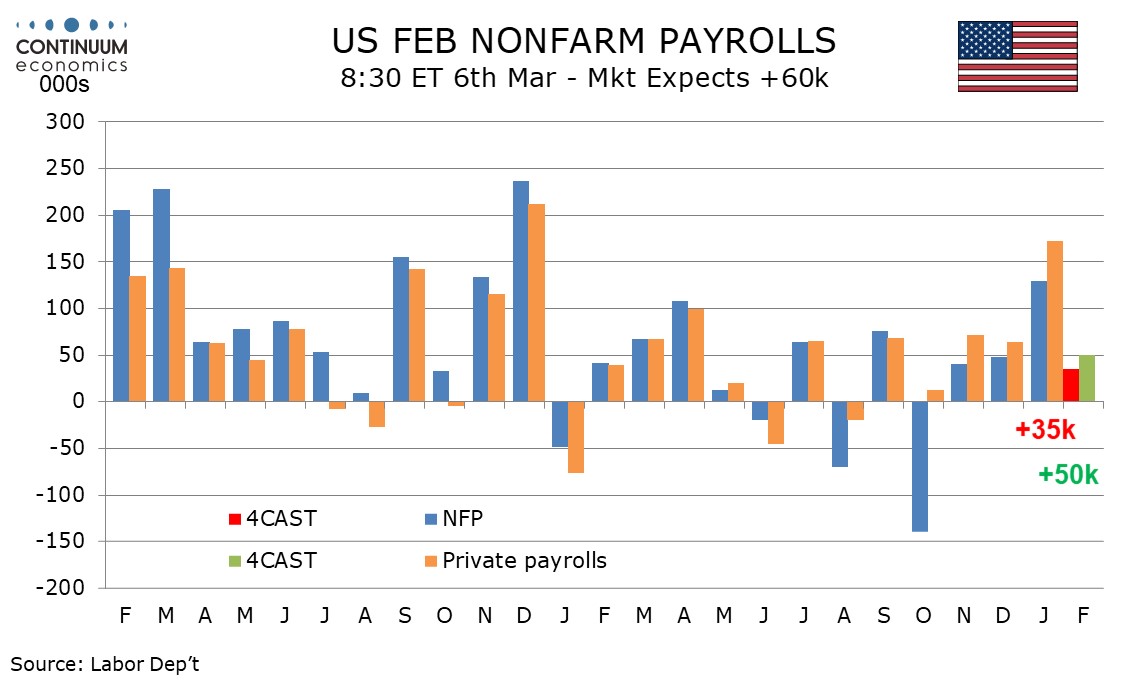

Preview: Due March 6 - U.S. February Employment (Non-Farm Payrolls) - Not as strong as January, but still marginally positive

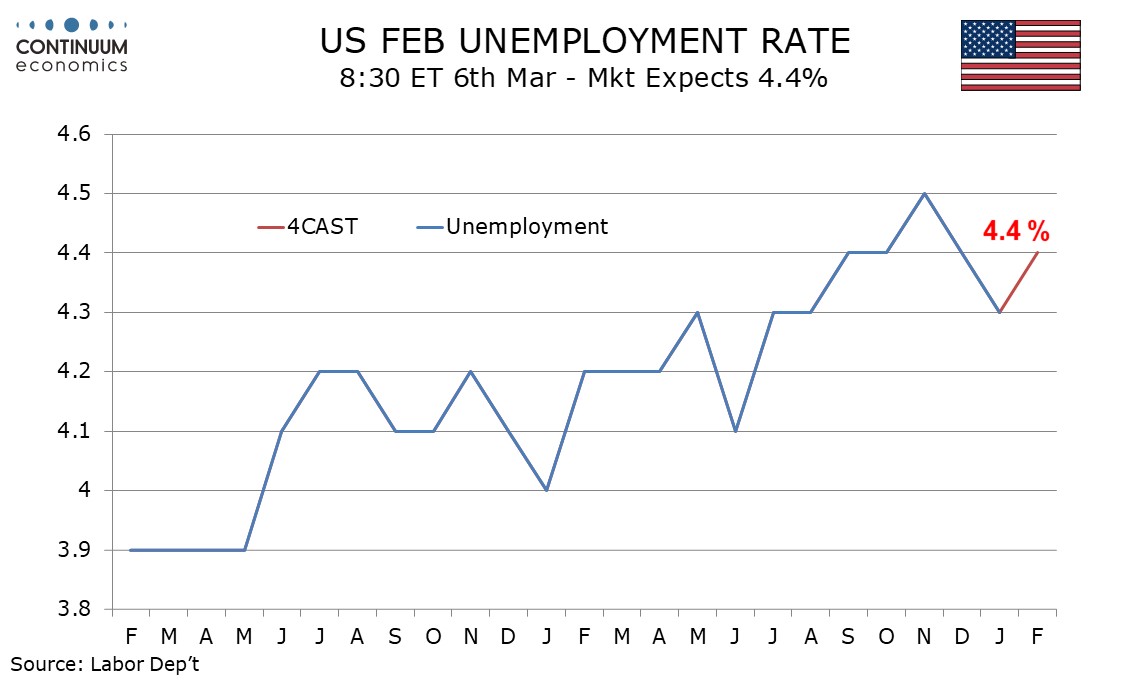

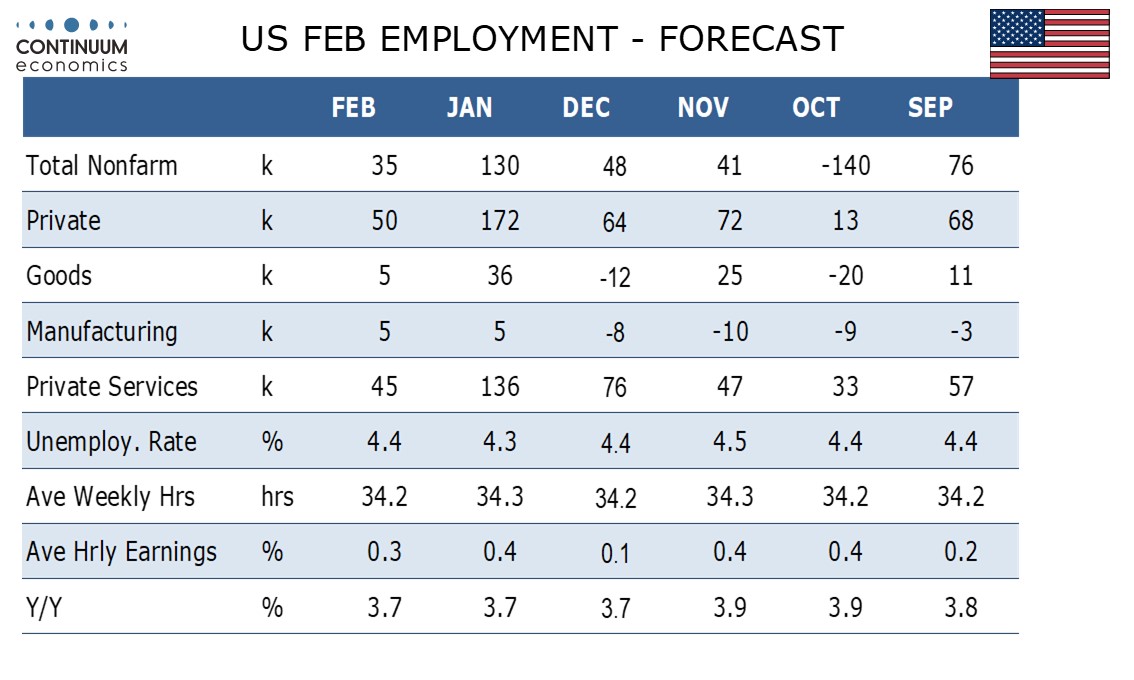

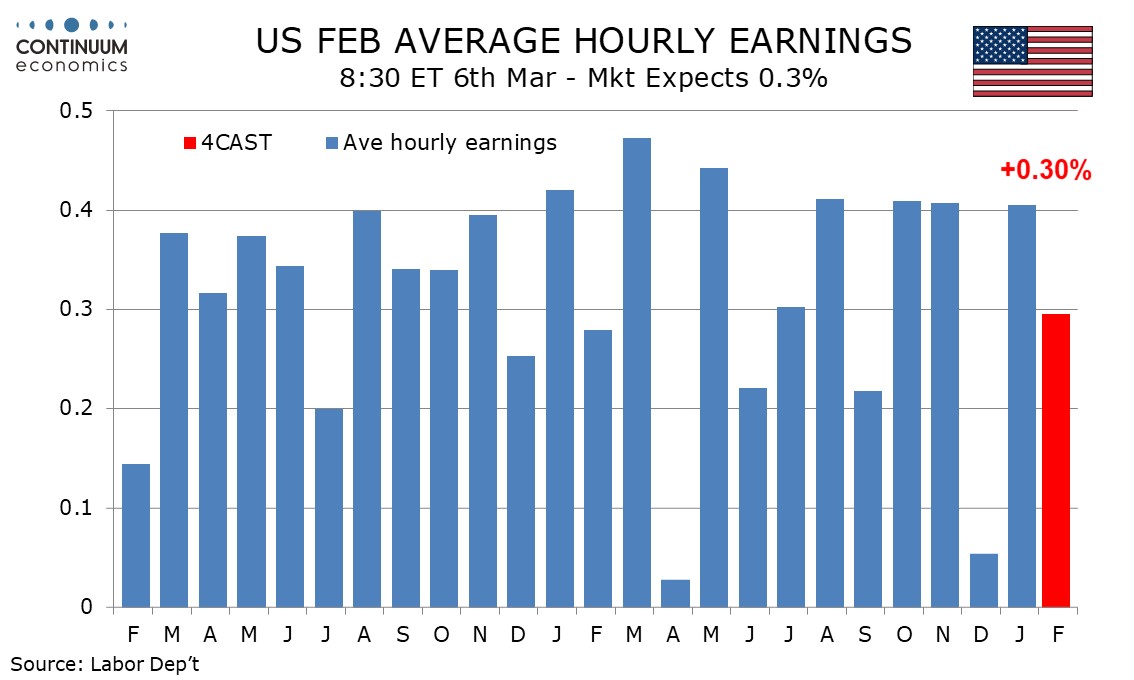

We expect February’s non-farm payroll to rise by 35k overall and by 50k in the private sector, both four month lows and significantly slower than January’s above trend respective gains of 130k and 172k. We expect unemployment to edge up to 4.4% from 4.3%, reversing a January dip, and average hourly earnings to rise by 0.3%, in line with trend.

January’s strength was led by health care, which increased by 123.5k, and a significant slowing is likely in February, though the sector is still likely to fully explain February’s payroll gain, and most of that in the private sector. Revisions tend to be negative and January data may be revised lower, though probably only by around 25k, leaving the month still well above the late 2024 trend.

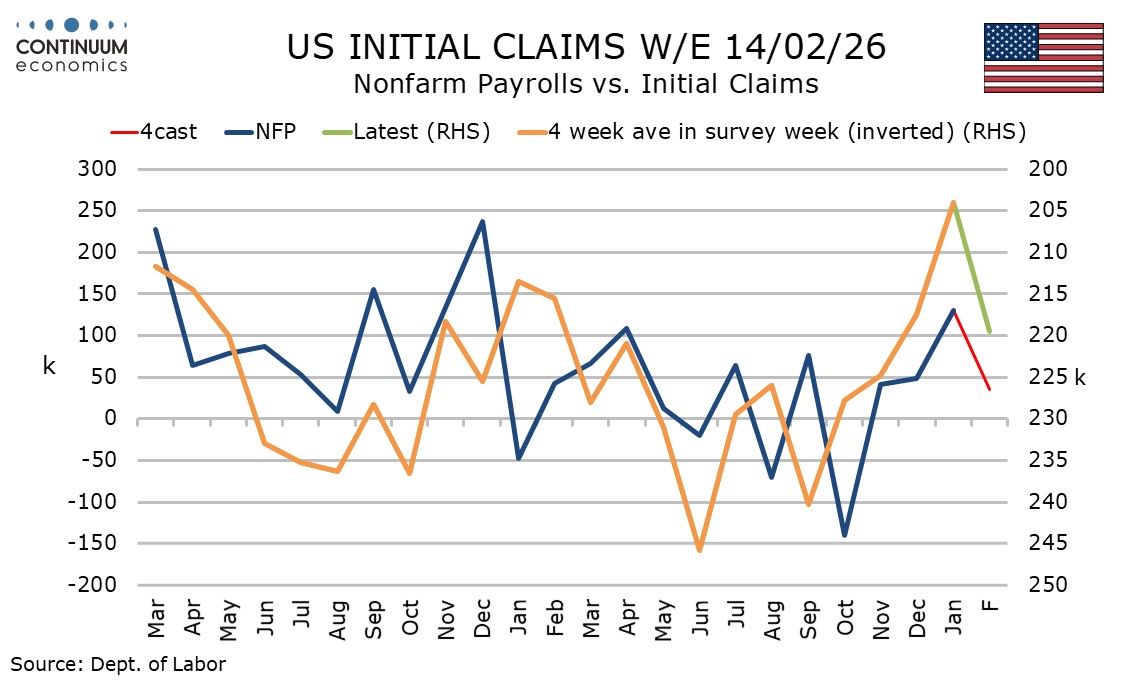

January’s data was supported by strongly positive seasonal adjustments, which turn negative in February. January’s data was also surveyed before some bad weather in late January, which would weigh on February data, though initial claims were back to normal in February’s payroll survey week after a bounce during the cold weather spell. A clearly negative payroll looks unlikely.

We expect goods employment to rise by 5k, led by a manufacturing sector that is showing signs of improvement, with construction vulnerable to weather. We expect private services to rise by 45k, mostly in health, while government falls by 15k, which would be the slowest of five straight declines.

We expect unemployment to rise to 4.4% from 4.3%, putting it back at December’s level, though before rounding we expect a rate of only 4.36%. Both the labor force and employment are likely to correct from strong January gains, in part on weather, with employment showing the larger moves in each month, with employment in the Household Survey (which calculates the unemployment rate) showing more volatility than the payroll, which surveys businesses.

January reports usually see population control adjustments to the Household survey, though this year they have been delayed to February’s report. These adjustments could be negative if reduced immigration is captured more fully, though back month data will not be revised.

Average hourly earnings trend is around 0.3% per month, though the last four months have seen three gains of 0.41% and one of 0.05%. We expect February to be in line with trend and close to 0.3% even before rounding. That would leave yr/yr growth stable at 3.7%.

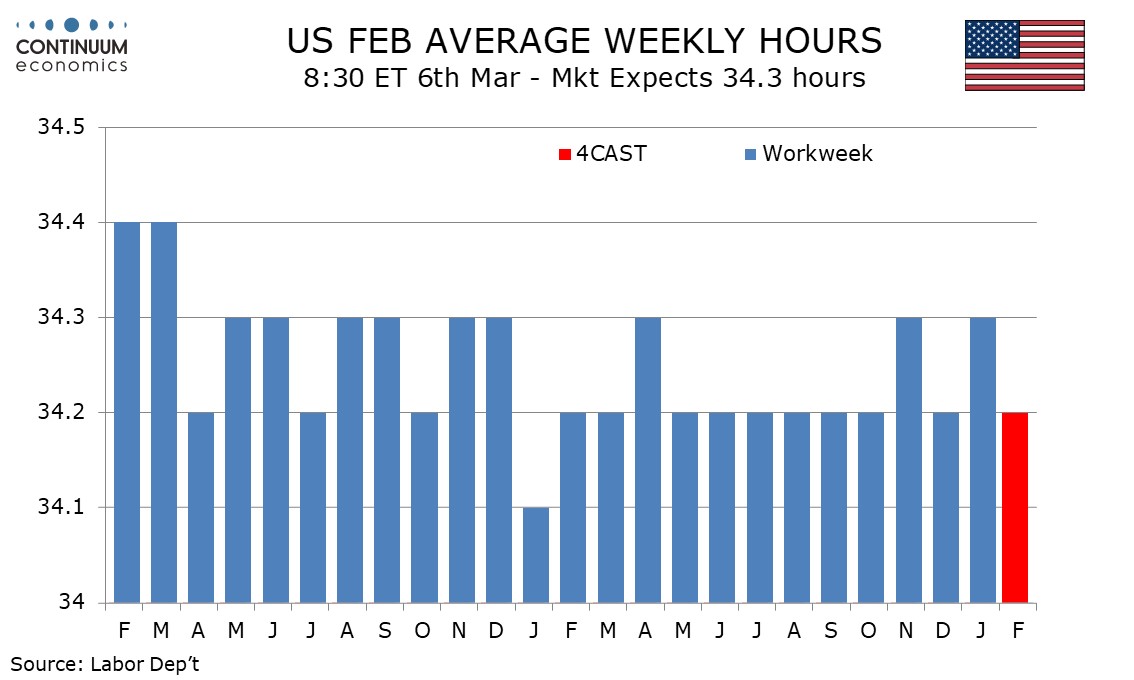

We expect an average workweek of 34.2 hours, down from 34.3 in January. While November and January delivered workweeks of 34.3 hours, seven of the last nine months have been 34.2, suggesting January’s bounce will not be sustained. If it is, it would be a positive signal for GDP.