Eurozone GDP Review: Consumer Revival, Surveys Gloomier?

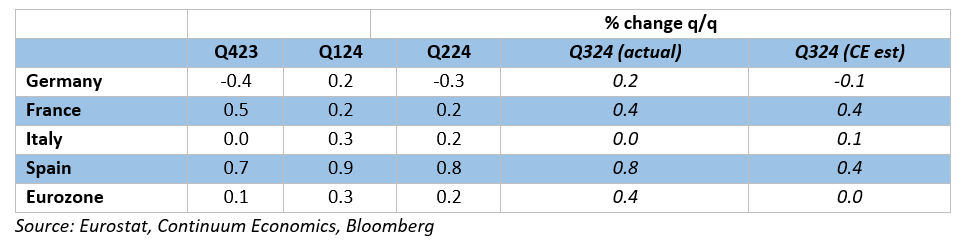

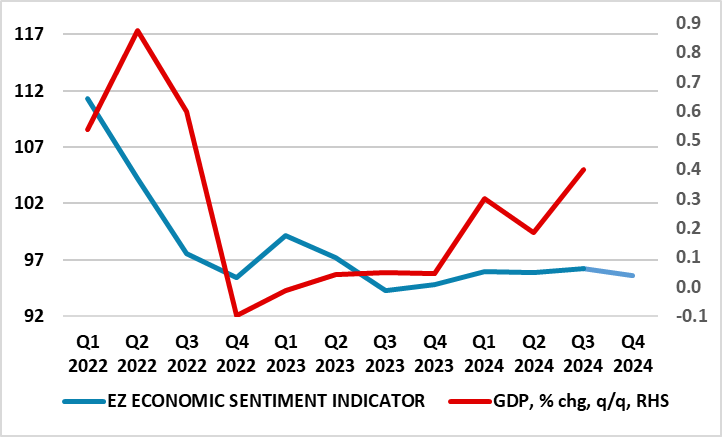

Even more clearly, the EZ economy is diverging as Germany stutters while Spain prospers. However, the risks are that the whole of the EZ is weakening given the possibly gloomier messages from business survey data. Admittedly, there were some upside surprises in the Q3 numbers, albeit with the unexpected rise in German GDP offset by downward revisions. Indeed, the data were better than both ECB and consensus thinking, but still very much with the various economies still seeing contrasting fortunes (Figure 1). This contrast reflects the varying size of the industrial sectors in these economies with those with the larger services (eg Spain) prospering more than those more reliant on recession-bound manufacturing (eg Germany). But the message from surveys is that hitherto solid services (which have been the main support to growth of late seems to be slowing) Indeed, the extent and breadth of the slowing in survey data, now including European Commission numbers at a nine-month low, has clearly perturbed the ECB, both by signaling downside risk to real activity (Figure 2) that may actually be materializing but also in highlighting softer cost and price pressures. But the ECB may draw some comfort from signs of a Q3 recovery in consumer spending, possibly a hint that disinflation has persuaded households to run down what seem to be elevated savings.

Figure 1: Divergent EZ GDP Picture Still Clear in Q3?

Missing Messages

Amid a paucity of reliable data, it is important to recognize that there are clear shortcomings to the flash estimate for EZ GDP. No details come with these flashes and they are prone to clear revisions, where even a 0.1 ppt change can be very meaningful when the economy is hardly growing. They are based on incomplete activity numbers with usually only one monthly value for services and two for construction and manufacturing. This may be why the ECB is openly more focused on survey data, especially as it is more timely. Time will tell whether the Q3 flash numbers will tell any more authoritative a story! The lack of a breakdown is also troubling as without this it is impossible to get a firm idea of where momentum may be building or ebbing. Notably, the fact that that EZ GDP has risen for six quarters masks a persistent drop in domestic demand. Admittedly, the latter may have recovered in Q3 given the limited insights from national data, and possibly from a disinflation induced recovery in private consumption (and drop in savings). This may bring some reassurance to the ECB which has been troubled by adverse trends in household spending and savings of ate. But the continued weak signs regarding capex (even in Spain) will be casting policy shadows.

ECB Still Too Optimistic

At face value the Q3 EZ result does make the ECB’s 0.8% 2024 projection more attainable, but even amid tentative better consumer signs, the question is whether momentum is ebbing, questioning (as we do) whether the 1.3% official 2025 forecast is too optimistic. While business survey data such as the PMIs have their shortcoming too, given the relative lack of geographical and sector coverage, the data from the European Commission may be somewhat more authoritative. These showed overall economic sentiment a nine-month low and very much a reading even more below par, very much questioning the apparent pick-up in GDP growth actually occurred or will persist

Figure 2: Surveys Question GDP Resilience

Source: Eurostat, European Commission

Regardless, the apparent resilience in overall GDP makes the sharp and broad fall in inflation all the more likely to have been driven more by supply factors than demand, although the weakness in the domestic economy has certainly been influential. The disinflation process may have further to run.