UK CPI Preview (Apr 22): Inflation Being Fuelled But Watch Financial Conditions?

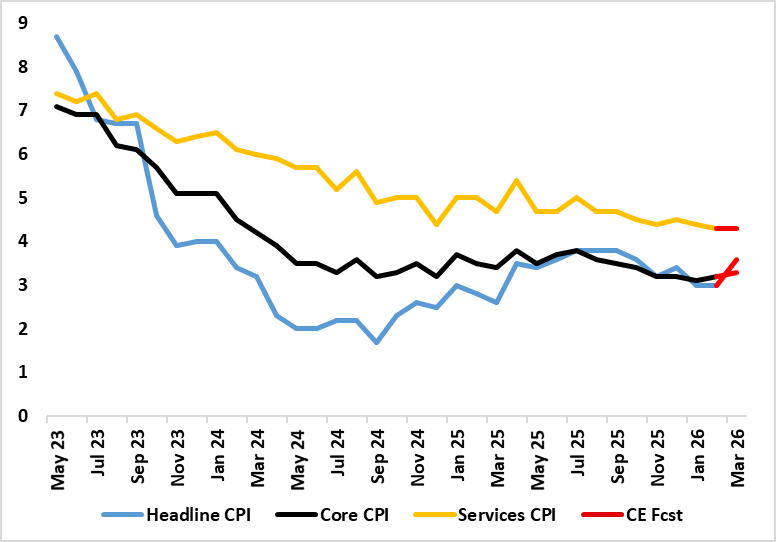

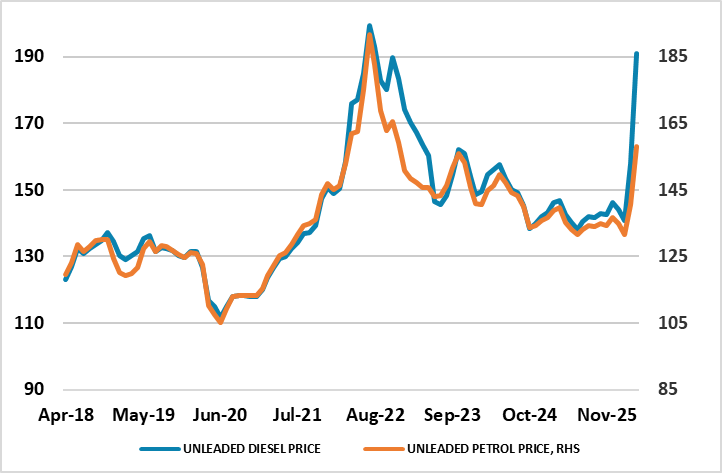

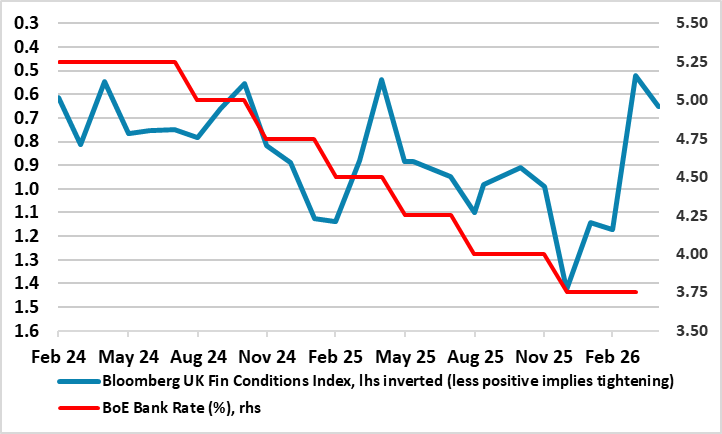

The stormy weather inflation wise is now very evident, most notably in UK fuel prices surging. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching both consensus and BoE projections we see it jumping to 3.5% in March. Services, however, may stay at 4.3% which was a four-year low (Figure 1) but the core could edge back up a notch due to higher non-energy good inflation (Figure 1). The markedly and relatively greater surge in diesel relative to unleaded fuel (Figure 2) warrants a hardly surprising upgrade to the price outlook for the rest of the year. On the basis of our baseline 4-8 week war thinking, we see the headline CPI falling back for in April before moving back higher in May in Q4 but then dropping back to end the year to 2027 at just over 2.5% but with the 2027 picture little changed, not least as tightening financial condition bite (Figure 3).

Figure 1: Headline Stable But Core Higher

Source: ONS, Continuum Economics

This outlook is above consensus thinking (but below that of the BoE) for next few months so that we see an average headline this year of 3.0% (0.2 ppt higher than in the Outlook a month ago), with this nearly all a result of the relatively greater jump in diesel prices. Indeed, the current jump in diesel relative to unleaded is both marked and unusual and a clear contrast to the 2022 energy shock (Figure 2) which was more gas price orientated. But we see the current 2.4% 2027 CPI headline consensus being undershot with actually a base effect induced below target period for a few months around the middle of next year.

This latter view very much reflects a position where we see little second round effects, with even BoE Governor Bailey suggesting firms do not have much pricing power and we would argue that households will not have much wage bargaining power either even if their inflation expectations do rise. Admittedly, not all aspects of recent CPI data have been reassuring in this regard, albeit with a fresh fall in catering services inflation, often seen as an indicator of price persistence given that the sector’s cost base is very much wage related. Even so, the evidence on this is mixed with HMRC pay data very clearly showing a slowing in wage inflation for accommodation and food services while ONS data suggest private sector core average earnings may already have slowed to rate consistent with the CPI target. Regardless there are other clearly reassuring aspects most notable in still low lower rental inflation which at just over 3% has more than halved in the last year, surely yet another sign that the housing market is in the doldrums. But while February also saw a fresh rise in non-energy goods inflation, we think this will not persist given both weak global demand and dumping of goods by China once destined for the U.S.

Figure 2: Diesel Surging Far More than Petrol Prices

Source: ONS, RAC – pence per litre

Indeed, it is notable that real activity indicators are already flashing worryingly with the March CBI retailing survey at its weakest since the GFC while last month’s PMI was below the key 50 level once construction sector is included. And we think real activity data will only get worse as consumers and firms face higher prices even if the later start to ebb in due course. Even without the Middle East conflict impact, we were suggesting a sub-consensus 2026 GDP picture of 0.8%. Now, while recession may (just) be avoided, the economy is likely to be even weaker ahead as the backdrop and outlook has changed so that GDP growth may be as low as 0.5% this year, ie almost half the BoE’s pared-back projection made in February. This reflects already weak demand which we think at least partly reflects tighter financial conditions. The latter is increasingly important given the manner in which they have tightened of late (Figure 3), practically nullifying recent curs in Bank Rate. As for the later, given the economic fall-out alluded to above, we side with Governor’ Bailey apparent scepticism that the MPC will Raise rates and instead continue to think policy will be eased afresh by late-year.

Figure 3: Economy at Risk From Tightening Financial Conditions

Source; Bloomberg, BoE