UK Labor Market – Private Payrolls Stay Soft Amid Cost Pressures?

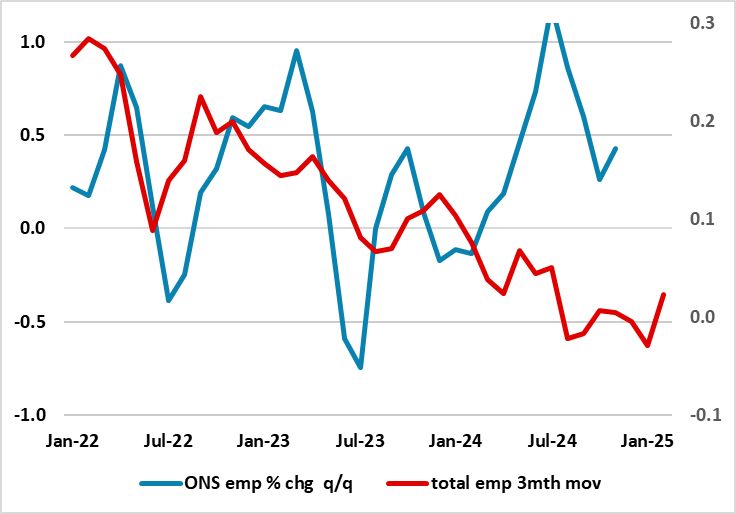

To suggest that the UK labor market is merely getting less tight misses the point entirely even given more signs of higher participation. Amid continued reservations about the accuracy of official labor market data produced by the ONS, alternative and very clearly more authoritative data on payrolls suggest that employment is continuing to contract, albeit possibly less clearly in these February numbers. Indeed, the payroll data produced by the HMRC, have now show six m/m falls since the level of payrolls peaked nine months ago, albeit with some stabilisation in the last month. Admittedly, the drop in this five-month period is only 0.1%, but this is a marked contrast to the 1.8% increase official data suggest has occurred in the last year. More notably, overall payrolls have been buttressed by sizeable public sector employment gains to a degree that private payrolls in the last five months are down almost 100K (ie -0.4%). Moreover, amid fiscal strains, non-health public sector jobs have now started to fall too, compounding what has been an ever clearer haemorrhaging of jobs in private services (Figure 2), thereby suggesting that cost pressures (now accentuated by the looming increase in employee National Insurance Contributions and the actual rise in the minimum wage) have already affected the labor market severely.

Indeed, HMRC data do show much softer wage pressures down to around 5% and somewhat more broadly than the largely bonus related drop the official ONS data pointed (at least on a single month basis. But there are even clearer contrast, if not conflicts, in the array of labor market data!

Figure 1: Sharp(er) Fall in Payrolls Contrast with Still-Strong Official Jobs Messages

Source; ONS, HMRC

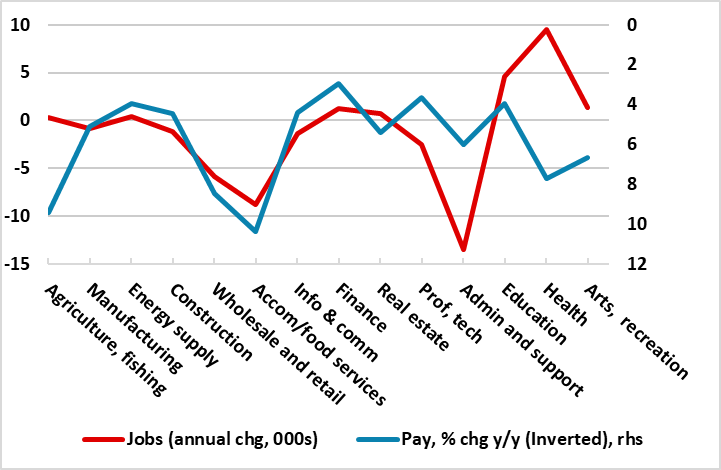

The looming National Insurance changes taking effect in April mirror similar moves seen of late (eg 2022, 2011 and 2003) what happened then is that Labour intensive sectors and other service-based sectors reduced both headcounts and vacancies either in anticipation or immediately after the change was effective. Tis already seems to be happening, but possibly as much to already rising pay bills as to the threat if even higher labor costs to come. Indeed, as Figure 2 illustrates, the labor market is working as it should do, with sectors where pay is the highest seeing falling payrolls as companies try to adjust to already high pay bills by curbing jobs to limit the rise in labor costs that otherwise would either/both hit profit margins and raise the prospect of higher consumer prices. This is one the main reasons why we think he BoE is too concerned about the overall inflation outlook as (to us|) we see companies are already acting to rein in their labor cost bills for fear that raising prices may only service to reduce demand. Indeed, as Figure 2 illustrates there is already a clear and inverse relationship between employment changes and pay growth, the exception being health where government spending initiatives are both trying to repair real pay and actual output in the sector.

Figure 2: Sectors Facing Highest Pay Growth Seeing Clearest Job Shedding

Source; HMRC