As We Expected, Russia’s Inflation Stood at 5.9% in March

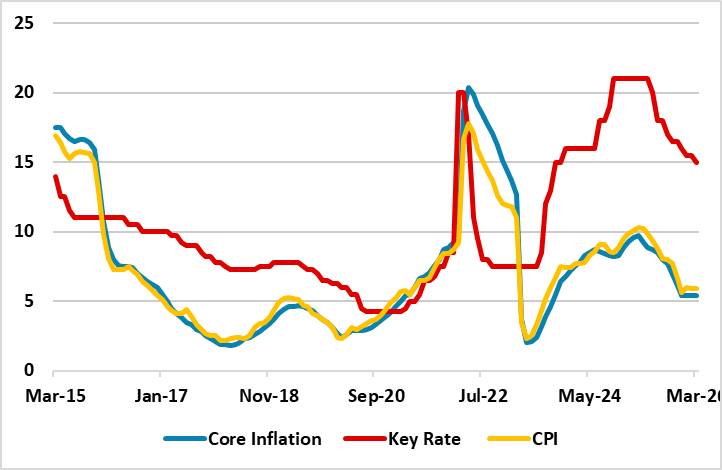

Bottom Line: As we expected, Russian inflation hit 5.9% in March owing to lagged impacts of previous aggressive monetary tightening and relative resilience of RUB. According to Rosstat’s announcement on April 10, prices increased by 0.6% in March on a monthly basis following a 0.7% rise the previous month. Despite Central Bank of Russia (CBR) predicts annual inflation to decline to 4.5–5.5% in 2026, with a goal of returning to its 4% target in 2027, our 2026 average headline inflation projection stays at 5.9% due to inflationary risks.

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – March 2026

Source: Continuum Economics

After annual inflation edged down to 5.9% y/y in February, Russian inflation hit 5.9% in March owing to lagged impacts of previous aggressive monetary tightening, relative resilience of RUB, and moderate core inflation. According to Rosstat’s announcement on April 10, prices increased by 0.6% in March on a monthly basis following a 0.7% rise the previous month.

According to a recent CBR document on commentary inflation expectations and consumer sentiment published on March 25, inflation expectations by households in one year stood at 13.4% in March 2026, when compared to 13.1% in February 2026. Companies’ price expectations remained almost the same.

Though CBR is projecting that inflation returns to the 4.5-5.5% target in 2026, with a goal of returning to its 4% target in 2027, we think reaching this target will be tough due to continued military spending, labor shortages, and supply-chain disruptions coupled with adverse effects of the value-added tax (VAT) increase and excise taxes. We believe pro-inflationary risks prevail over disinflationary ones in the mid-term horizon. Our CPI forecasts stand at 5.9% and 5.2% in 2026 and 2027 since we expect inflation will continue to soften as previous tight monetary policy affect bank lending and private consumption. High domestic gas and oil production will curtail domestic energy prices in contrast to global energy prices. Higher global oil prices in Q2/Q3 and temporary sanctions relief due to the Iran conflict could boost Russia crude exports help relieve fiscal pressures, and stimulate growth. (Note: Higher oil revenues may facilitate expanded military spending, potentially triggering demand-pull inflation. Conversely, they could moderately decelerate inflation via the FX channel, although the impact of sanctions would likely limit this effect. We expect the net result to be a secondary rather than a dominant factor).

We still believe a peace deal in Ukraine remains the real key to ease pressure on inflation and alleviate demand-supply imbalances in Russia.