UK CPI Preview (Apr 16): Inflation to Slip Further Ahead of Likely Key April Surge?

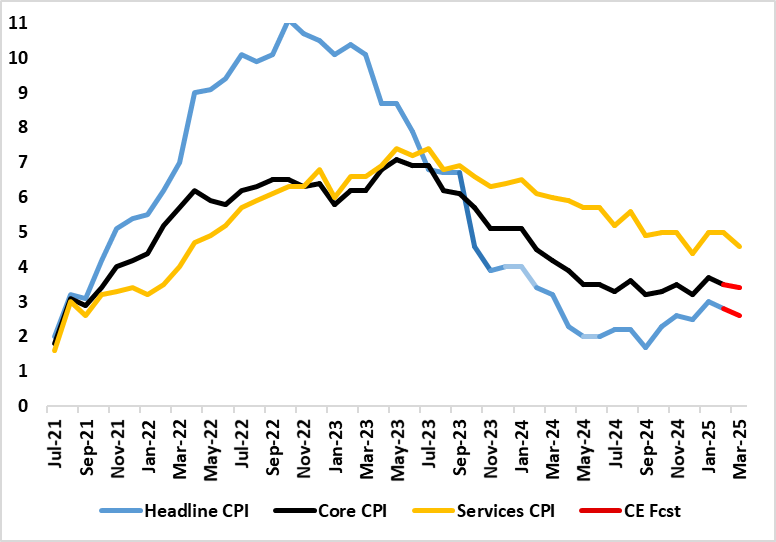

Not surprisingly, February’s CPI data provided mixed signals, albeit reversing some of the upside surprises seen in January data. The numbers may have undershot expectations, but actually tallied with our and BoE thinking, at least in terms of a 0.2 ppt drop for both the headline to 2.8% and for the core to 3.5%. Although relegated by current market ructions and tariff threats, the main near-term inflation story was (and remains) what happens in the April data when a series of energy, utility, post office and some other regulated and service price rises are due, albeit now possibly offset somewhat by a fall in petrol prices if the slump in energy prices persists. All of which would have made the March data something of a side issue even though they may show headline CPI inflation retreating a little further; we see it dropping a further 0.2 ppt to 2.6%, a notch below BoE thinking. But we will be interested to see if there are more signs of softer clothing and rental inflation, both possible signs that weak consumers are starting to rein in company pricing power.

Figure 1: March CPI Inflation to Slip Back Broadly – Albeit Temporarily?

Source: ONS, Continuum Economics

February’s CPI data provided mixed signals and came in spite of higher alcohol duties and no drop in services, the latter pulled higher by mobile phone costs, with goods inflation actually softening instead, based around clothing inflation turning negative for the first time since the midst of the pandemic in 2021 – this possibly a fresh sign of consumer weakness? Also notable was the first clear drop in rent inflation in the current cycle – also possibly a sign of the economy or at least consumer weakness. But with price pressures falling in just three of the 12 CPI components, the data hardly will soften worries about price resilience among some MPC members, especially core inflation has basically moved sideways in the last 6-9 months

Regardless, while overall inflation may drop back further in March we acknowledge that the headline will spike back higher in Q2 as a series of regulated prices (eg water bills) and energy costs take effect. Indeed, inflation may now average around 3% in Q3, some one ppt higher than previously thought but still well below the 3.7% rate that the BoE now projects but with downside risk given that current market turmoil could mean that petrol prices in April knock inflation back some 0.3 ppt.

Notably, these added price pressures are hardly demand determined and may accentuate already weak growth, thereby further restraining company pricing power, but where the BoE will now be (or should be) shifting its concerns from alleged price persistence to assessing and minimising downside activity risks from the tariff (both direct and indirect). We therefore still see three more 25 bp Bank Rate cuts this year, as the BoE reacts to weaker core inflation and the added damage to demand ensuing from price spikes, with the impact of likely further fiscal tightening a further issue alongside the impact of likely U.S. tariffs. Indeed, the May 8 decision looks a relative formality of a rate cut at that juncture, the question being how/if the MPC changes its forward guidance.