Strong Inflation Rally Continued in July: 9.1% YoY

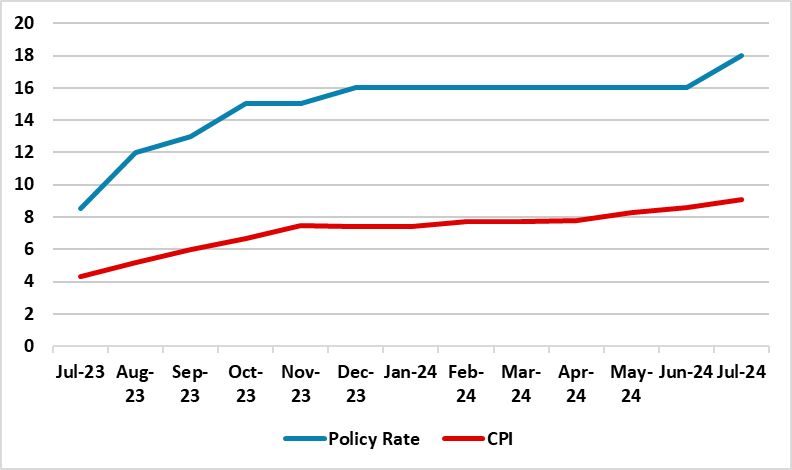

Bottom Line: According to Russian Federal Statistics Service data released on August 9, inflation jumped to 9.1% YoY in July after hitting 8.6% YoY in June, the highest reading since February 2023, due to adverse base effects, strong military spending, high domestic demand, tight labor market, continued expansion of retail and corporate lending, and recent surges in food and services prices. Taking into account that Central Bank of Russia (CBR) increased the key rate by 200 bps to 18% on July 26, we expect CBR to keep the policy rate stable at the next policy rate meeting on September 13 to view the impacts of tightening on the overheated economy while this would depend on the inflation readings in the upcoming months.

Figure 1: CPI (YoY, % Change) and Policy Rate (%), July 2023 – July 2024

Source: Continuum Economics

According to Rosstat figures, the inflation rate continued its upward trend and hit 9.1% YoY in July. MoM price growth fastened to 1.14% in July from 0.64% in June driven by the food and services prices which rose by 0.36% and 2.86% MoM (9.67% and 11.36% in annual terms), respectively. Prices of nonfood goods went up 0.58% MoM and 6.66% in annual terms. We think the inflationary pressures remain strong basically due high military spending, strong fiscal policy, demand-cost pressures stemming from high demand, and tight labor market.

June’s 9.1% YoY inflation remained far above the CBR’s 2024 forecast range of 6.5–7.0%, and CBR’s medium term target of 4%. It is worth noting that CBR decided to lift the policy rate by 200 bps to 18% on July 26 MPC meeting and cited that inflation remaining far above the CBR’s targets. CBR highlighted in its statement on July 26 that "Inflation has accelerated and is developing significantly above the April forecast. Growth in domestic demand is still outstripping capabilities and expansion of retail and corporate lending continues while returning inflation to the target requires considerably tighter monetary conditions than presumed earlier."

We expect the CBR to keep the key rate stable at the next policy rate meeting on September 13 to view the impacts of tightening on the overheated economy, but this would depend on the inflation readings in the upcoming months. Of course, it will not be surprising if CBR decides a further rate hike given inflationary risks and its hawkish forward guidance, particularly considering that it strongly signaled it will consider the necessity of further key rate increase at its upcoming meetings.

Taking into account restrictive monetary policy partly suppresses prices with lagged impacts, we feel cooling off inflation will not be straightforward as it is likely that the inflation would remain higher than CBR’s expectations in H2 2024 as we envisage annual average inflation to record 6.9% in 2024 partly due to adverse base effects coupled with surges in food and services prices.

As mentioned, the risks to the outlook remain strong as the fiscal policy making a big contribution to domestic demand coupled with continued military spending due to ongoing war in Ukraine. The risk is even higher as a larger Russian offensive operation is already ongoing, which continue to pump up the military expenses.