UK GDP Preview (Mar 13): Were Things Getting Better?

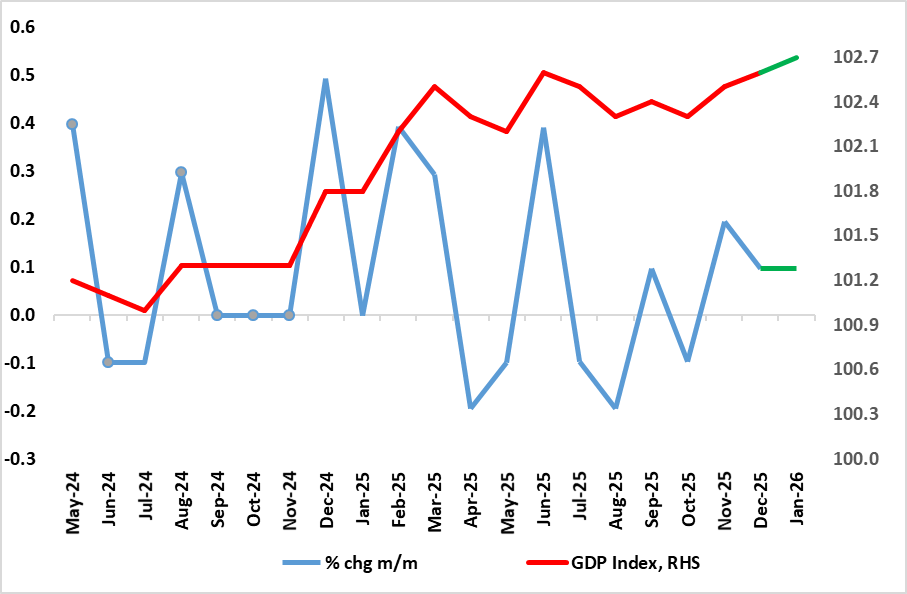

Belatedly, some good news; the UK economy grew for a second successive month in December, something not seen for almost a year. Even more encouragingly, it may very well enjoy a further rise in the looming January data, thereby providing the best three-month showing in two years. But as is familiar with recent UK real economy data, there is a negative flip side with the positive growth rates still feeble so that the economy grew by 0.1% q/q in Q4, less than consensus and BoE thinking but matching the feeble gain of the previous quarter. Moreover, any improvement in activity and sentiment (Figure 2) will, of course, be hit by events in the Middle East, implying that even if a base effect induced pick-up in GDP growth to 0.2% this quarter does occur, it will be fleeting. Even without the Middle East impact we were suggesting a sub-consensus 2026 GDP picture of 0.8% which now has even greater downside risks attached.

Figure 1: GDP Growth Better But Hardly Strong?

Source: ONS, CE

Activity in December was impaired by fresh weakness in manufacturing, utilities and construction. The data seemingly reinforced the demand worries of what now seems to be an emerging majority on the MPC; six members of the MPC appear worried about the disinflationary impact from a weak economy - four of whom actually voted for a 25bp cut at last month’s meeting.

Indeed, even given a modest further January rise, this would merely take the level of GDP to a bare notch above where it was in June. That January rise is likely to be based around already-released better retail sales data, albeit offset by what may be more (vehicle-based) manufacturing weakness and possible marked drop in the housing market

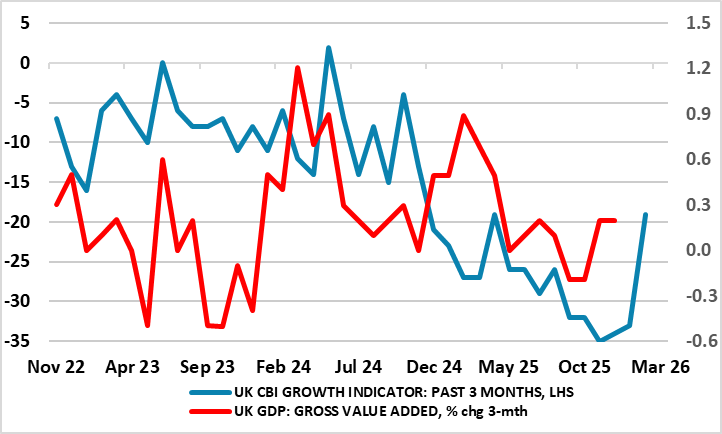

As for the outlook and perspective, 2025 growth was 1.3%, two notches above that seen for 2024. But we have been pointing to no more than 0.8% this year; this actually and merely being a minor pick-up from the anemic growth seen in the last two quarters. Regardless, we remain wary about the GDP numbers, even given their relative weakness. Although there have been some better business survey numbers, other such insights provide still sobering reading (Figure 2) as do non-official employment indicators, the latter actually suggesting a worsening backdrop of late.

Figure 2: Surveys Had Started to Offer Better Signals?

Source: ONS, CE, CBI

But obviously, the inflation and negative growth implications of the Middle East conflict complicates matters to put it mildly. The UK consumer will be largely protected from higher energy prices until July due to the price cap but companies will be hit much sooner, not only directly from higher energy prices but from supply chain effects, the latter already emerging in terms of higher freight costs.