UK CPI Preview (Mar 26): Inflation Slips as Services Soften?

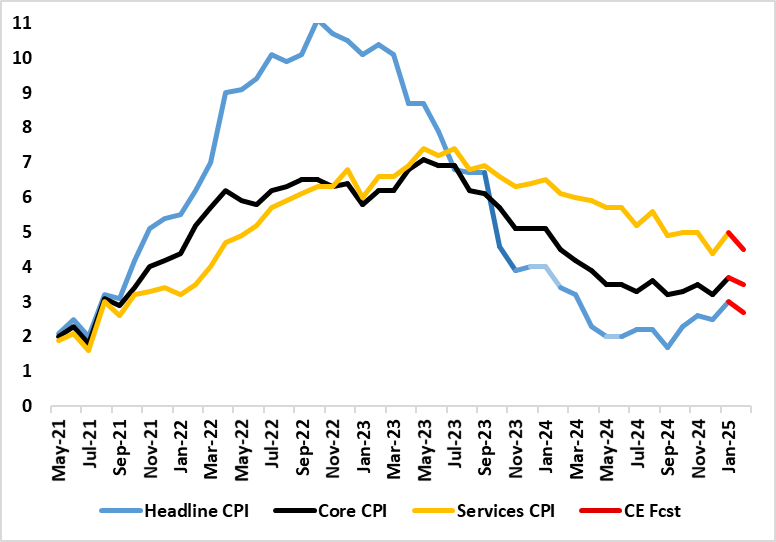

January’s CPI numbers showed a marked bounce back up, and with the 0.5 ppt rise taking it to a 10-month high of 3.0%, this being above consensus and BoE thinking. Notably services jumped from 4.4% to 5.0%, actually below expectations, having been driven higher by a swing in airfares and the rise in school fees, bit with further upward pressure evident in rents too. We think some of this services noise with reverse in February and despite the impact of higher alcohol duties and fuel prices, then headline CPI inflation may slip back to 2.7% or a notch higher – ie the BoE projection of 2.8%. In fact, we see services inflation down 0.5 ppt to 4.5%, very much below BoE thinking, all the more important as the MPC will not have advance insight into these CPI numbers. Even so, it is unlikely to alter the split MPC’ mindset with perhaps the government fiscal update due later the day on Mar 26 more important!

Figure 1: February Inflation Slips Back?

Source: ONS, Continuum Economics

The January CPI data added to worries about a fresh spike in price pressures having emerged, albeit with it unclear the extent to which pandemic-induced changes in seasonal price patterns have acted to make the CPI backdrop much more volatile. Certainly the data were not helped by an increase in the weighting of (currently high) services and a lower setting for (currently soft goods). Notably, these CPI data come after more apparently perturbing wage data, although we think that there are actually signs that companies are reacting to labor costs pressures by curbing jobs as a means of trying to raise prices. This explains our still optimistic outlook.

The January jump also reflect ‘noise’ elsewhere in volatile services and higher energy inflation both due to fuel price rises (including a rise in the energy price cap) and base effects. More notably, while overall inflation may drop back in the rest of the current quarter we acknowledge that the headline will spike back higher in Q2 as a series of regulated prices (water bills) and energy costs (mainly gas) take effect. Indeed, inflation may now average around 3% in Q3, some one ppt higher than previously thought but still well below the 3.7% rate that the BoE now projects. These added price pressures are hardly demand determined and may accentuate already weak growth, thereby further restraining company pricing power. We therefore still see 3-4 more 25 bp Bank Rate cuts this year, as the BoE reacts to weaker core inflation and the added damage to demand ensuing from price spikes.