Oil, Fertilizer, and the Rand will Likely Push South Africa Inflation to Around 3.8% y/y in March

Bottom Line: Following the decline in headline inflation to 3.0% y/y in February, we project that the March print will rise to approximately 3.8% y/y. This anticipated surge is driven by a combination of higher energy costs, a weaker Rand (ZAR), rising food prices, and elevated fertilizer costs—stemming from the ripple effects of the U.S.-Israel-Iran conflict. Statistics South Africa (Stats SA) is scheduled to release the March inflation data on April 22.

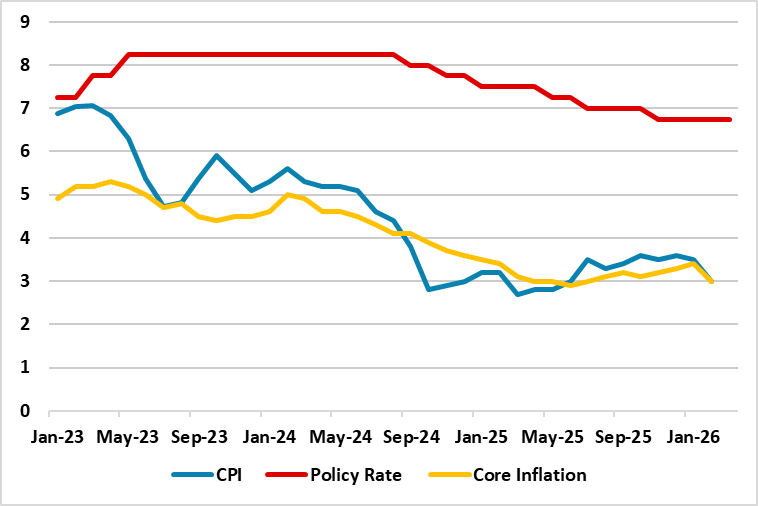

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2023 – March 2026

Source: Continuum Economics

After cooling to 3.0% y/y in February—supported by the lagged effects of monetary tightening and a relatively stable Rand (ZAR)—we envisage that inflation in March will surge to approximately 3.8%. This uptick is driven by rising energy costs, a weaker ZAR, climbing food prices, and elevated fertilizer costs resulting from the conflict in Iran. Stats SA will release the March print on April 22.

The ongoing Iran conflict continues to threaten South Africa’s inflationary outlook. We believe these risks remain significant, leading us to expect a slower convergence toward the South African Reserve Bank’s (SARB) 3% target than initially projected. While we anticipate inflation will ease in Q3/Q4 as the conflict potentially subsides, the recovery is expected to be gradual. (Note: We foresee average inflation will hit 3.8% and 3.5% in 2026 and 2027, respectively).

Following the outbreak of the conflict in Iran, the SARB significantly adjusted its economic forecasts during the March 26 meeting. In line with our predictions, SARB now anticipates that the headline inflation to accelerate to around 4% soon, with fuel inflation of more than 18% in Q2. (Note: SARB also revised its policy outlook, now projecting only one rate cut instead of two previously, while assessing two possible Iran conflict scenarios, a short-term two-month scenario and a prolonged one-year scenario, both implying the need for higher interest rates).

SARB governor Kganyago recently underscored that "Since our last MPC meeting, the key event has been the outbreak of conflict in the Middle East. Prices for commodities like oil, gas and fertiliser have moved sharply higher. (…) At this stage, it is obvious that global inflation will be higher in the near term, while growth will probably suffer from supply-chain disruptions and rising costs."

Despite energy concerns following the outbreak of war in Iran, South Africa’s national utility, Eskom, announced on April 10 that the country has achieved 329 consecutive days without power interruptions. With only 26 hours of load-shedding recorded across April and May 2025, the stabilized power supply remains a positive buffer against inflationary risks.

However, we think the Iran conflict will remain a critical factor for the South African economy. Returning to the 3% inflation target range will likely be a slow process unless the conflict loses momentum, geopolitical risk premiums dissipate, and oil prices decline in line with shifting market dynamics.