FOMC Preview for March 18: Little change seen in either statement or dots

The FOMC meets on March 18 with rates likely to be left unchanged at 3.5-3.75%. The dots will be updated but we expect them to remain where they were in December, looking for one 25bps easing in 2026 and one more in 2027. The economic forecasts are likely to see only modest changes from September, while we expect the statement to read very similar to the last one from January 28.

The Statement

On January 28 the FOMC stated that economic activity has been expanding at a solid pace. Since then we have seen a weaker than expected 1.4% increase in Q4 GDP, but with a large negative coming from the government shutdown (Federal government took 1.15% off GDP), we do not believe the assessment needs to be changed. They added that job gains have remained low and the unemployment rate has shown signs of stabilization. Despite the weaker February non-farm payroll January’s statement also came before a stronger than expected January report, so the net jobs picture has not changed much. Inflation was seen as somewhat elevated. While there has been some progress on core CPI, core PCE prices, which have moved above core CPI, remain stubborn, while there are added near term upside risks from energy. Again, there appears to be little need to alter the assessment.

Particularly given elevated uncertainty due to the situation in the Middle East, the statement is unlikely to hint at any near term changes in policy, but will keep the Fed’s options open, as did the statement on January 28. January saw two dissenting dovish votes, from Governors Waller and Miran, who are likely to do so again. Miran has made it clear that he will do so while Waller suggested before February’s employment report that weak data would justify easing. There are divisions on the FOMC. January’s minutes showed that several saw further easing as likely to be appropriate if inflation declined in line with their expectations but some felt it would likely be appropriate to hold policy for some time.

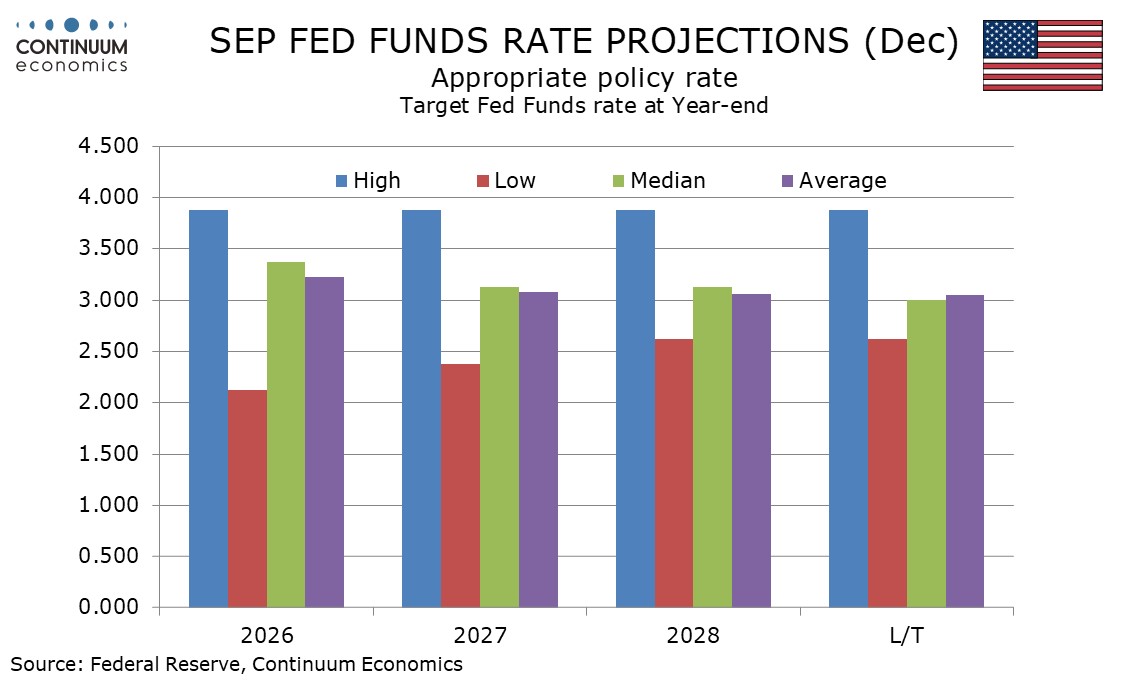

The Dots

These divisions are likely to be reflected in the dots. December’s dots for 2026 showed three (who disagreed with December’s ease) favoring rates 25bps higher than where they are now, and four wanting no change in policy, meaning a total of seven more hawkish than the median. Four were on the median looking for one 25bps easing. Eight were below the median, four looking for two moves in 2026, two looking for three, one looking for four and one looking for 150bps of easing. The later was probably Miran, though in February he stated he now backed 100bps of easing in 2026.

Two would have to shift in a dovish direction to push the median dot into projecting two easings in 2026, so that is not out of the question, but there is no strong reason to expect that there will be any shift in either direction, so we expect the dots to look similar to December’s. The 2027 and 2028 dots are fairly evenly spread with six in each year being on the median of 3.0-3.25%, which would imply one further easing in 2027 after one in 2026, and steady policy in 2028. We do not expect any change in the medians for either 2027 or 2028. The long-term median is likely to remain at 3.0% though there is some debate on this, with some feeling that an AI-led boost in productivity will lower inflation and hence lower the neutral rate, and some feeling that strong investment demand will increase it. This debate is unlikely to be resolved any time soon, though Chair nominee Kevin Warsh will be an advocate of the former view.

The Forecasts and the Future

The economic forecasts are also likely to suggest FOMC views have not changed much from December, which saw GDP rising by marginally more than the 1.8% long-term potential pace in 2026, 2027 and 2028. There will be some debate on whether AI will lift the long-term pace, but we doubt the estimate will be revised. The end 2026 unemployment view of 4.4%, unchanged from where it is now, may however be a little low. PCE inflation forecasts are likely to see a near term upgrade on energy but we expect the core PCE price view to be left unchanged. December saw a 2.5% pace in 2026, 2.1% in 2027 and a return to the 2.0% target in 2028.

A unremarkable statement, dots and economic forecasts may leave the press conference as the main opportunity for market moves, though Powell is likely to take on a cautious tone given the heightened uncertainty, but a cautious tone on inflation would imply no rush to ease. While we expect the median dot to show only one 25bps easing in 2026 our forecast remains for two 25bps moves, though this will be dependent on core PCE prices moving closer to target at least on an annualized basis, which we expect to be the case in the second half of the year as the tariff impact fades. We however now lean to the moves coming in July and October, rather than June and September. While Powell’s term is due to expire in May, it remains uncertain whether Warsh will have been conformed as Chair in time for June’s meeting.