UK GDP Preview (Jan 15): Underlying and Headline Economy Fragility Continues?

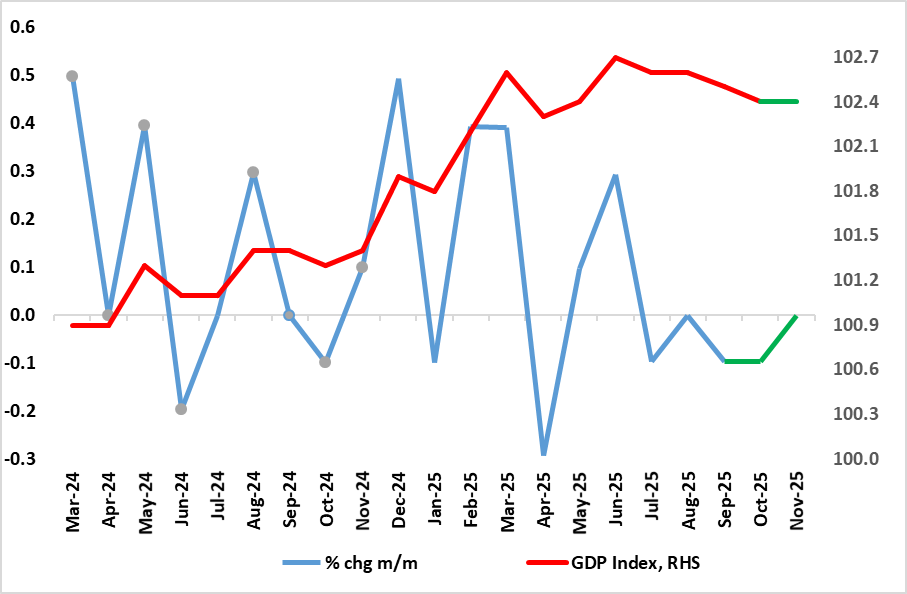

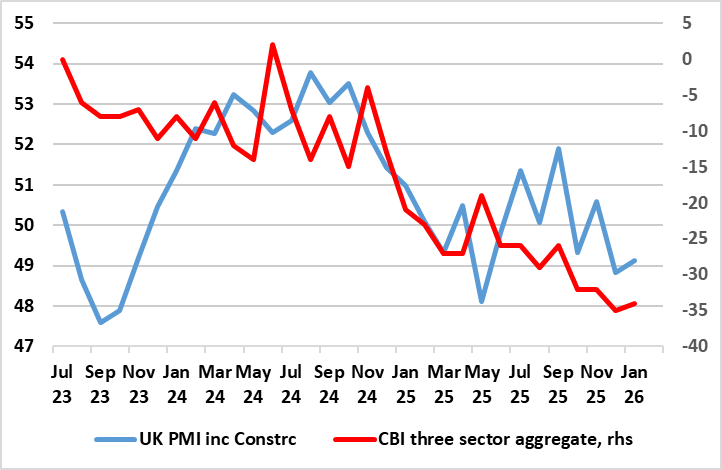

As we have underlined, UK GDP has hardly moved since March and this became even clearer with the last (October) GDP release, the question being whether weakness is getting more discernible and significant. Indeed, it has fallen in three of the last four months of data (Figure 1) and where we see no improvement in the looming November numbers with a flat m/m outcome envisaged. Admittedly, a further recovery from a cyber-attack at JLR vehicle manufacturing does provide modest upside risks, but these are offset by wet and warm weather swings, which seemingly accounted for the already-reported soft November retail sales figure. This points to Q4 GDP possibly falling by 0.1% q/q; indeed, a non-negative outcome would need growth of over 0.1% in both Nov and Dec GDP figures. A negative outcome would be below the BoE’s flat expectation, this revised down last month from its previous 0.3% forecast. This weakness chimes nevertheless with what surveys still suggest (especially construction), namely the economy is at best moving sideways, and very probably likely to contract further (Figure 2).

Figure 1: GDP Growth Ebbing, If Not Negative?

Source: ONS, CE

It is unclear how uncertainty affected activity in October. Businesses across the production, construction and services sectors reported that they, or their customers, were waiting for the outcome of the Autumn Budget 2025 announcement on 26 November 2025. These comments came from a range of industries, but were mainly from manufacturers, construction companies, wholesalers, computer programmers, real estate firms, and employment agencies. If so, then this may have damaged November GDP numbers too. This increases the chance that Q4 may see a small fall in q/q terms for the first time in two years. This would be sharp contrast to the 0.3% BoE Q4 projection had in mind prior to its belated change of mind last month.

Figure 2: Surveys Suggest Negative Picture to Persist?

Source: ONS, CE, CBI, Markit

Regardless, for some time, we have discerned very feeble momentum, which may actually be nearer zero if not weaker at least according to some business survey data, especially once ever-clearer construction weakness is incorporated. Indeed, GDP has hardly moved since March. Admittedly, solid GDP outcomes early in the year suggest that UK GDP growth in 2025 will be around 1.3% - the highest in the G7 according to the IMF but this masks what is very much a weak(er) picture in per capita terms, this being a politically important issue amid current immigration issues. Indeed, the IMF see a cumulative per capita growth of 0.9% for 2025 and 2026, the weakest in the DM world save for a similar soggy outlook for Germany. Regardless, the 0.8% GDP projection we had previously penciled in for this year actually constitutes some modest pick-up in activity momentum and thus may actually be too optimistic, something that surveys would suggest given their weakness (Figure 2). In fact, GDP growth this year may now be as soft as 0.6%. This supports our view that the BoE will cut rates down to 3.0% by end 2026!

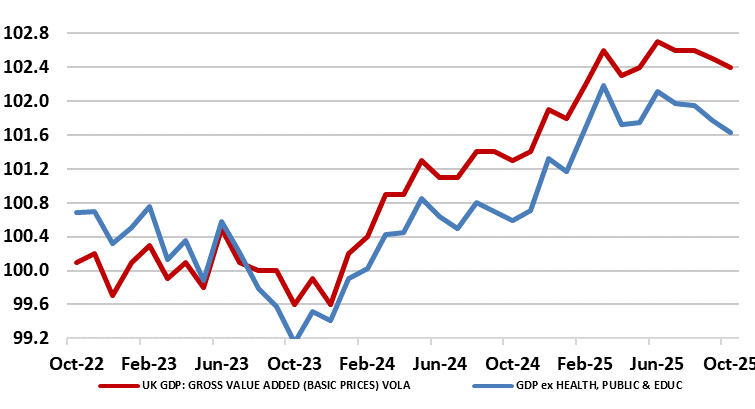

Moreover, gauging the economy is all the more difficult given the extent to which the public sector has supported growth and employment of late (Figure 3). Amid fiscal strains, albeit where the recent Budget legislated some increase in real government spending into 2027, the question is whether this latter factor will go in to reverse, sooner but probably later – health sector jobs already seem to be being shed.

Figure 3: GDP Boosted by Public Sector

Source: ONS, CE, 2023=100