South Africa Inflation Eased to 3.0% y/y in February; but Rate Cut is Unlikely on March 26 Due to Adverse Global Developments

Bottom Line: Statistics South Africa (Stats SA) announced that annual inflation edged down to 3.0% y/y in February, the lowest since June 2025, driven by slowdown in prices of transportation and food and non-alcoholic beverages (NAB). The inflation stayed within the South African Reserve Bank’s (SARB) 1 percentage point tolerance band of 3% target supported by no power cuts (loadshedding), stronger Rand (ZAR), lower oil prices in February and decrease in inflation expectations. Despite favorable February print, we now anticipate that a weakening rand, driven by higher oil prices and surging food costs (due to increased fertilizer expenses) following the war in Iran, will likely push inflation over 4% in Q2/Q3. Thus, we think SARB will hold the key rate stable at 6.75% during the next MPC meeting on March 26 due to risks.

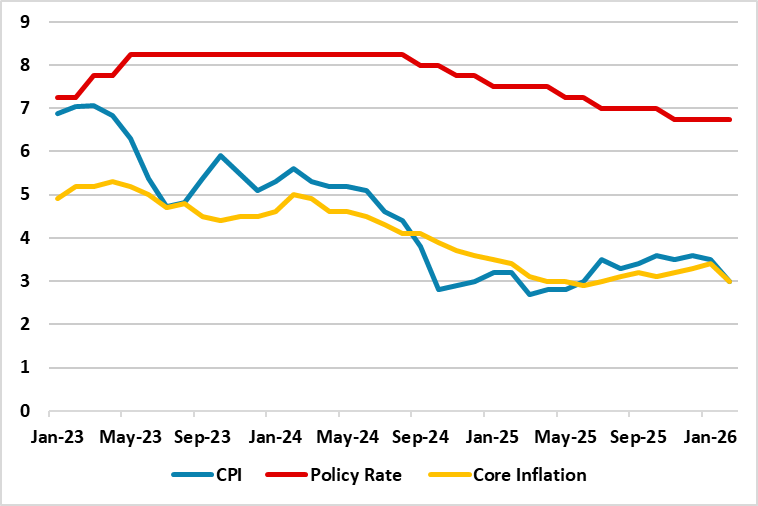

Figure 1: Policy Rate (%), CPI and Core Inflation (YoY, % Change), January 2023 – February 2026

Source: Continuum Economics

After hitting 3.5% y/y in January, annual inflation softened to 3% y/y in February the lowest since June 2025, driven by slowdown in prices of transportation and food and non-alcoholic beverages (NAB). According to the announcement, annual transportation prices softened by 2.1% and fuel prices dropped 10.1% y/y, a sharper fall than the 3.7% decline in January. Food inflation eased, with prices of food and non-alcoholic beverages rising 3.7%, compared with 4.4% in January. MoM prices surged by 0.4% in February from the previous month. Annual core inflation came in at 3% in February, its lowest print in 7 months.

On the power cuts front, South Africa’s national electricity utility company Eskom announced on March 13 that South Africa has now experienced 300 consecutive days without an interrupted supply, with only 26 hours of loadshedding recorded in April and May and the energy availability factor (EAF) rose to 65.85% for the financial year to date (April 1, 2025 to February 12, 2026). Low oil prices and suspension of loadshedding continued to help businesses and households to relieve facing increasing costs, contributing at lower inflation figures. We think February inflation outlook has also been supported by a stronger ZAR, which hovered around 15.9-16.15 against the USD.

Additionally, there was a fall in the inflation expectations in February. The Bureau for Economic Research’s (BER) latest survey for the SARB showed that in Q1 2026 (the second survey after the inflation target changed to 3%), the two- and five-year inflation expectations on average, fell to a record low of 3.6% (from 3.7% before). Next-year expectations were also down from 3.7% to 3.6%.

The inflation stayed within the SARB's 1 percentage point tolerance band of 3% target in February supported by suspended power cuts, stronger ZAR, lower oil prices and decrease in inflation expectations. Despite favorable February print, we now anticipate that a weakening rand, driven by higher oil prices and surging food costs (due to increased fertilizer expenses) following the war in Iran, will likely push inflation over 4% in Q2/Q3. Thus, we think SARB will hold the key rate stable at 6.75% during the next MPC meeting on March 26 due to risks.