UK GDP Review: Momentum Dissipated?

The latest data, including that for the Q3, very much questions the UK’s economy’s apparent solidity, if not strength, as apparently seen in sizeable q/q gains in the first two quarters of the year of 0.7% and 0.5% respectively. Indeed, GDP growth has been positive in only two of the last six months of data and worth a cumulative 0.3%, and where even that much more modest momentum looks to have ebbed given that September GDP fell 0.1% m/m, soft enough to have limited Q3 GDP growth to a 0.1% q/q rise, half the pace the BoE recently pared back its estimate too but in line with our thinking. Echoing an inventory draw-down, output weakness was widespread, but most notable in manufacturing, thereby chiming with business survey data which has also pointed to a softer service sector backdrop that these figures also point to. The GDP data also are more in line with the weakness in payroll growth, albeit where the combination of small gains in q/q GDP suggest a possibly less downbeat productivity picture than the BoE reverted to in its last set of data. Regardless, the monthly real economy data may be becoming an increasingly important factor in shaping BoE policy ahead.

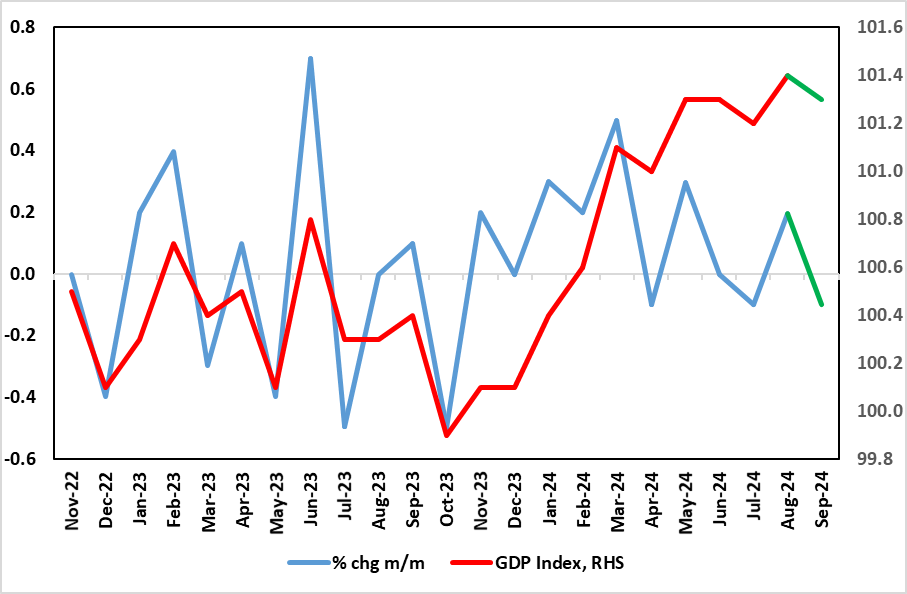

Figure 1: Momentum Has Ebbed

Source: ONS

To suggest that the unexpected GDP drop in September was a result of pre-Budget apprehension is wide of the mark; after all, GDP stopped growing between March and when the new government too office in July. As for the latest details, m/m real GDP is estimated to have fallen by 0.1% in September, largely because of declines in manufacturing output and information and communication services, after unrevised growth of 0.2% in August 2024. Monthly services output showed no growth, following an unrevised increase of 0.1% in August 2024, and grew by 0.1% in the three months to September 2024. Even construction, where surveys are the most upbeat, output grew only by 0.1% in September 2024, following a revised growth of 0.6% in

As for September, we think that mild weather curbed utility production. There was a small boost from real estate, but with something of an imponderable being the public sector which had been clearly boosting activity in H1, but may now be flattening out, if not reversing, at least outside of health.

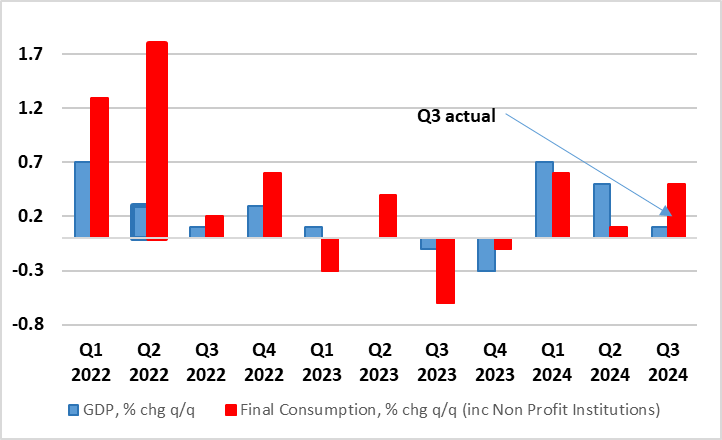

Figure 2: Less Domestic Weakness?

Source: ONS

Regardless, the lack of growth in late Q3 has created a soft base effect for Q4 growth which we see advancing just 0.2%, a notch below the BoE estimate and maybe even weaker. Regardless, this weaker immediate GDP backdrop is something that chimes more with labor market and public borrowing data and where HMRC payrolls paint a much softer backdrop and possible outlook that also conflicts very much with PMI survey numbers, at least until recently.

Notably, GDP is estimated to have increased by 1.0% y/y, with the services sector up by 0.1% on the quarter; the construction sector grew by 0.8%, while the production sector fell by 0.2%. Within the expenditure approach to measuring GDP, offsetting a correction back in volatile inventories, there was an increase in net trade, household spending, business investment, and government consumption in expenditure terms in the latest quarter. Nominal GDP is estimated to have increased by 0.8% in Quarter 3 2024, mainly driven by increases in compensation of employees and other income. However, real GDP per head is estimated to have fallen by 0.1% in Quarter 3 2024, and is flat, compared with the same quarter a year ago.

But the data has a slightly more positive tone, with the data indicative of a (modest) revival in private sector productivity given the drop in payrolls for the latter. Regardless, the real economy backdrop is likely to become an increasingly important component in shaping BoE policy, with business survey data helping provide insights into both activity and price/cost pressures. At this juncture even our below-consensus 2024 GDP picture of 0.9% may be too high, while the 1% envisaged for 2025 may be no more than potential. While December is too soon for a further BoE cut, we see two more 25 bp easing in Q1 as part of a cumulative 125 reduction next year.