would most likely see Iran pressuring the U.S. to pressure Israel to stop. However, a chance exists that Iran threatens to suspend shipping flows through the Strait of Hormuz. The Trump administration would likely put pressure on Israel and Iran to defuse the situation. However, we feel it is a 20% probability that Iran threat or actually closes the Strait of Hormuz on a temporary basis, which would add an extra risk premium to oil prices in H2 2026 and 2027. An actual temporary closure would produce a bigger risk premium. Figure 1 assume an Iran threat, rather than actual closure, though on a temporary basis WTI could still hit USD90-95 again.